January '22 Market Update

Quick Take:

Note: You can find the charts & graphs for the Big Story at the end of the following section.

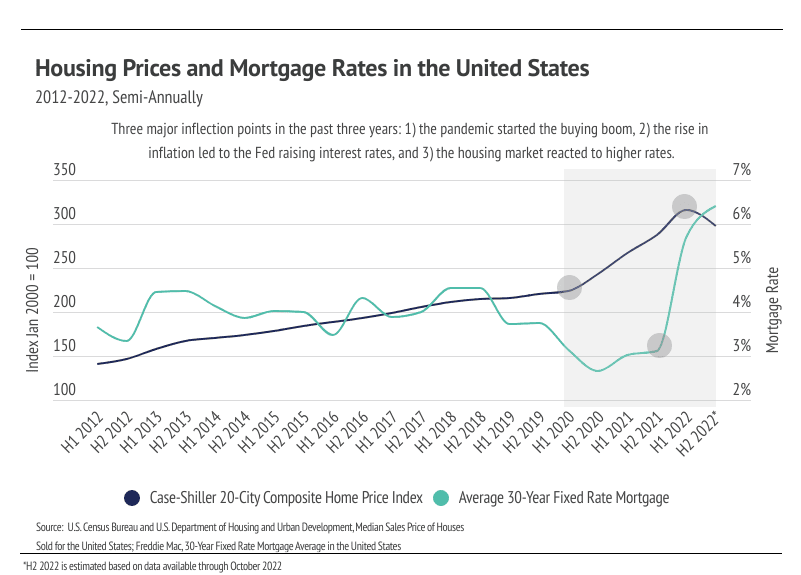

What happened yesterday has more bearing on today than what happened five years ago, so we’re shortening our lookback window to get a better understanding of what’s to come. This isn’t to say we can’t use history or that it should be dismissed entirely; rather, the pandemic set in motion a series of events that led to a different housing market, a different overall economy, and a different world when compared to pre-pandemic times. So, as many do in the new year, we reflect on the last year and envision what’s to come.

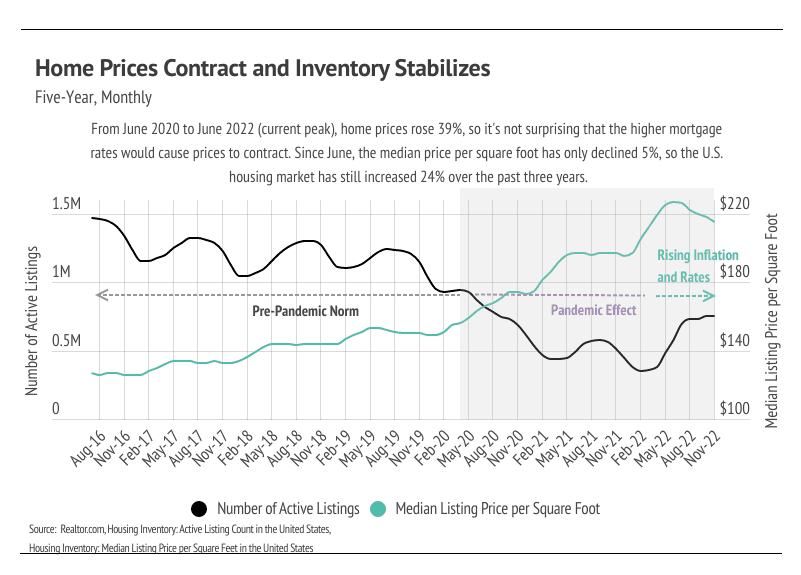

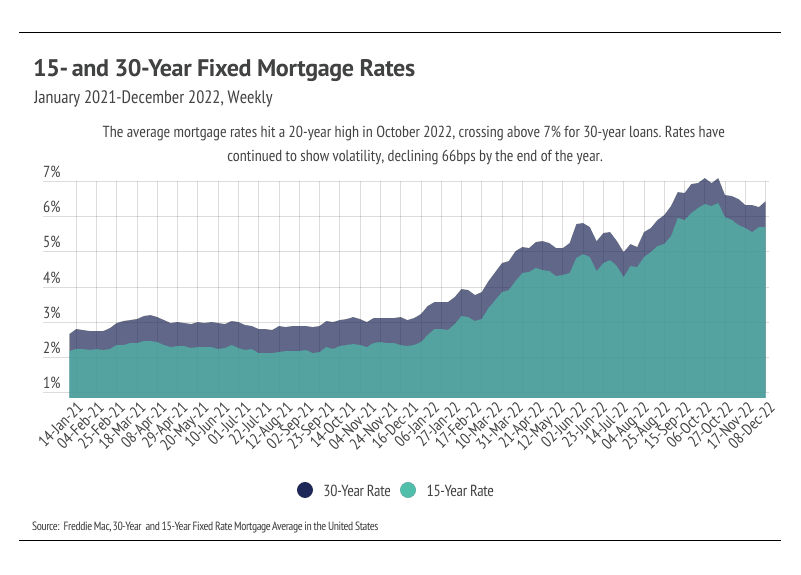

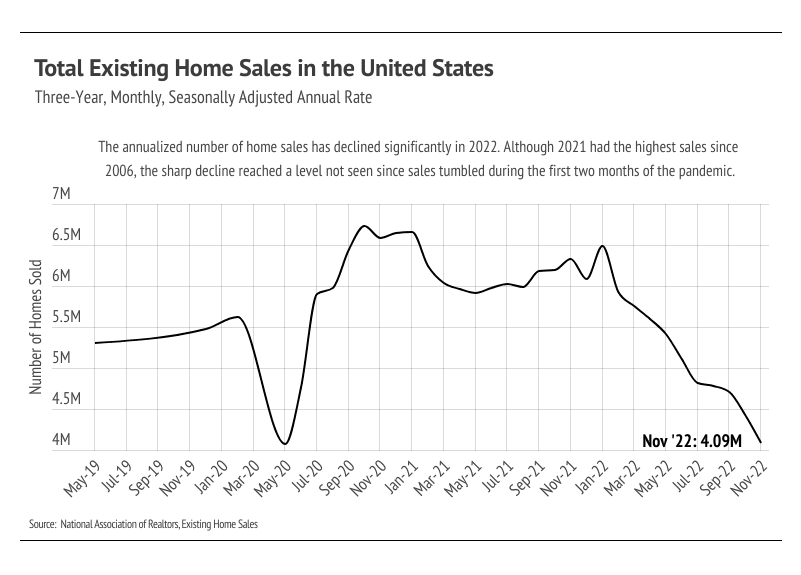

The economic factors are mixed, suggesting that the market is balancing out. Demand had nowhere to go but down after the rise in interest rates and the buying frenzy between 2020 and 2021. (The average homeowner stays in their home for about eight years.) The supply of homes is still about 20% below pre-pandemic levels, so the drop in demand brought the market closer to balance. In 2023, we expect a return to seasonal trends — price and inventory growth in the first half of the year and contraction in the back half — but at relatively lower levels, meaning fewer new listings and fewer sales overall.

The U.S. housing market has certainly shifted throughout the year, and we must recognize the current conditions homebuyers and sellers face. Of course, different regions vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage of your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

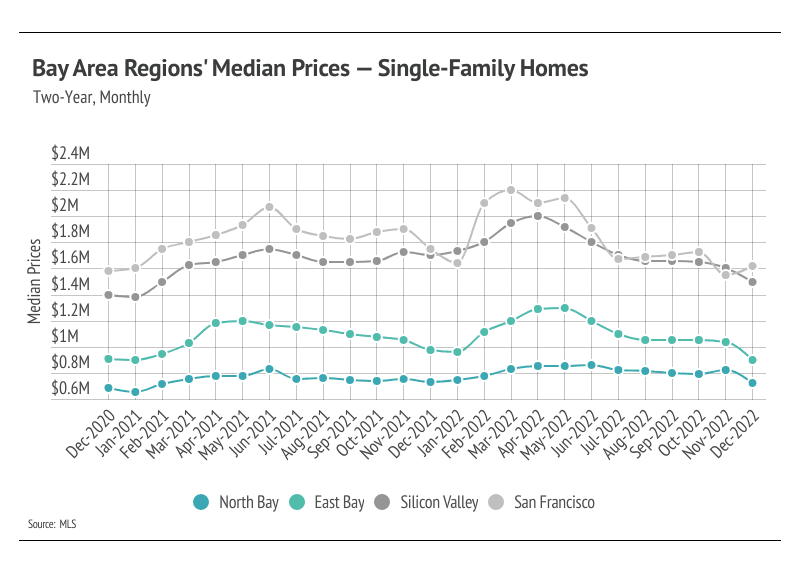

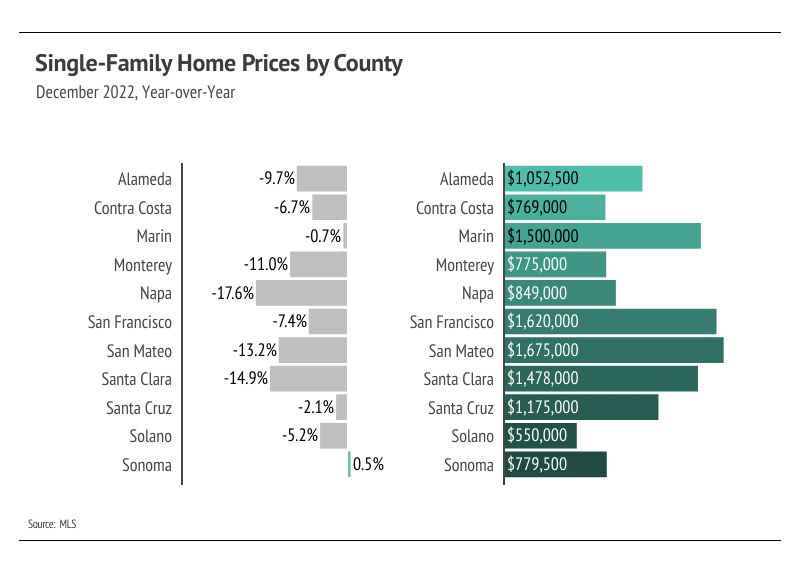

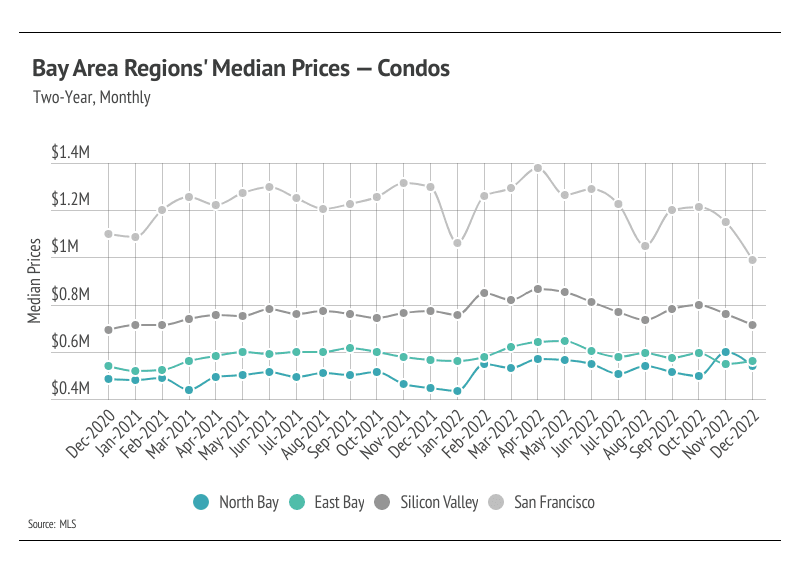

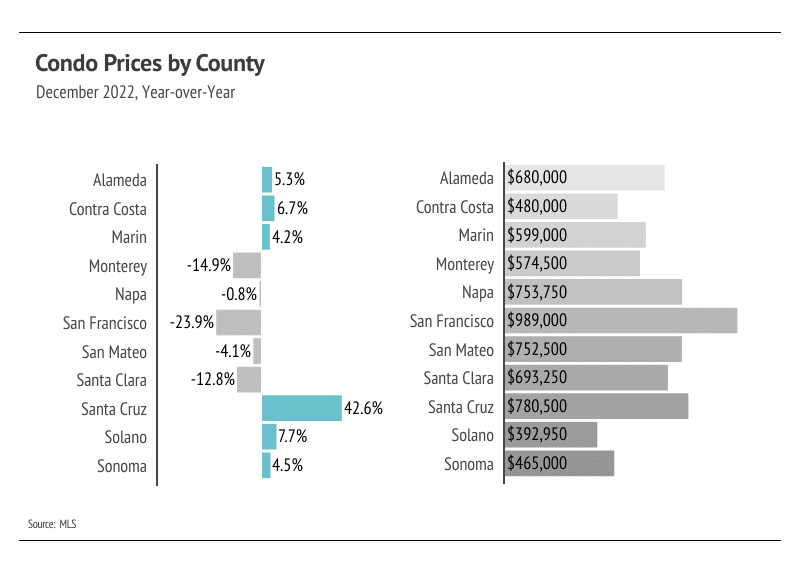

As we mentioned in the Big Story, the market has cooled for both buyers and sellers, largely because of higher interest rates. As we enter the new year, the market feels familiar — but from the era before 2020. Demand in the Bay Area is evergreen, so we aren’t worried about matching buyers and sellers. That said, sellers likely won’t be getting multiple offers the second the home hits the market again anytime soon. To make a long story short, there is definitely less stress on the buying side of the market. Prices will most likely increase in 2023, but at a more modest rate of around 5-6%, which makes for a much healthier market than what occurred over the past three years. Overall, single-family home and condo prices increased over the past two years, even with the declines from the peaks reached in 2022, with the exception of Marin and San Francisco condo prices, which are lower than they were in 2020. Without any signs of interest rates dropping, we’re entering a stage of slower, longer-term growth.

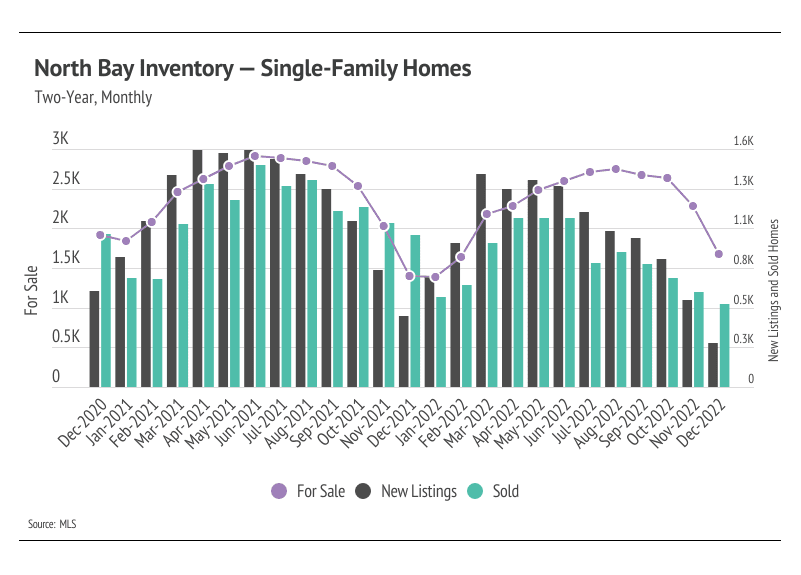

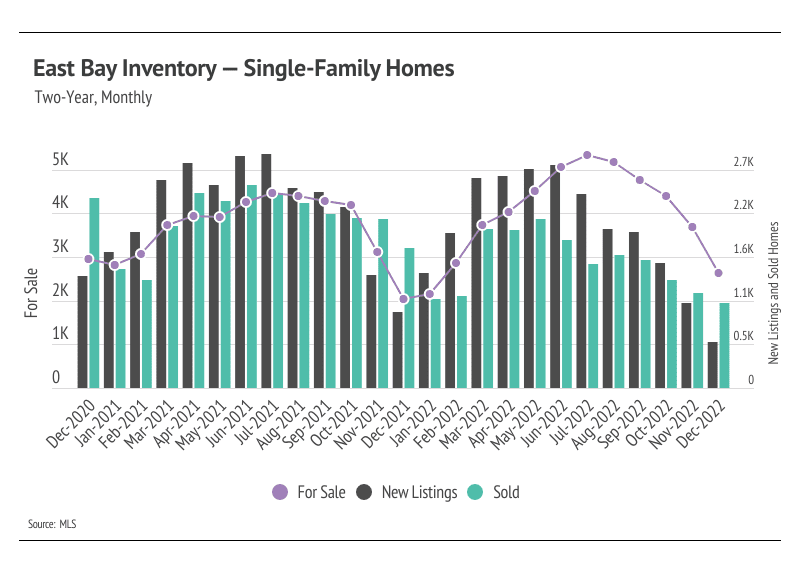

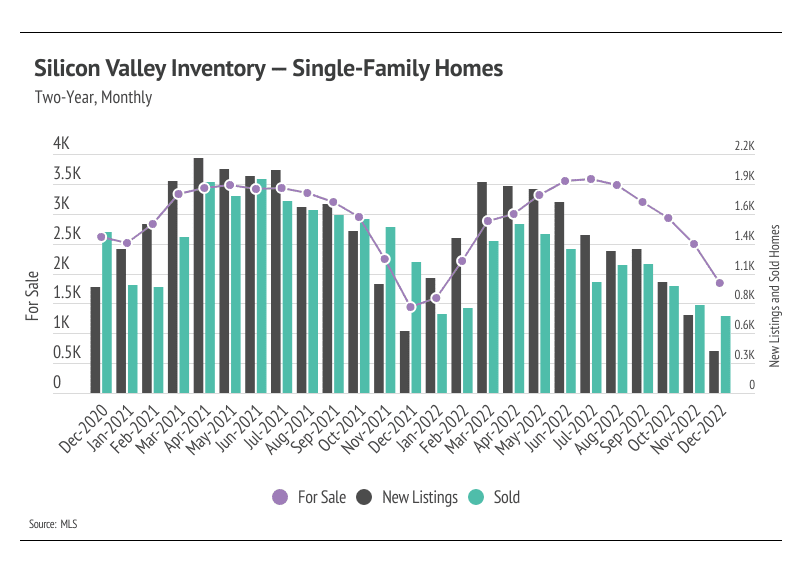

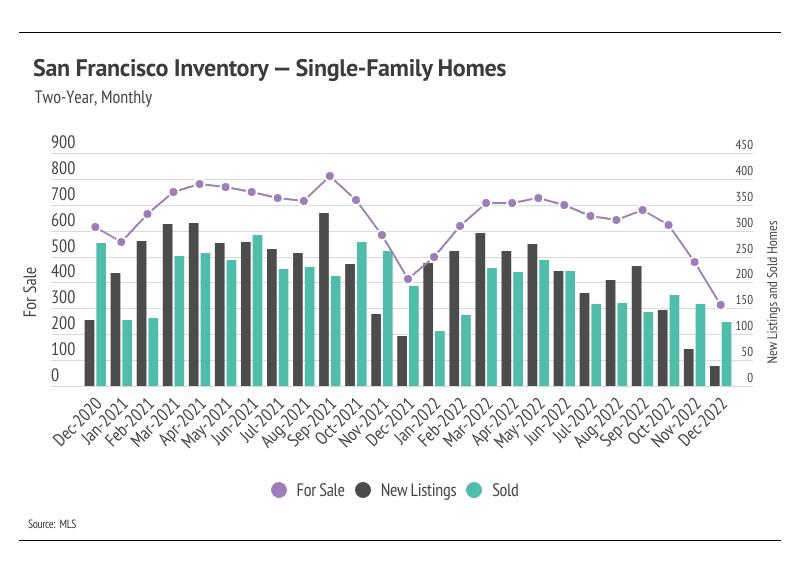

When we look at single-family home inventory levels for 2021 and 2022 side by side, it’s immediately apparent that inventory levels in any given month were fairly similar, but the markets were quite different. The 2021 market was defined by the high demand and high number of new listings, which helped drive a huge number of sales. New listings and sales rose and fell in tandem, but sales significantly outpaced new listings at the end of 2021, which dropped inventory to extremely low levels. In 2022, however, far fewer listings came to market, especially in the second half of the year. Fewer homes and the rising rate environment dropped demand, bringing the market closer to balanced between buyers and sellers in the second and third quarters, but the sharp decline in new listings and steady sales reversed that trend in the fourth quarter. The condo market had a simpler story in that fewer new listings came to market without a proportional decline in sales, so inventory remained historically low. This year, we expect the housing market to look a lot more like 2022 than 2021.

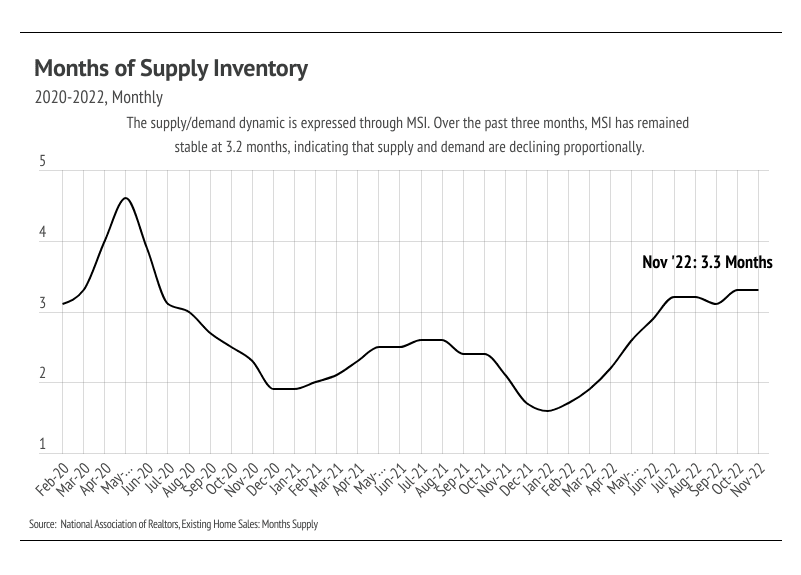

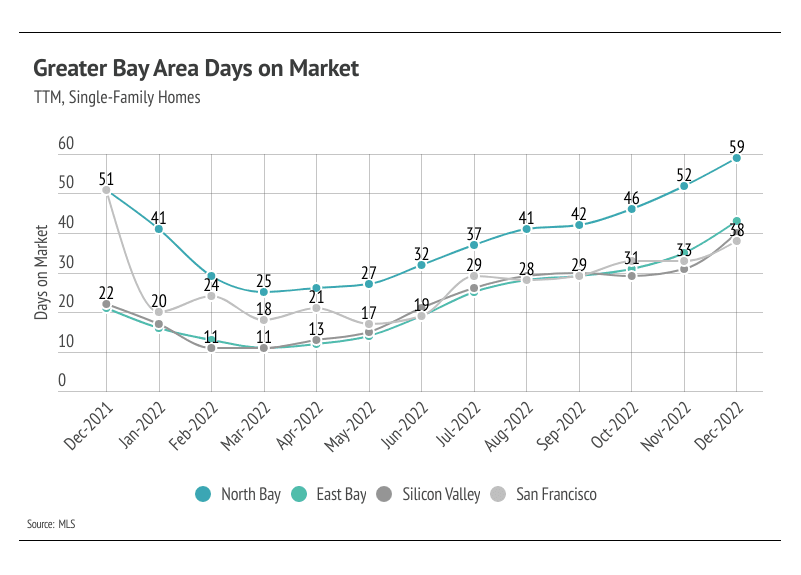

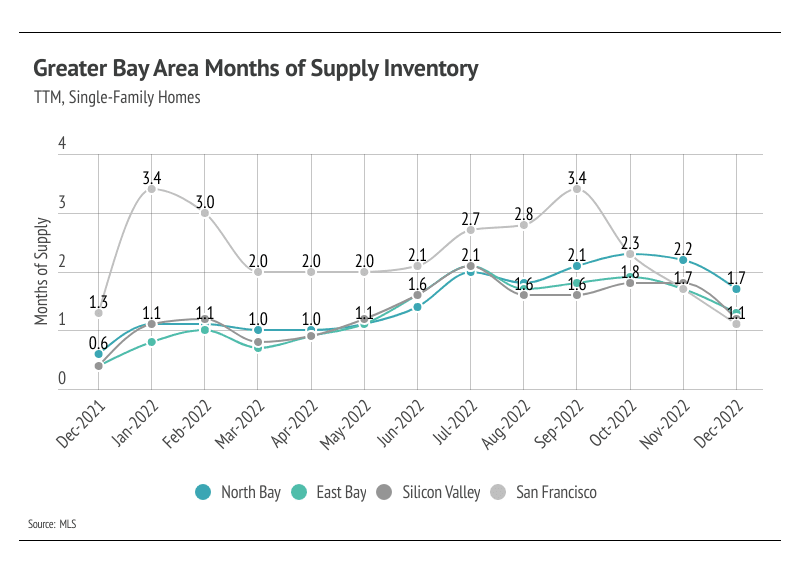

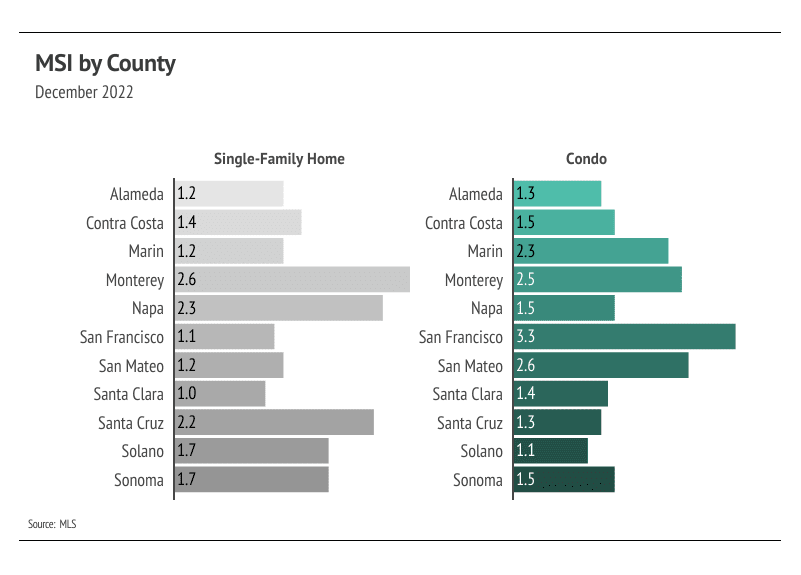

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI trended higher in the spring and summer of 2022, but only San Francisco MSI flirted with a balanced market before dropping in the fourth quarter, indicating the Bay Area is still a sellers’ market. Despite the changing economic environment, we are comfortable saying that the market will still favor sellers for at least the first quarter of 2023.

Stay up to date on the latest real estate trends.

April 28, 2026

April 23, 2026

April 21, 2026

April 20, 2026

April 16, 2026

April 2, 2026

March 25, 2026

March 24, 2026

March 24, 2026

You’ve got questions and we can’t wait to answer them.