February '24 Market Update

Market Update

Market Update

Will consumer confidence bring back the housing market?

BIG STORY DATA

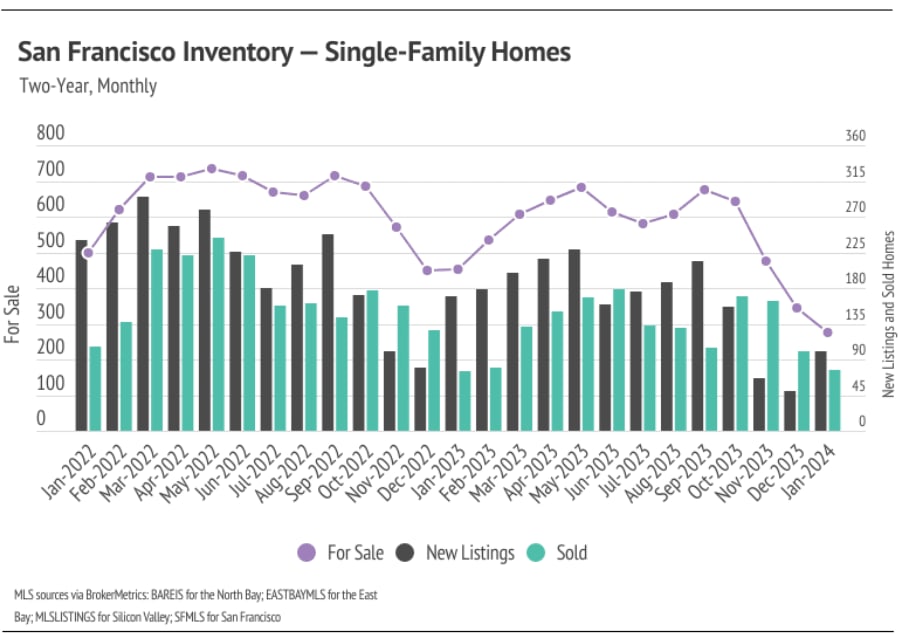

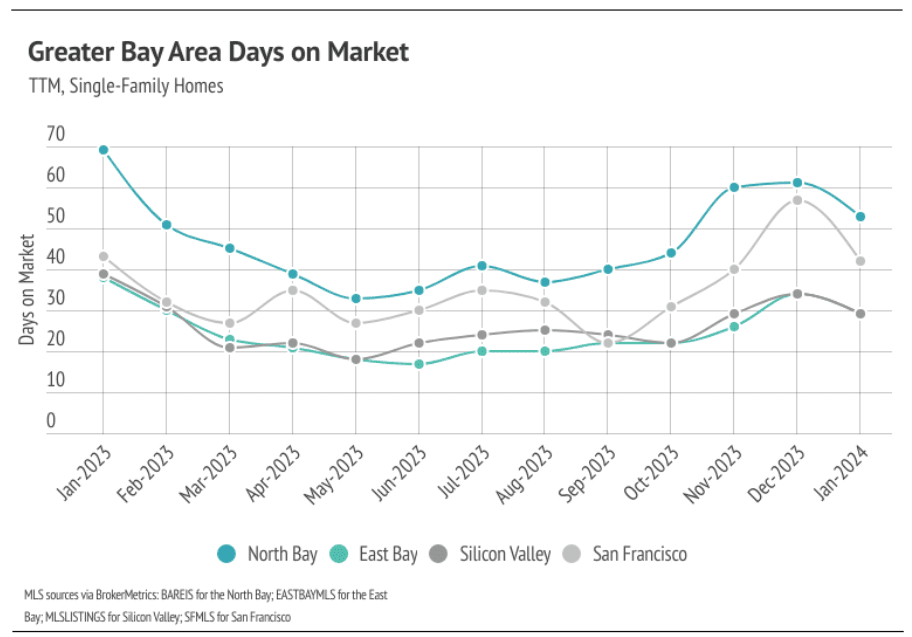

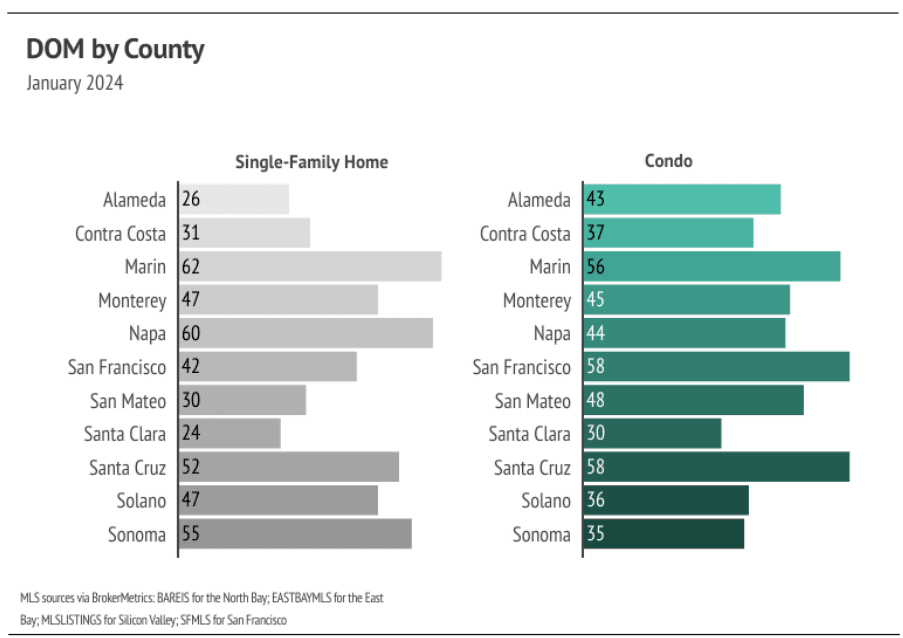

LOCAL LOWDOWN

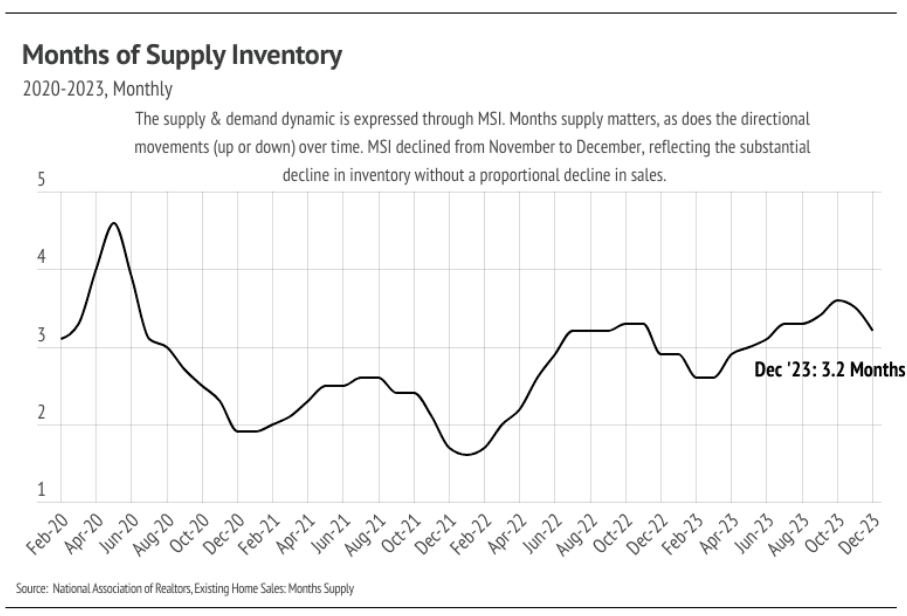

Months of Supply Inventory in January 2024 indicated a sellers’ market

Stay up to date on the latest real estate trends.

July 23, 2026

July 20, 2026

Low Inventory Is Keeping Sellers in Control

July 16, 2026

July 15, 2026

July 15, 2026

July 9, 2026

July 2, 2026

June 27, 2026

June 25, 2026

You’ve got questions and we can’t wait to answer them.