June '25 Market Update

THE BIG STORY

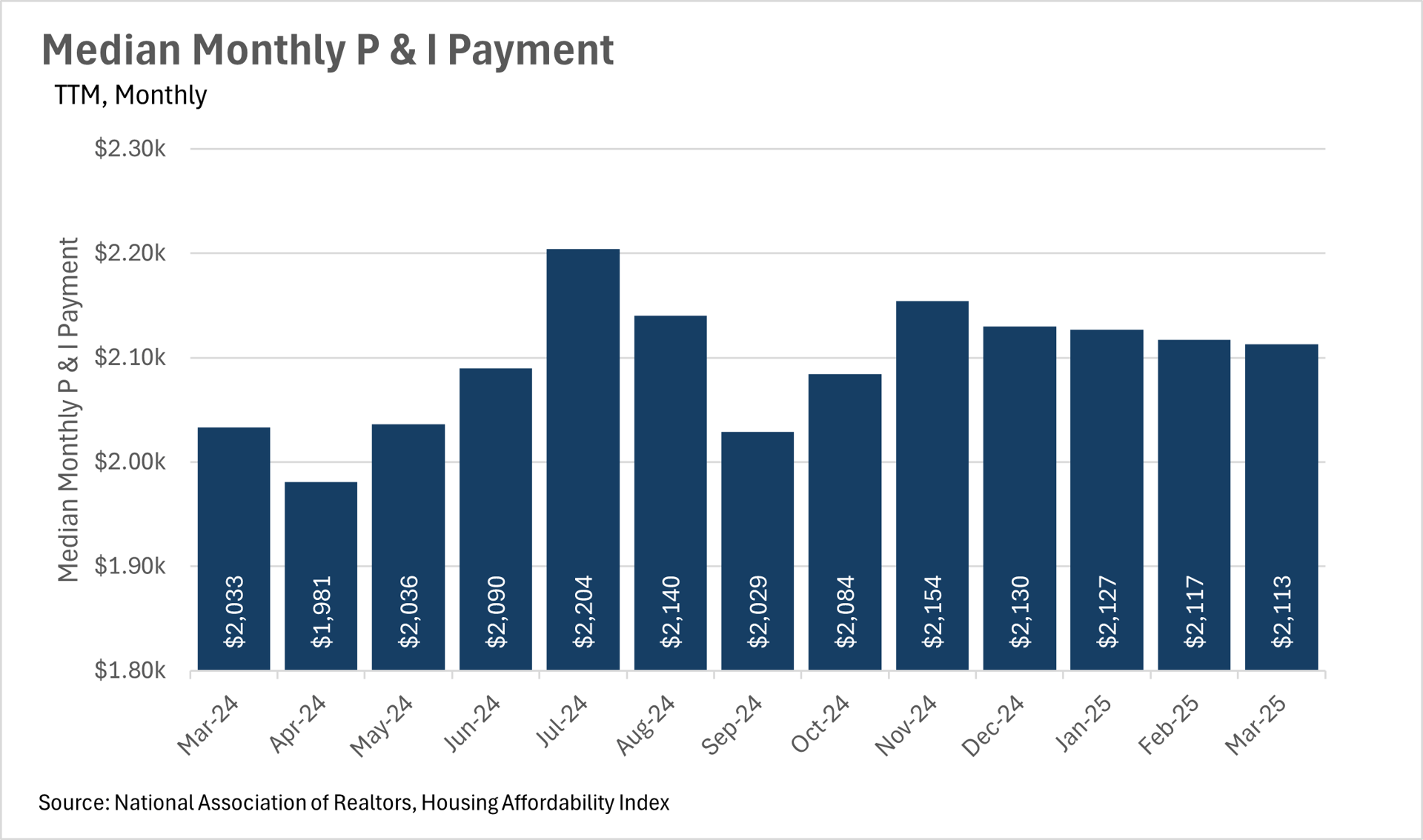

GROWTH IN MEDIAN MONTHLY P&I PAYMENTS CONTINUES TO OUTSTRIP INFLATION

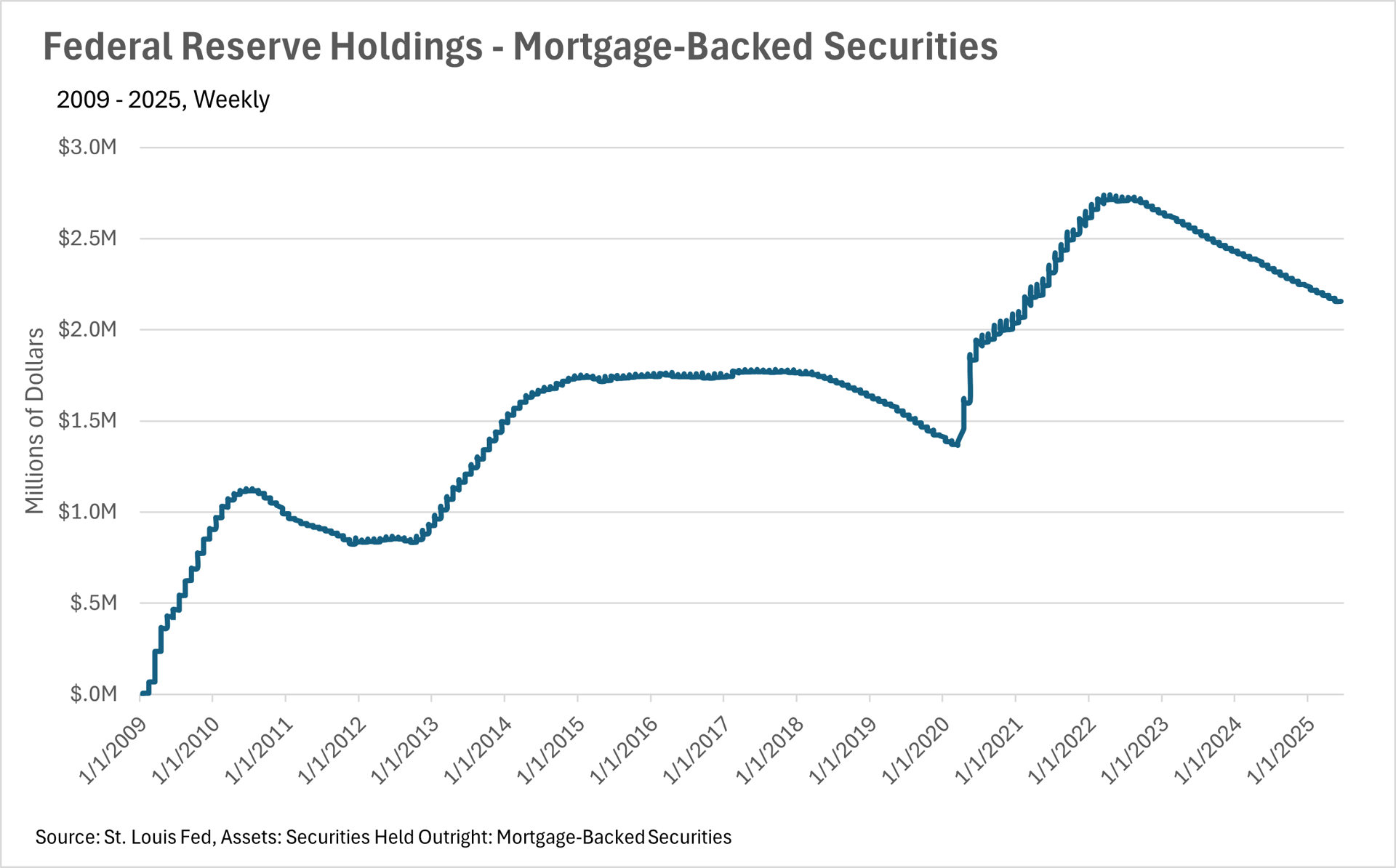

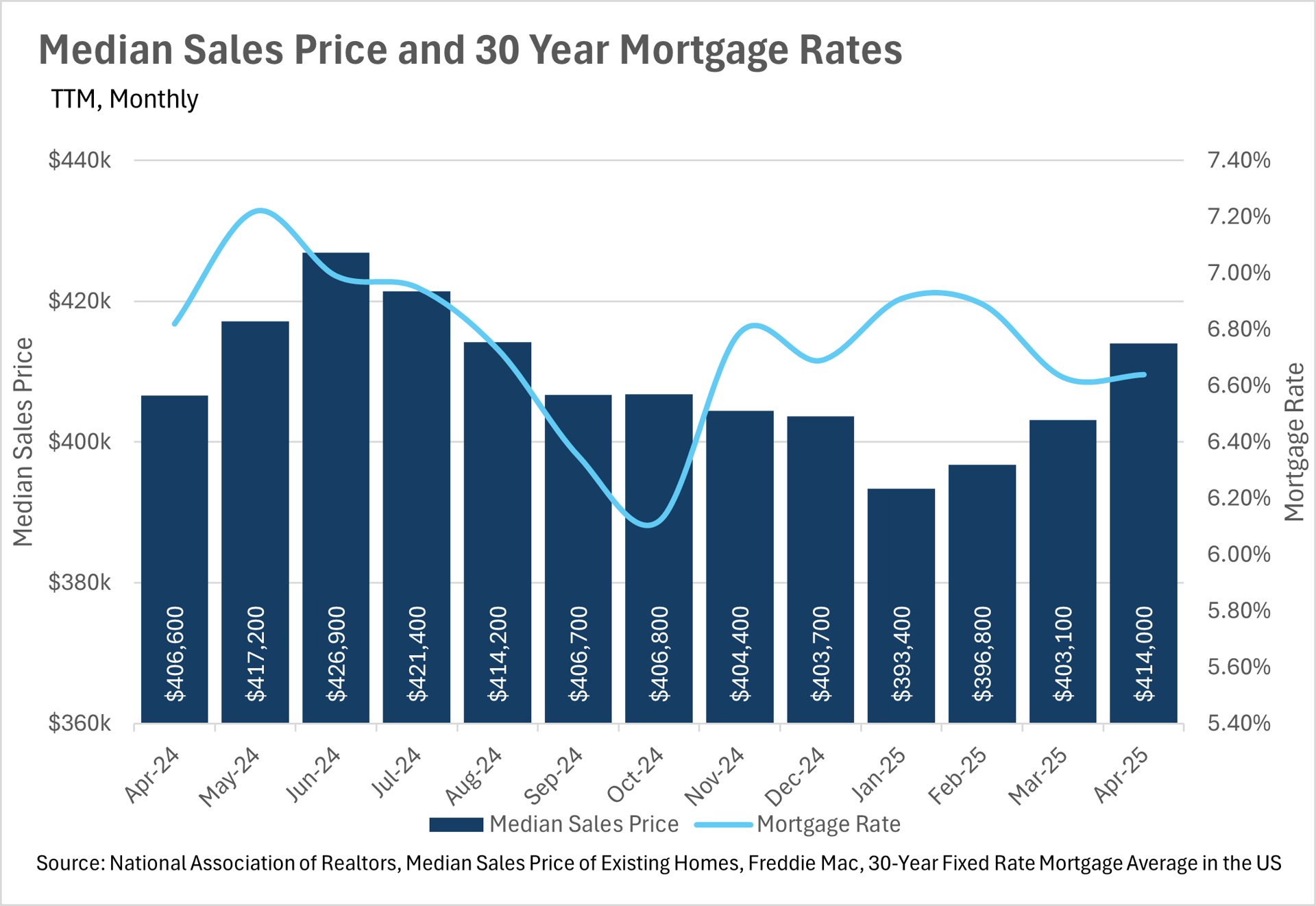

MORTGAGE RATES REMAIN HIGH, DESPITE LOOMING ECONOMIC UNCERTAINTY

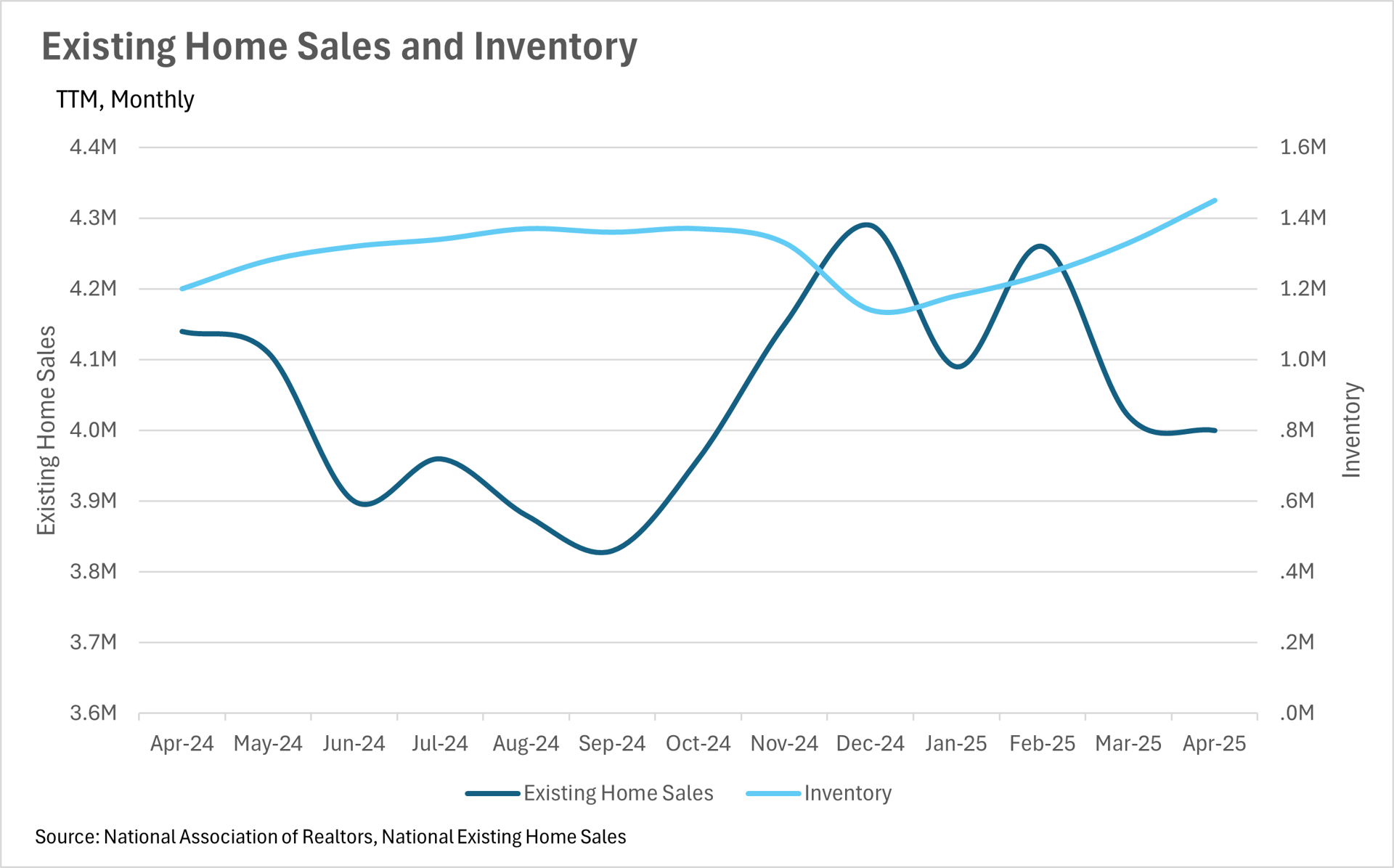

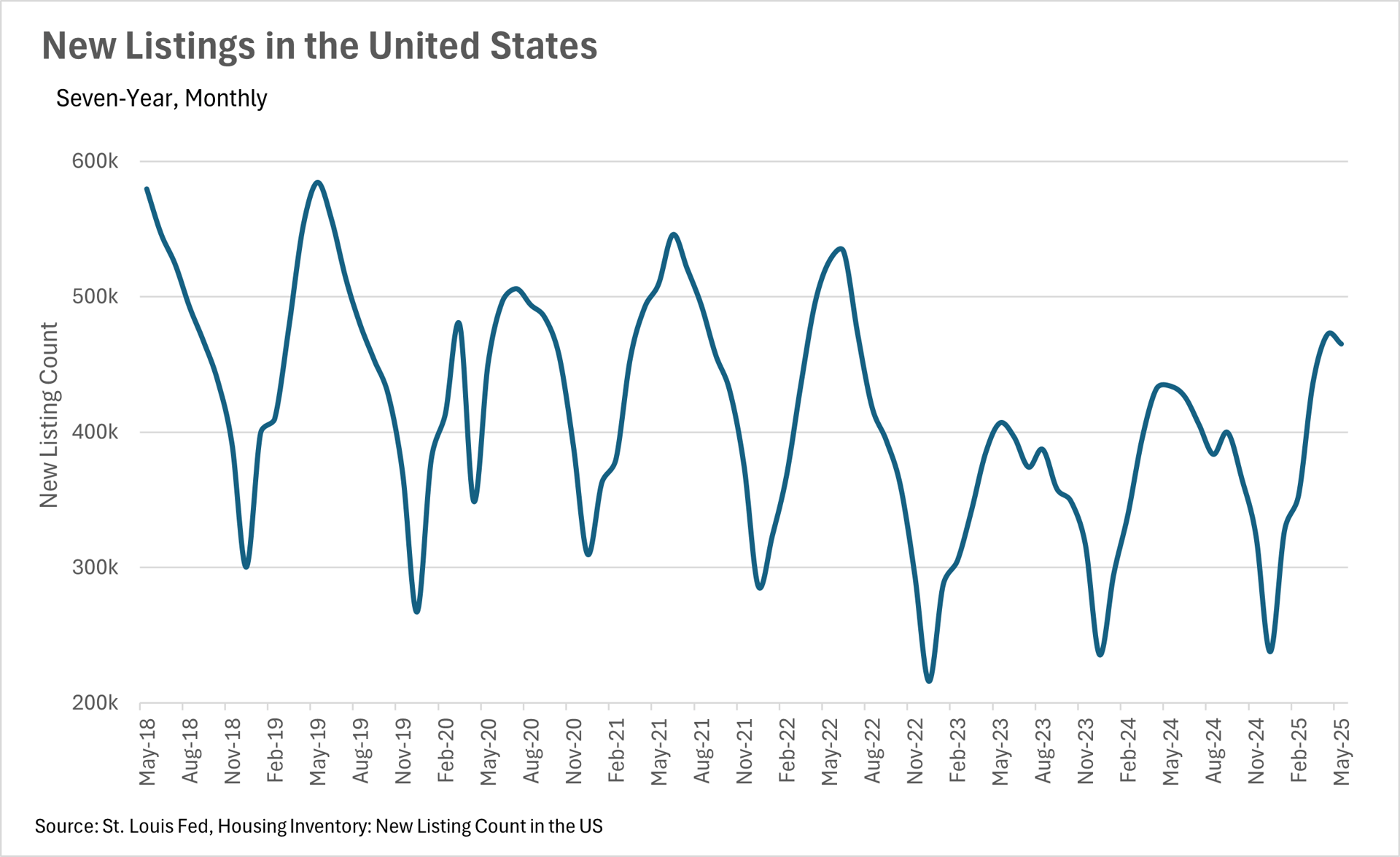

Nationally, the US housing market in April 2025 mirrored California's trends:

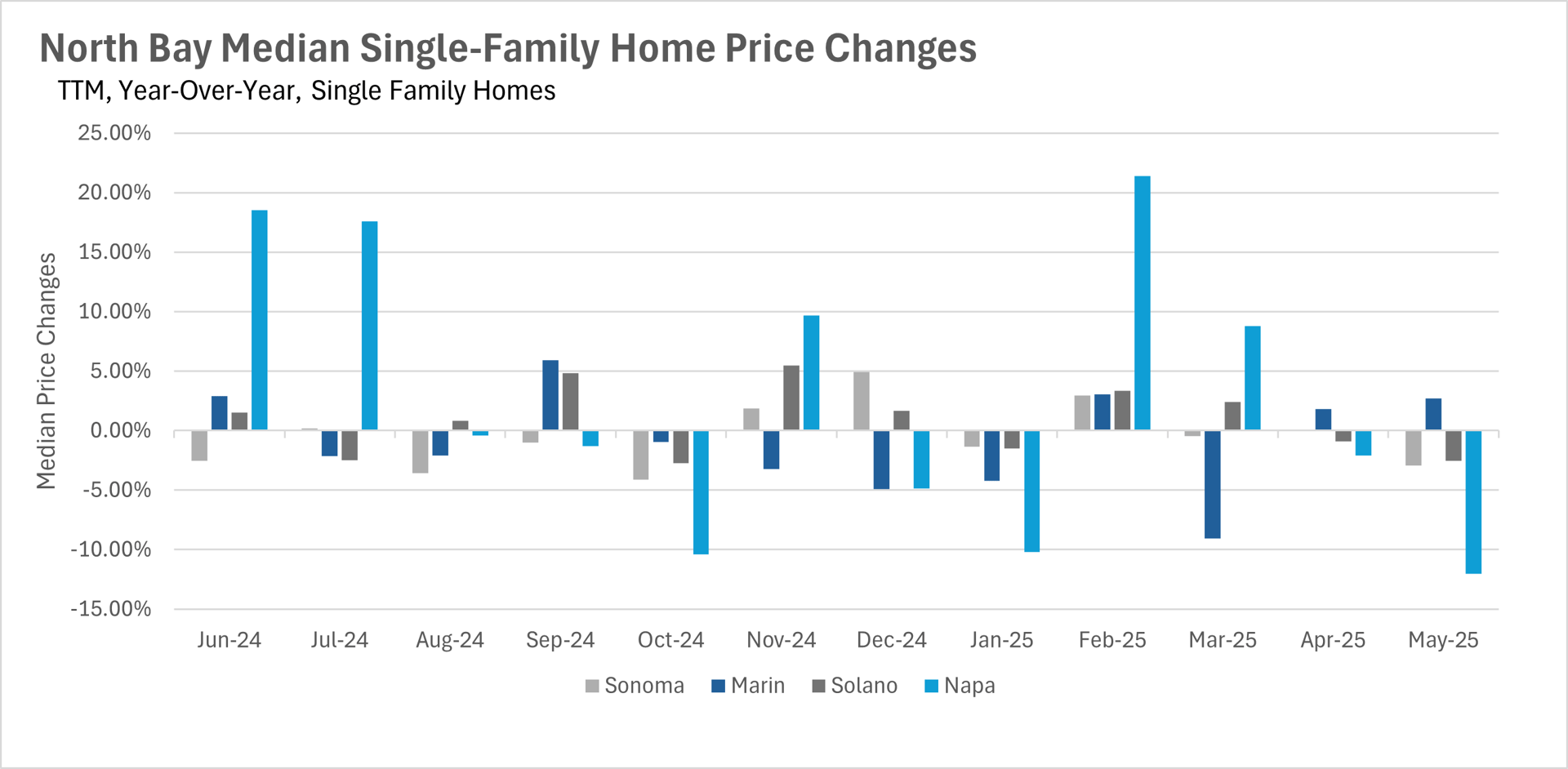

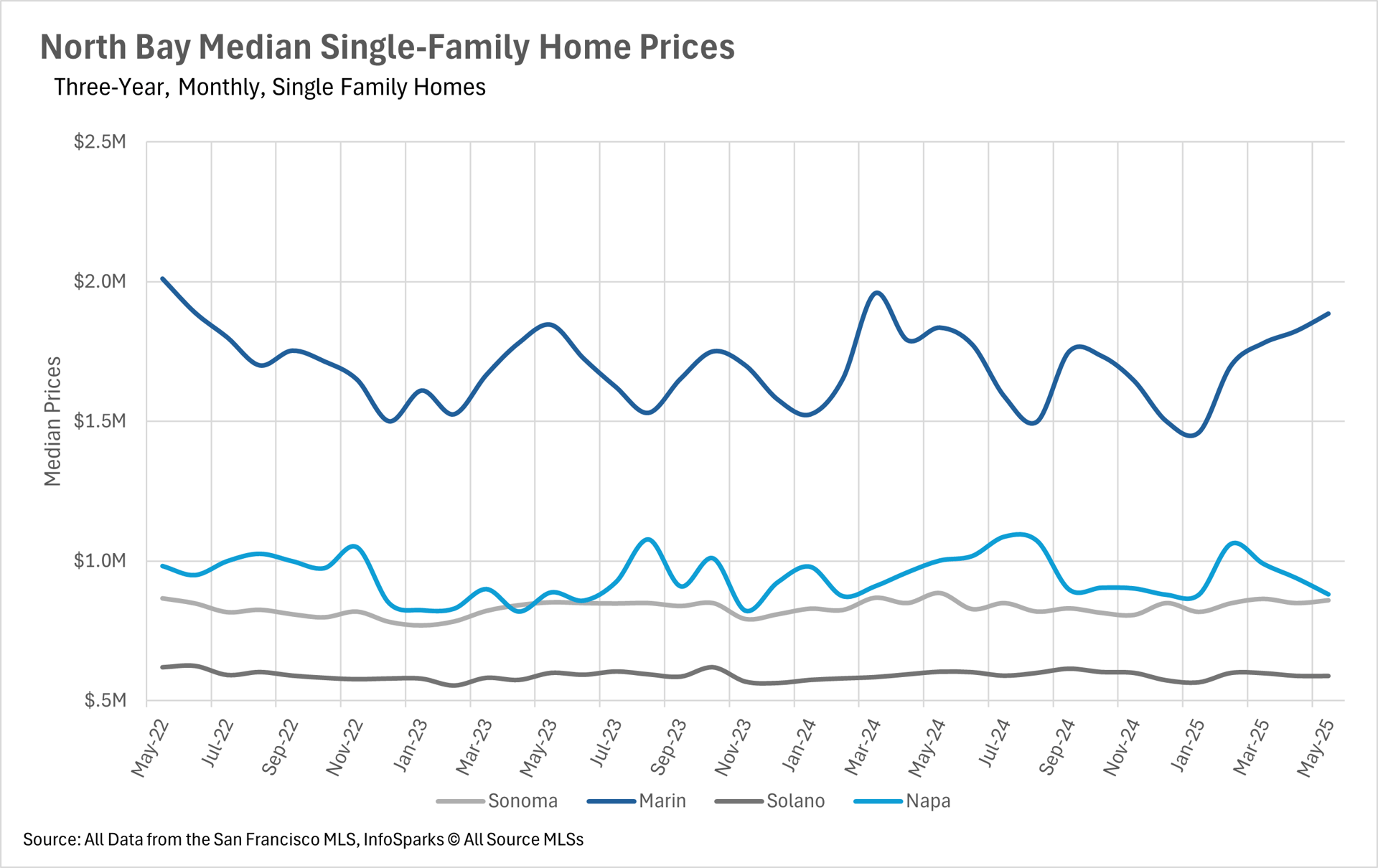

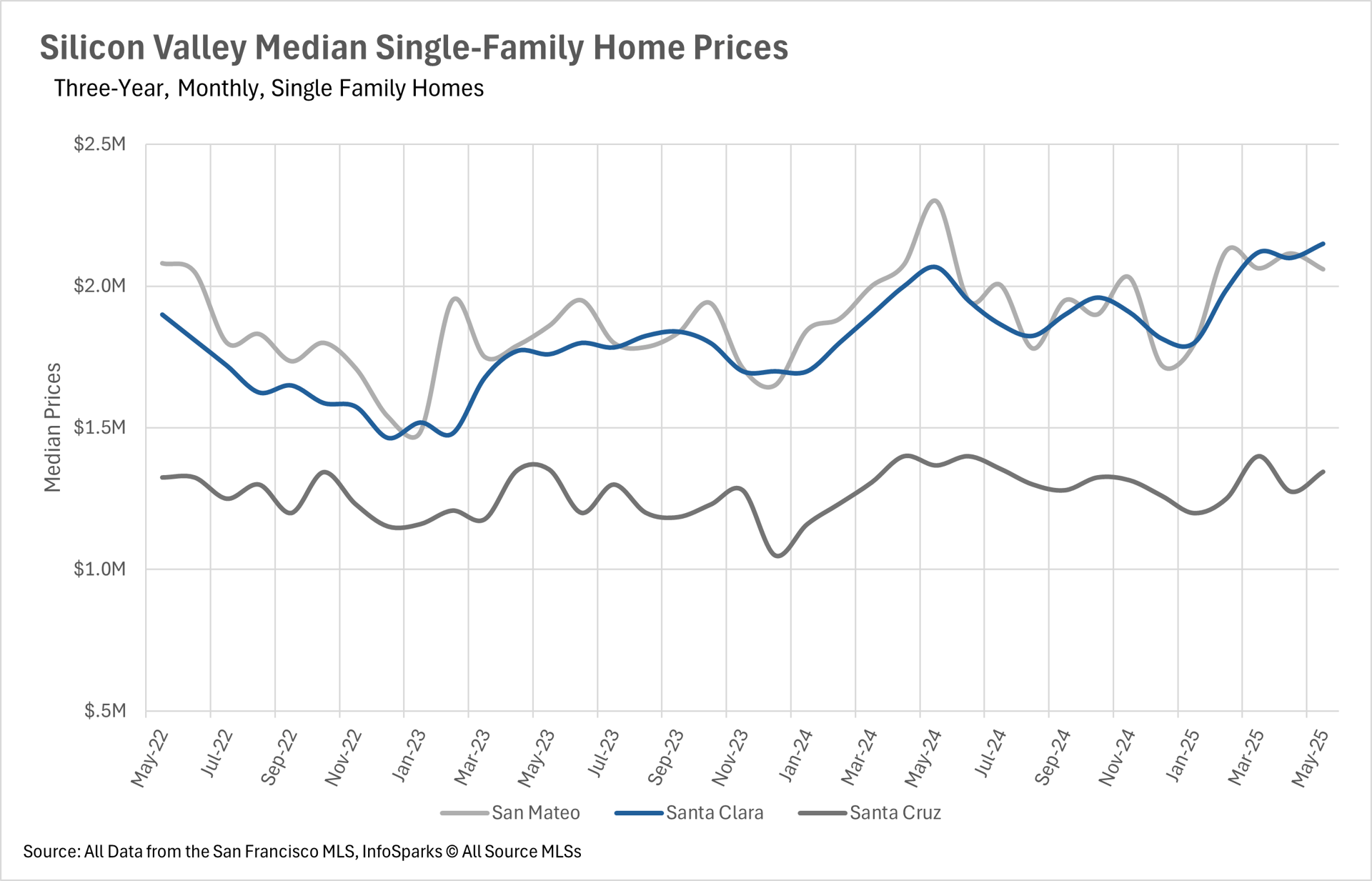

SAN FRANCISCO LEADS PRICE GROWTH WHILE OTHER REGIONS COOL

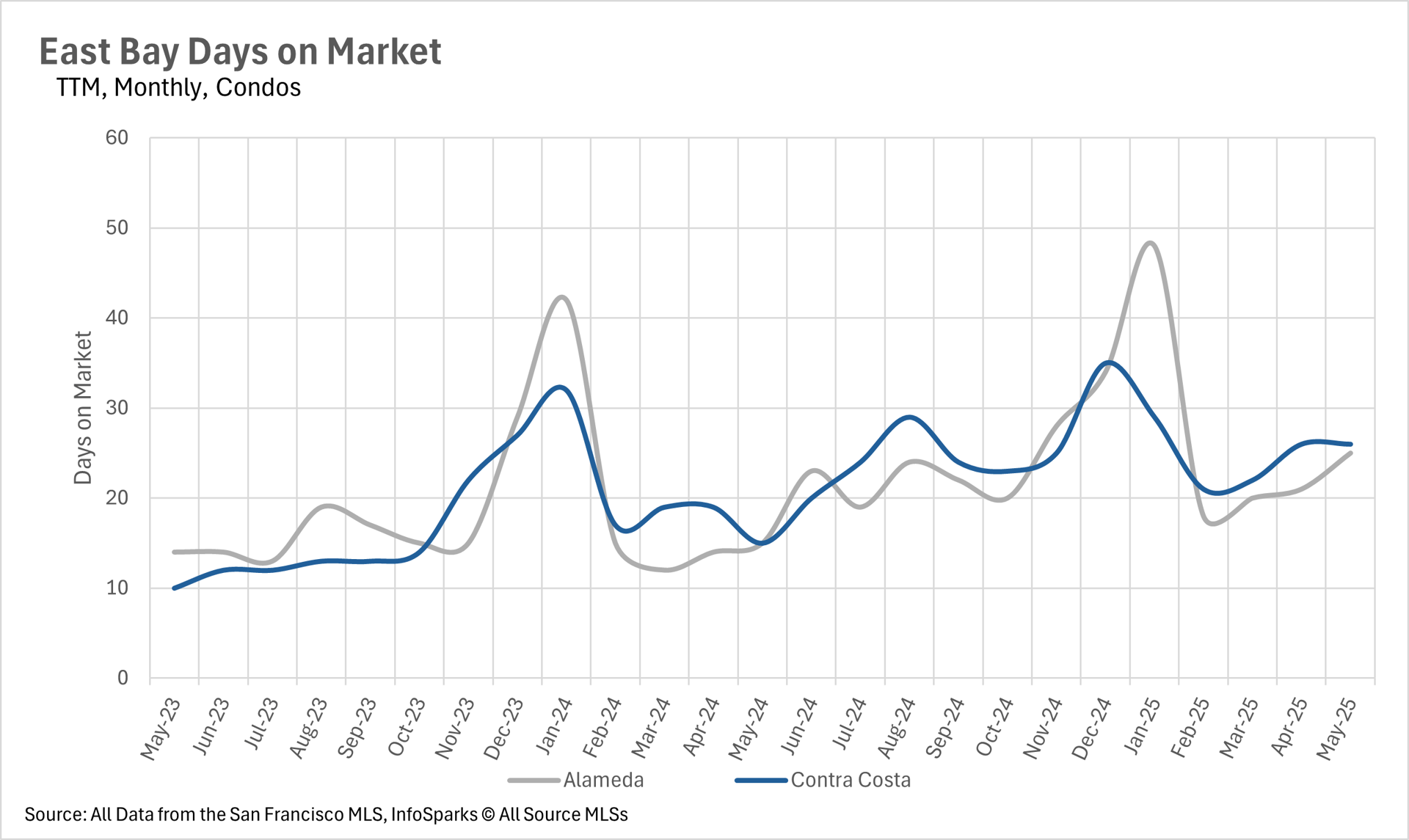

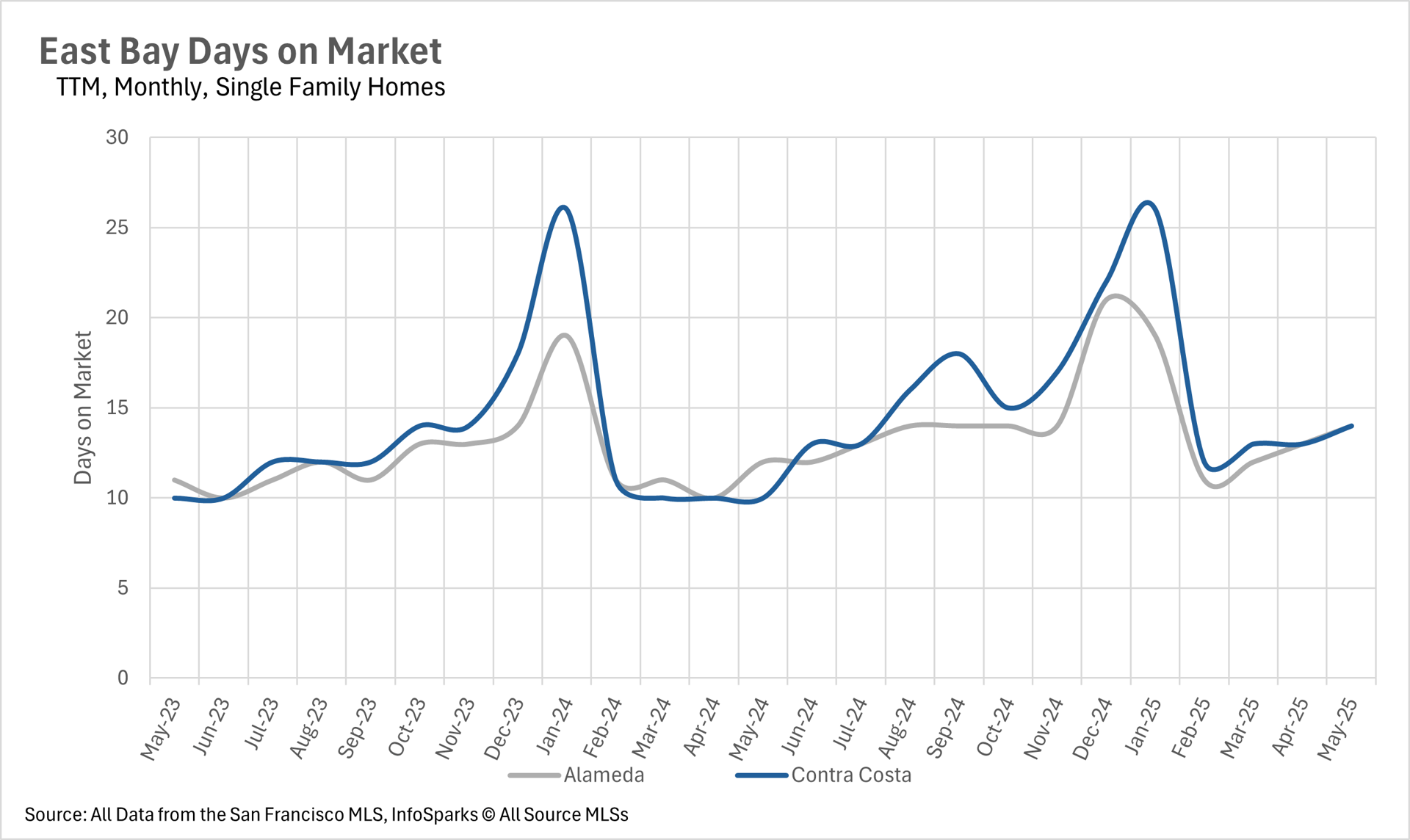

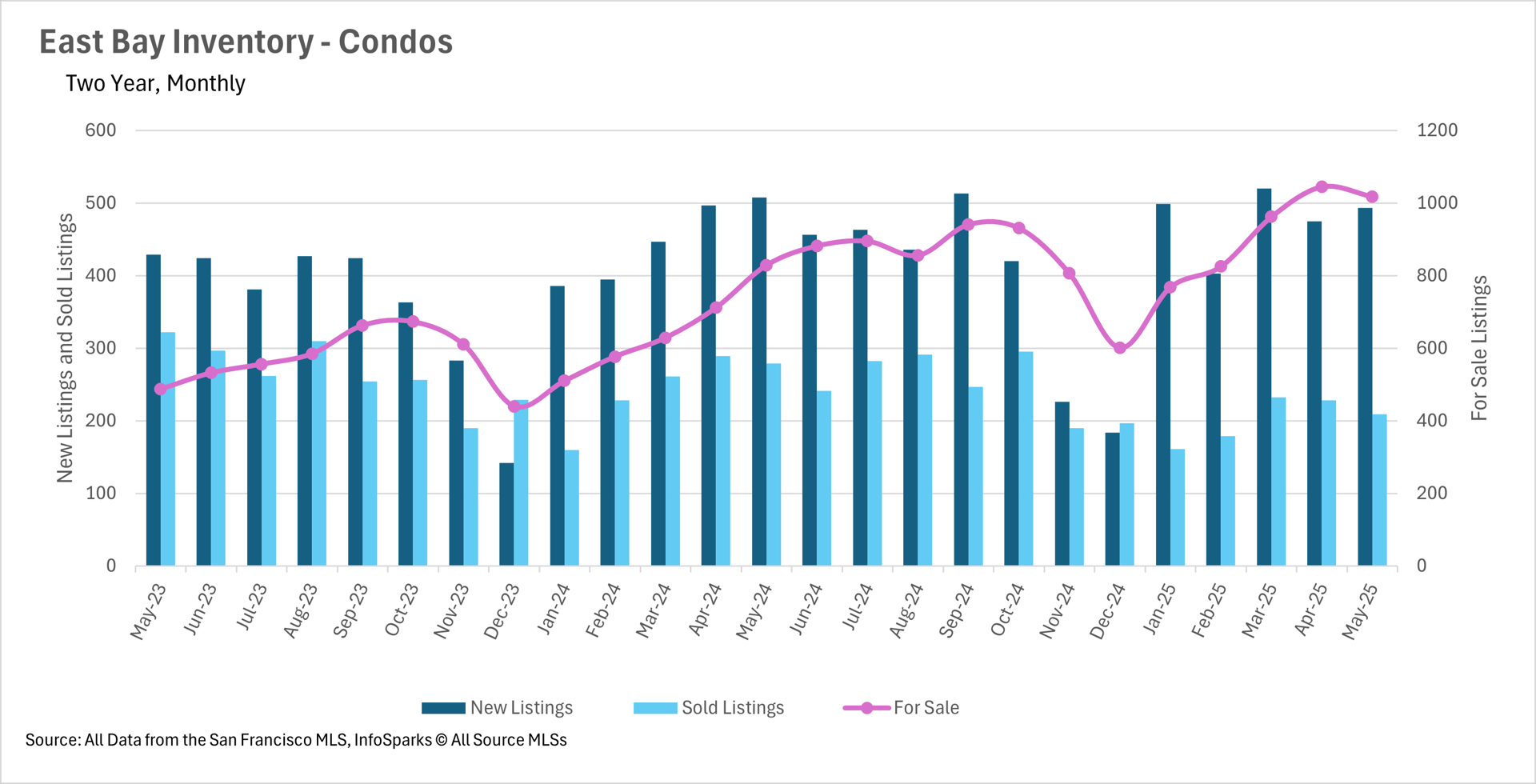

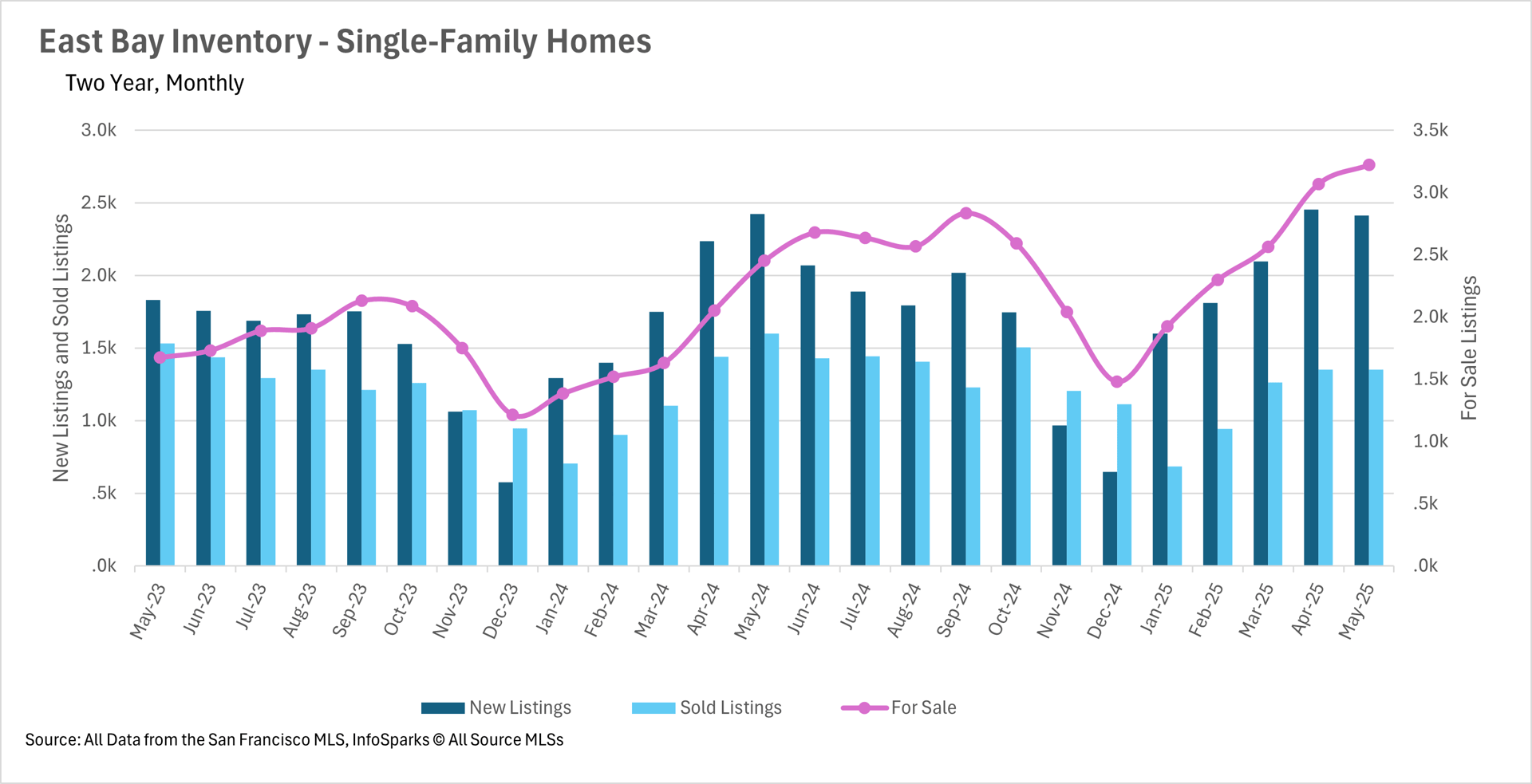

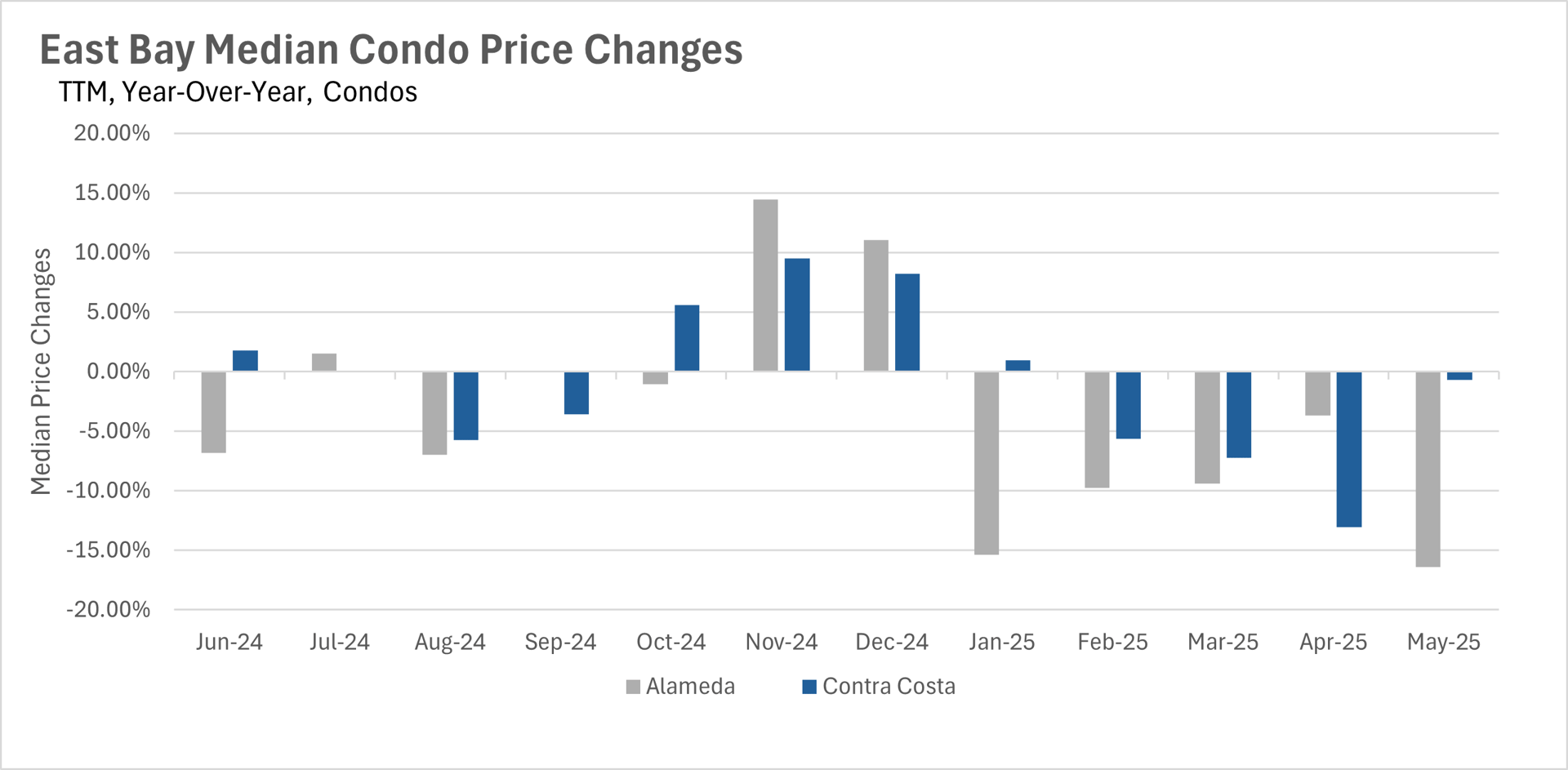

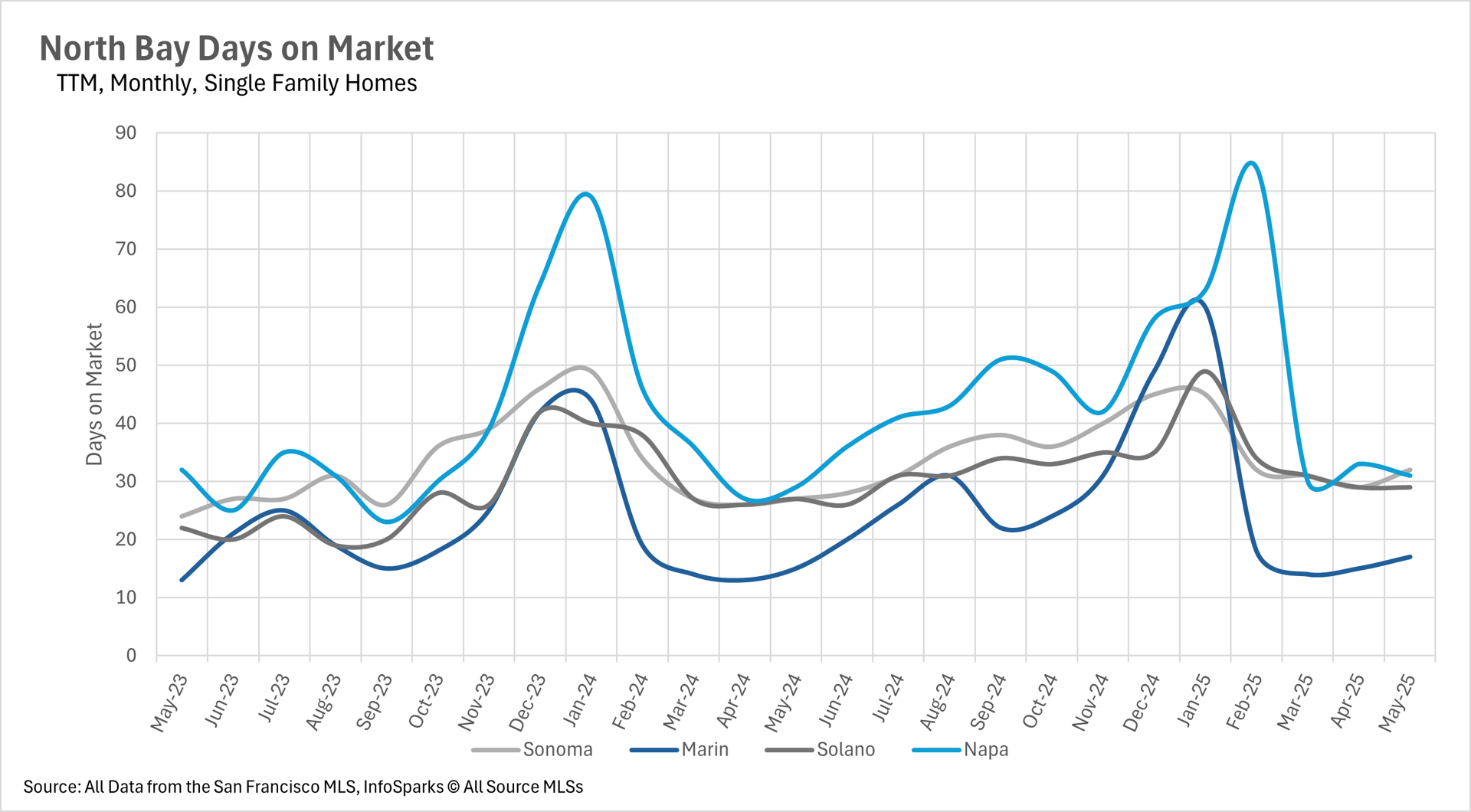

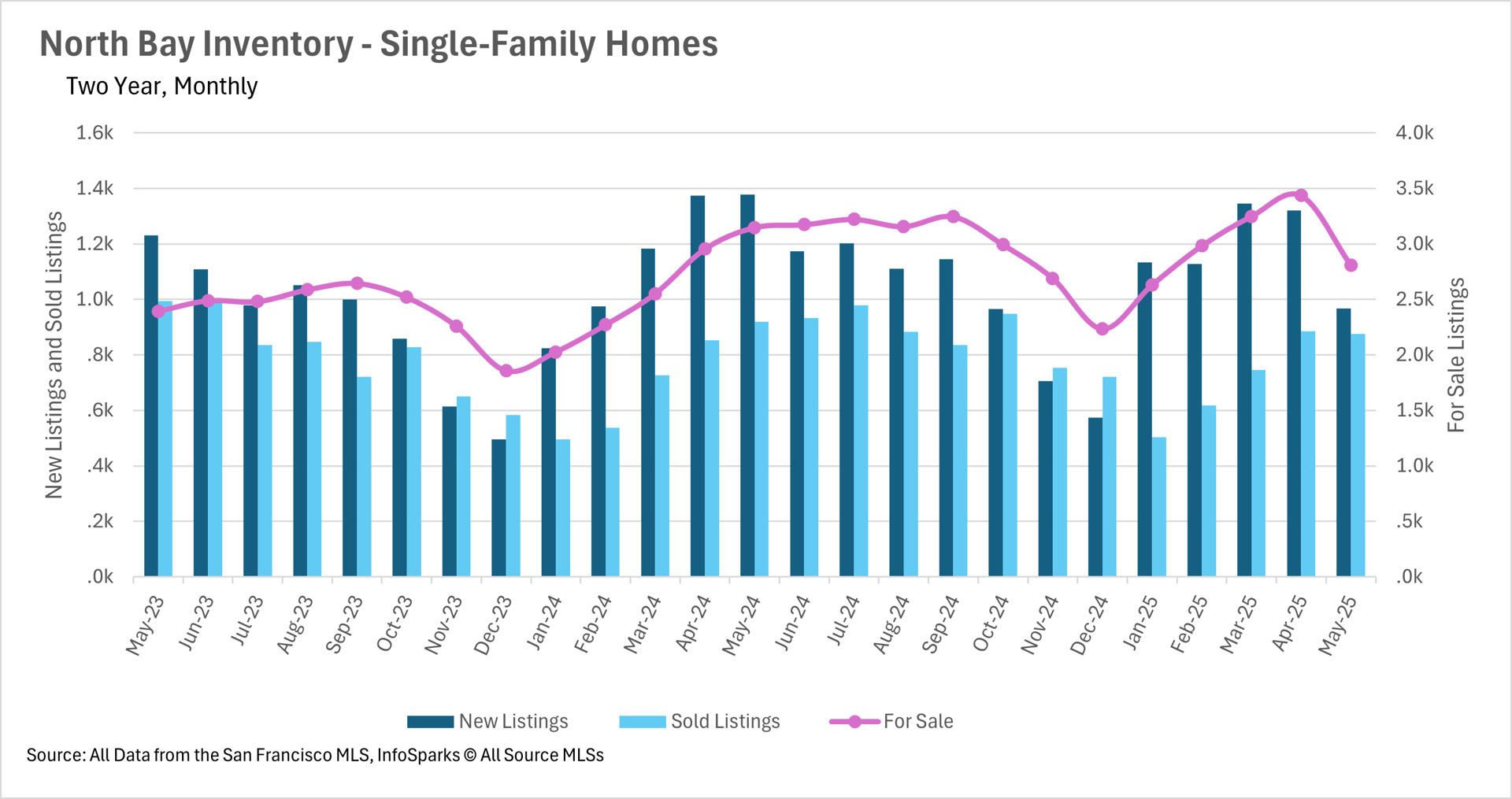

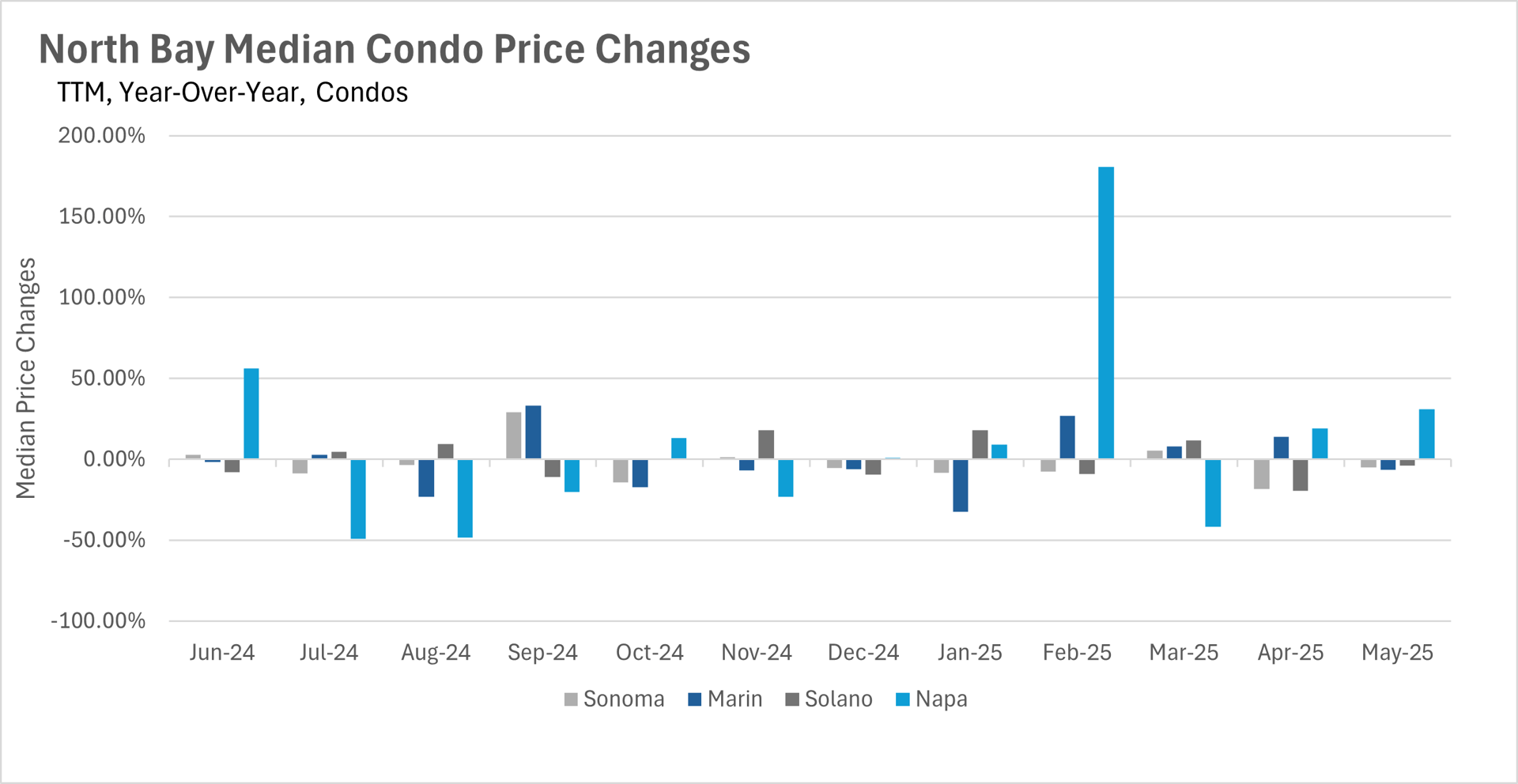

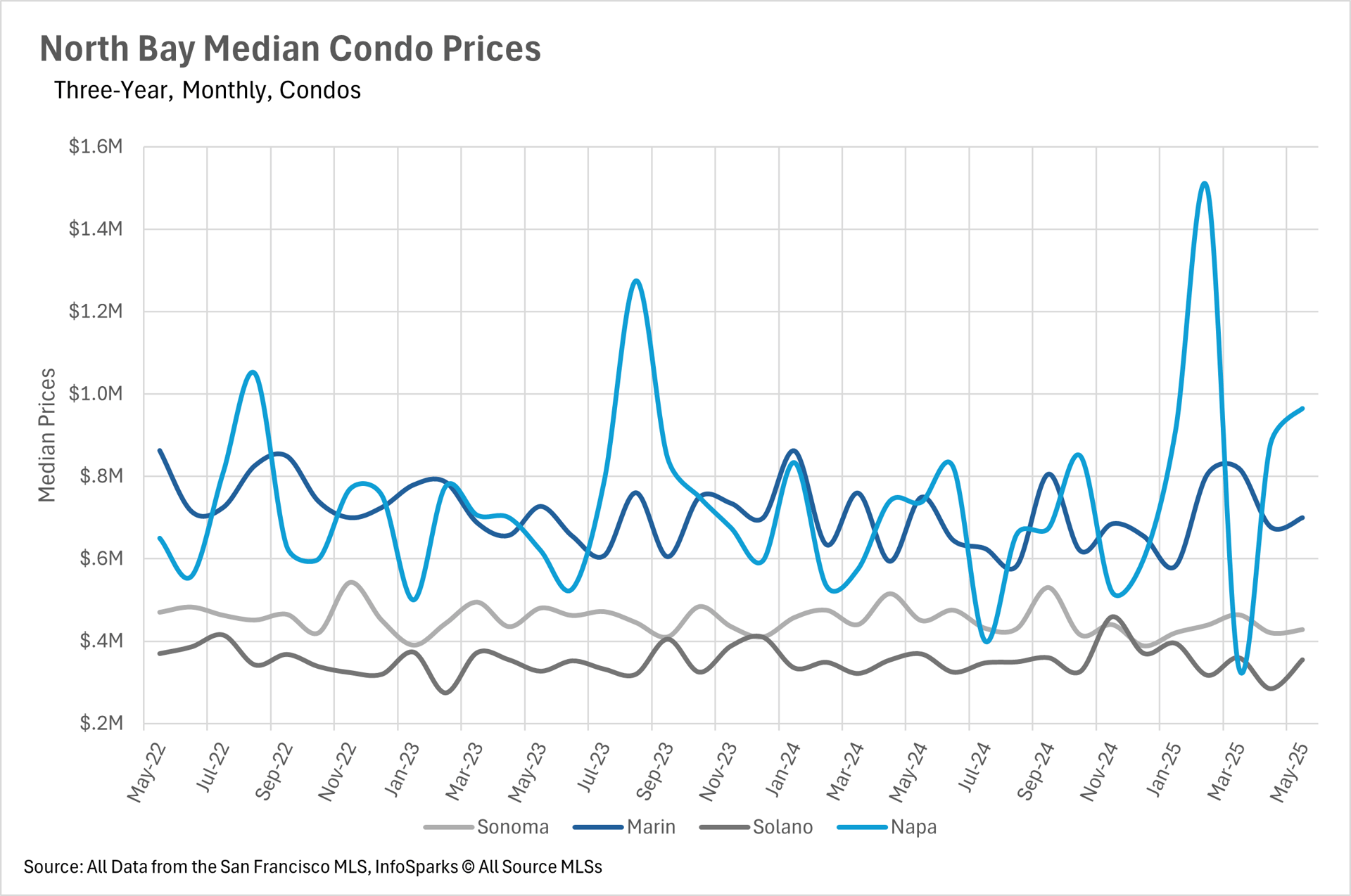

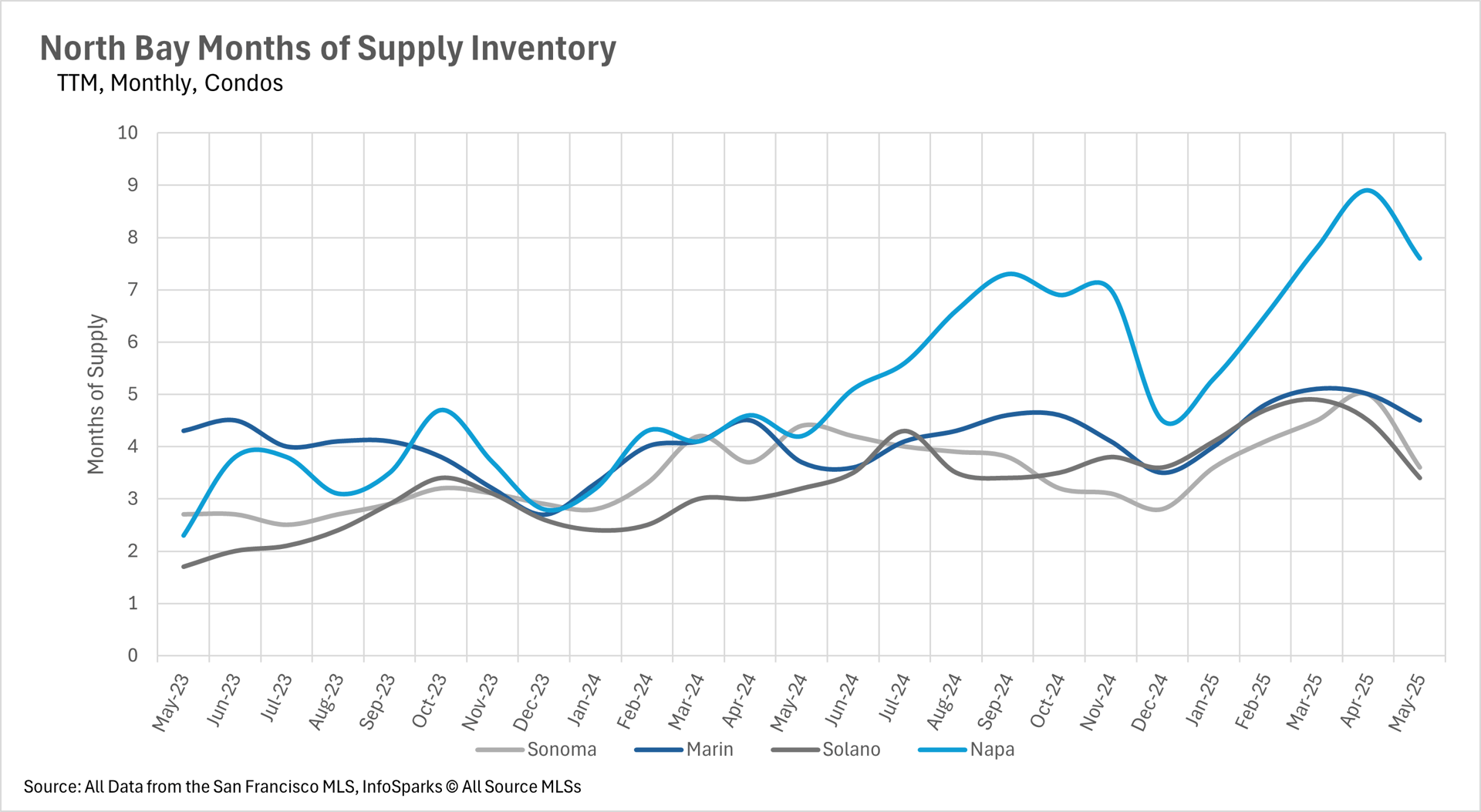

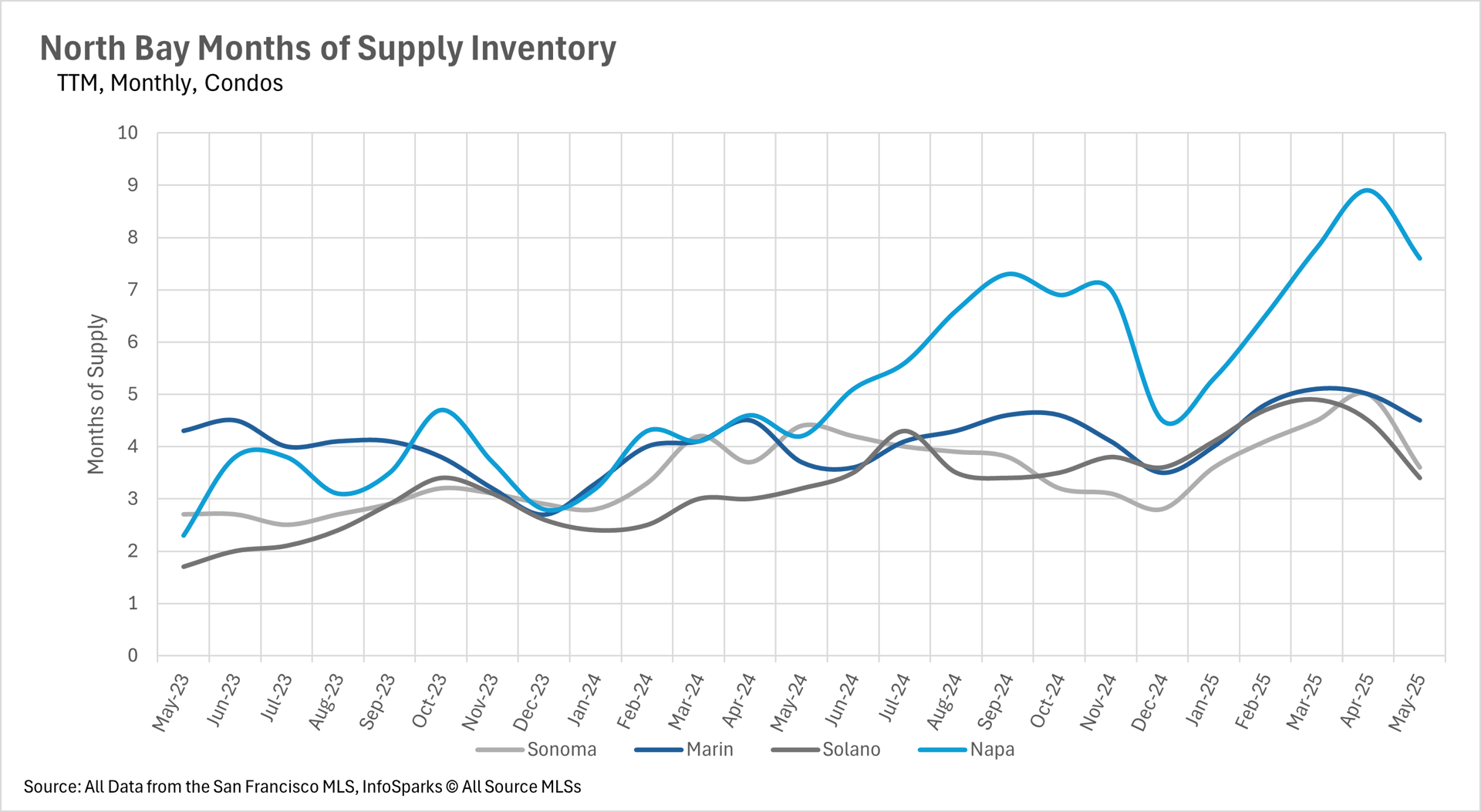

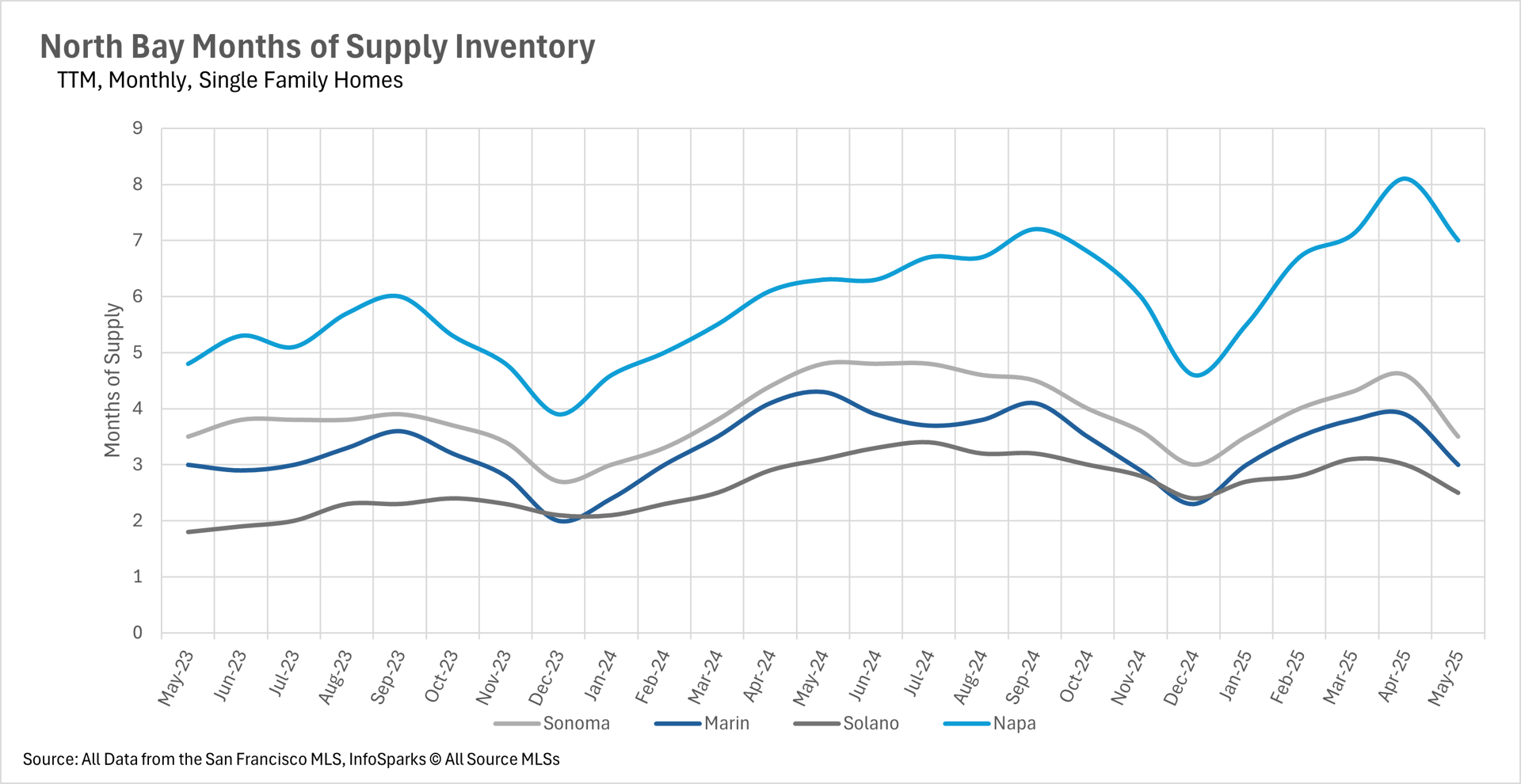

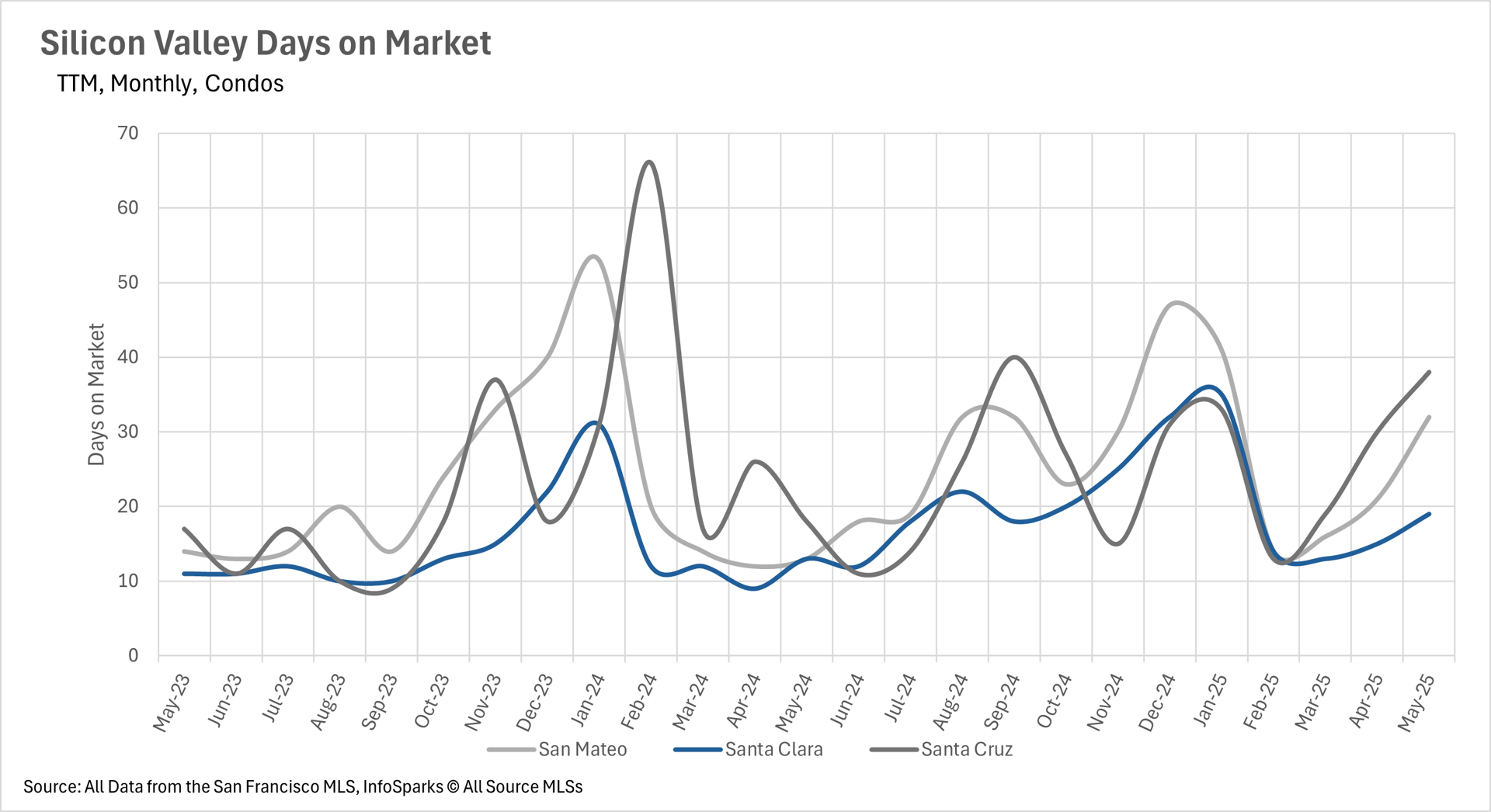

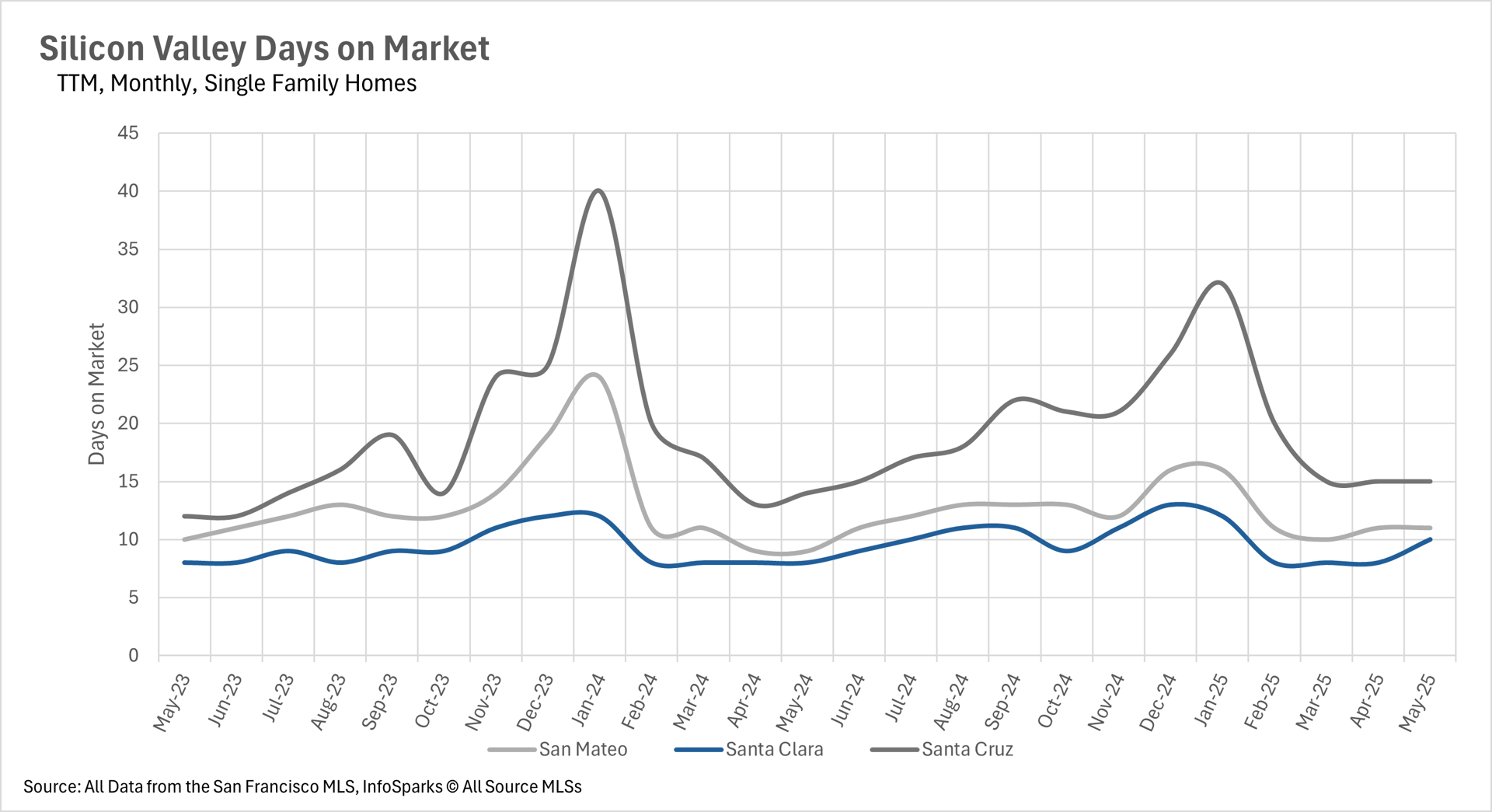

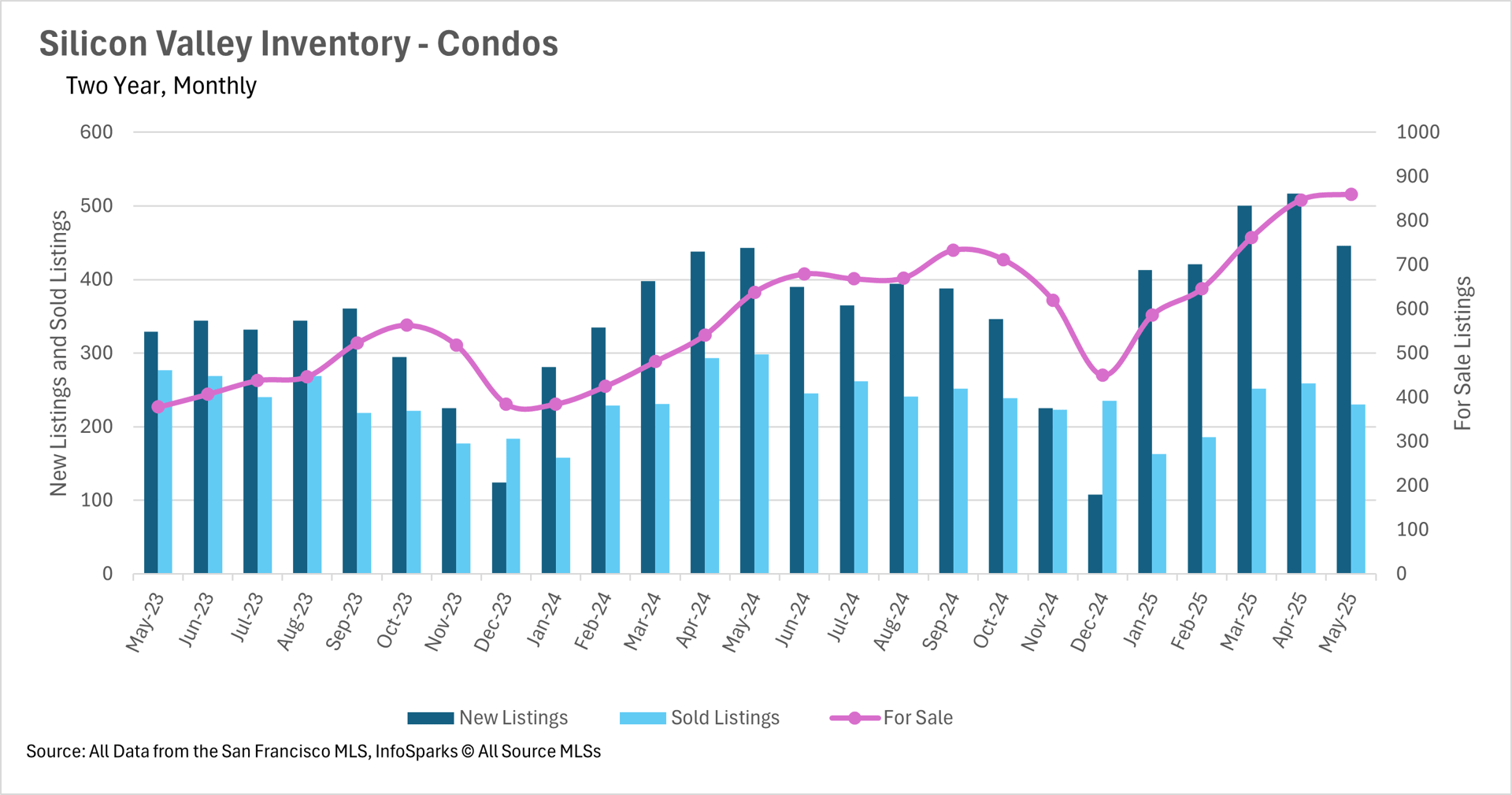

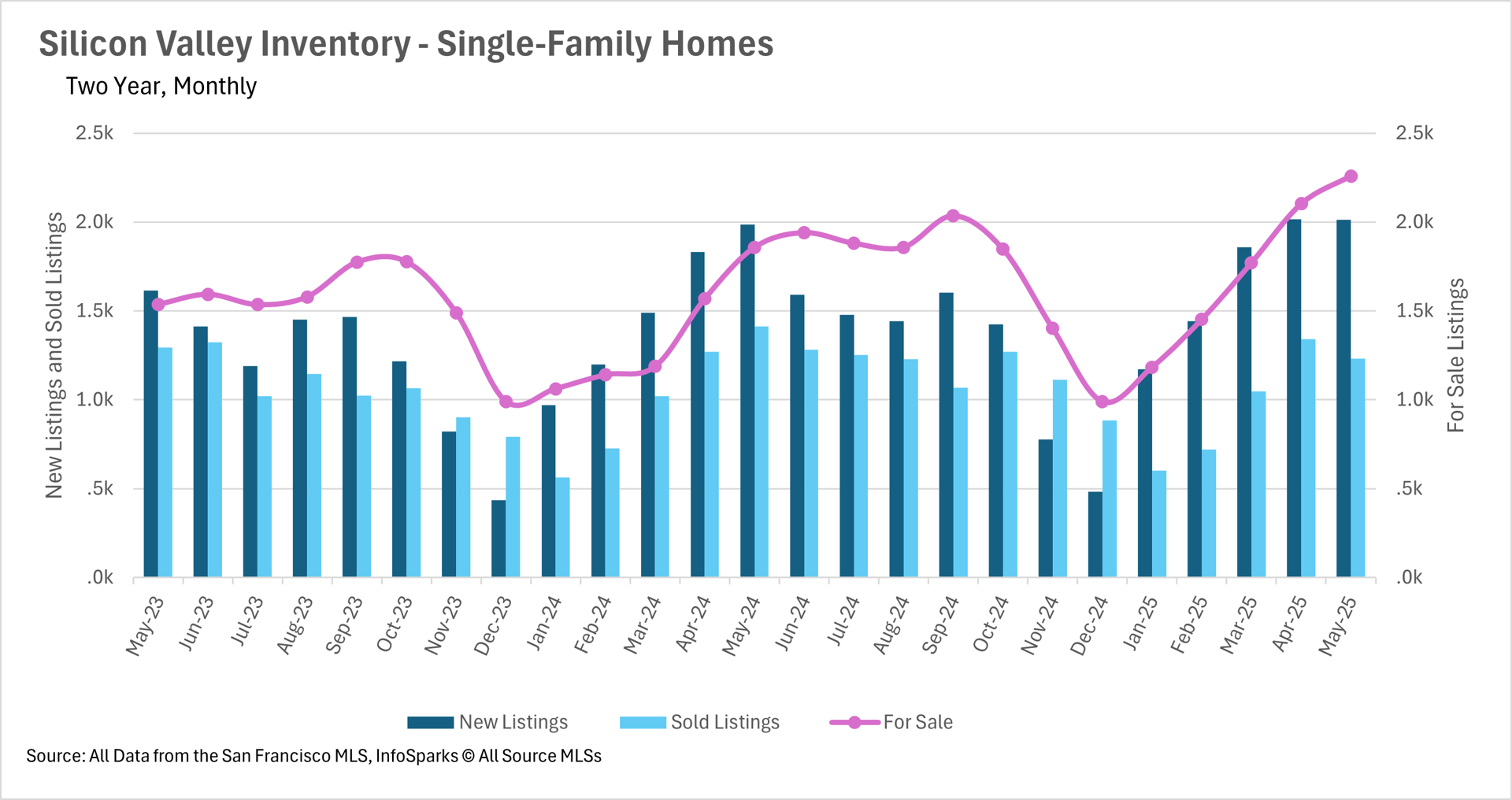

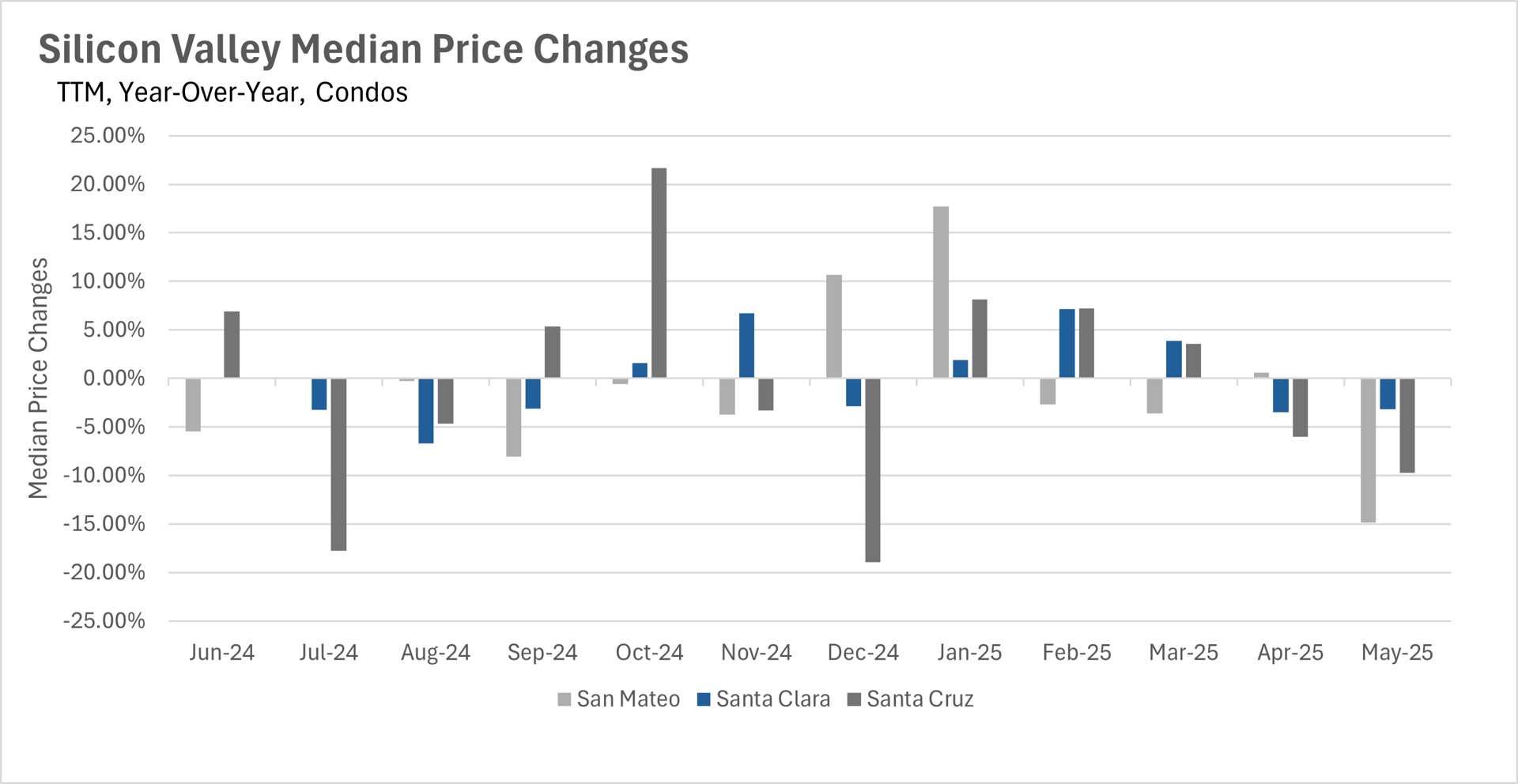

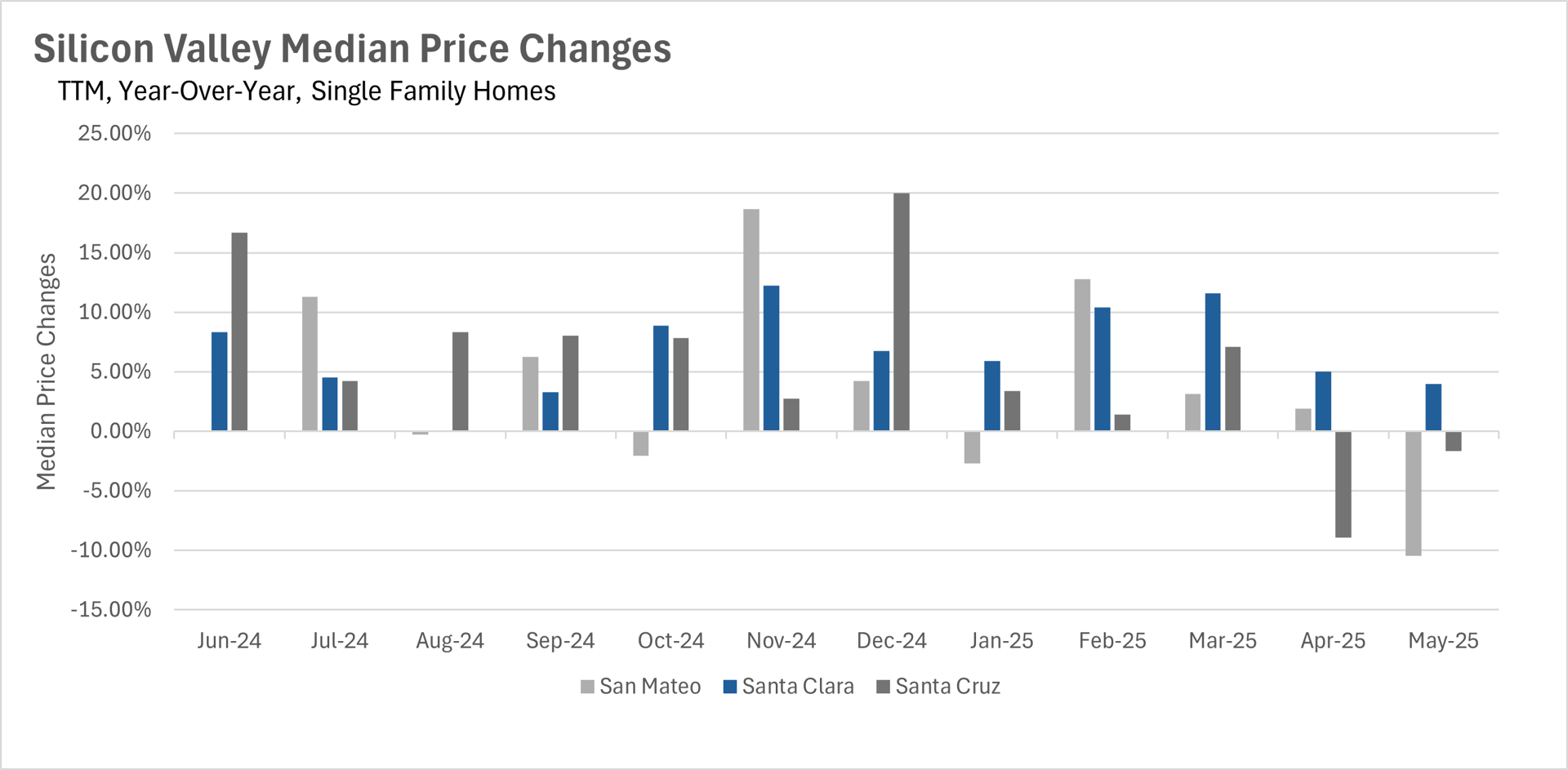

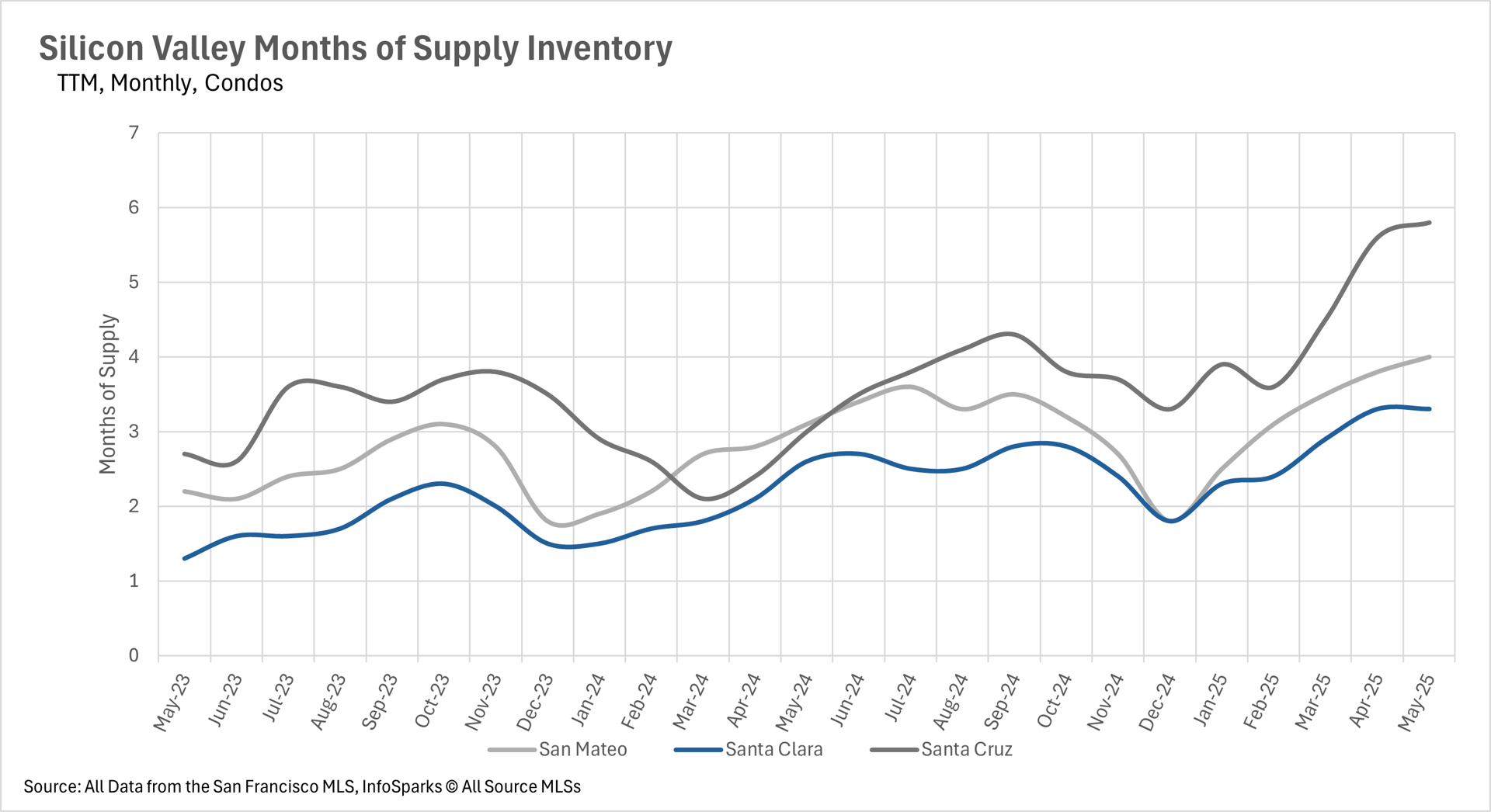

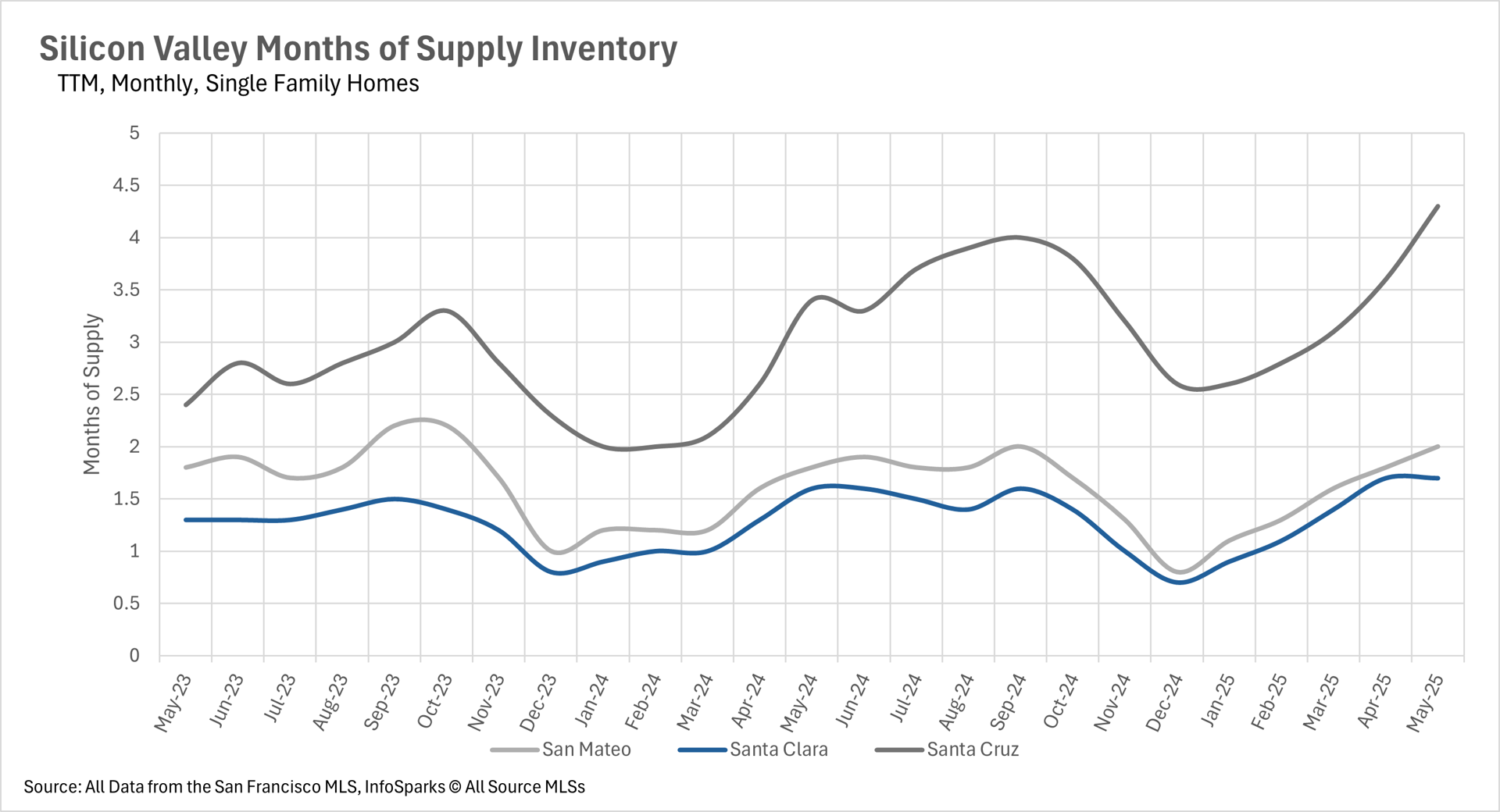

The Months of Supply Inventory (MSI) reveals a consistent Bay Area trend: single-family homes largely remain in a seller's market, while condos increasingly favor buyers.

Stay up to date on the latest real estate trends.

July 23, 2026

July 20, 2026

Low Inventory Is Keeping Sellers in Control

July 16, 2026

July 15, 2026

July 15, 2026

July 9, 2026

July 2, 2026

June 27, 2026

June 25, 2026

You’ve got questions and we can’t wait to answer them.