January 2025: Silicon Valley Real Estate Market Insights

Market Update

Market Update

ELEVATED RATES ARE HERE TO STAY

Economic (policy) uncertainty elevated mortgage rates

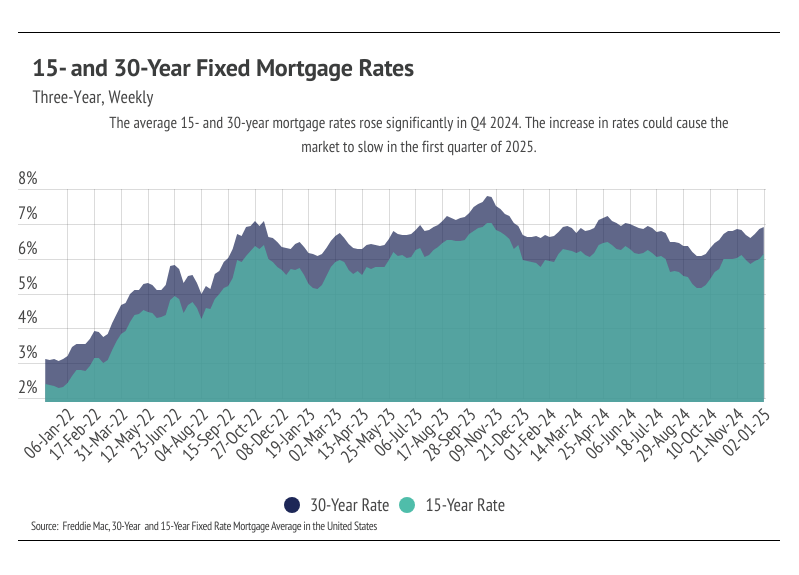

The Federal Reserve cut interest rates by 1% in 2024, but mortgage rates remain high, with the average 30-year fixed-rate mortgage reaching 6.91% on January 2, 2025, its highest in six months. This is due to external factors like economic growth, inflation concerns, and 10-year Treasury bond yields. Economists, including Lawrence Yun of the National Association of Realtors, expect mortgage rates to stay elevated between 6% and 7% in 2025, averaging around 6.5%.

Economic uncertainty persists as President-elect Donald Trump’s proposed policies, including tariffs and tax cuts, may reignite inflation. If inflation rises, the Fed might halt further rate cuts, though analysts suggest some of Trump’s proposals could be strategic rather than definite. The Fed projects two additional rate cuts for 2025, down from the four initially planned, as inflation trends remain cautious.

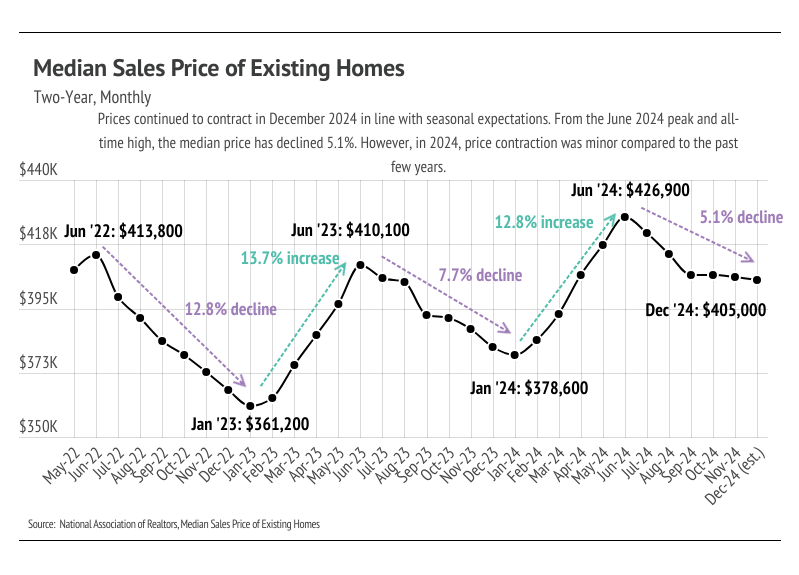

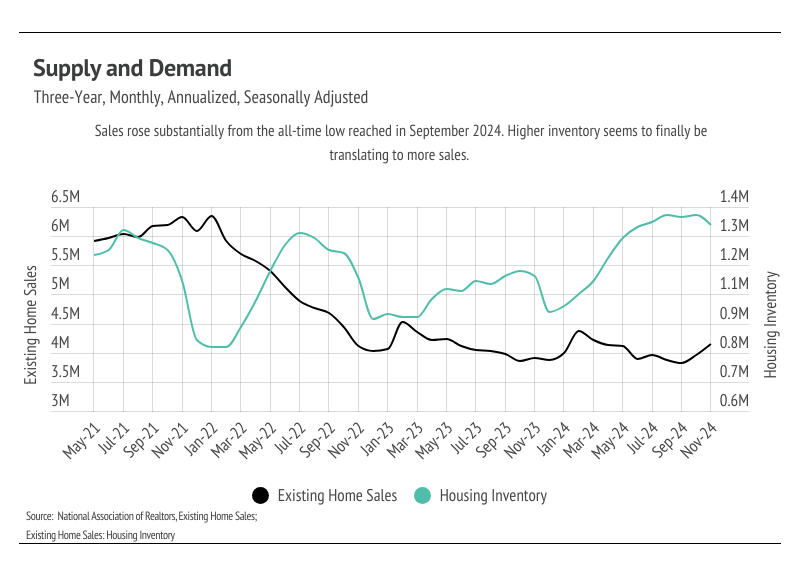

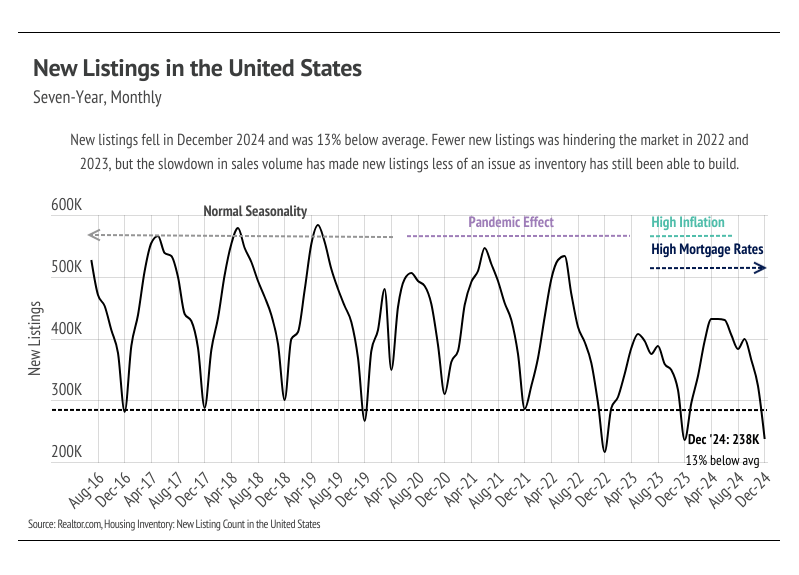

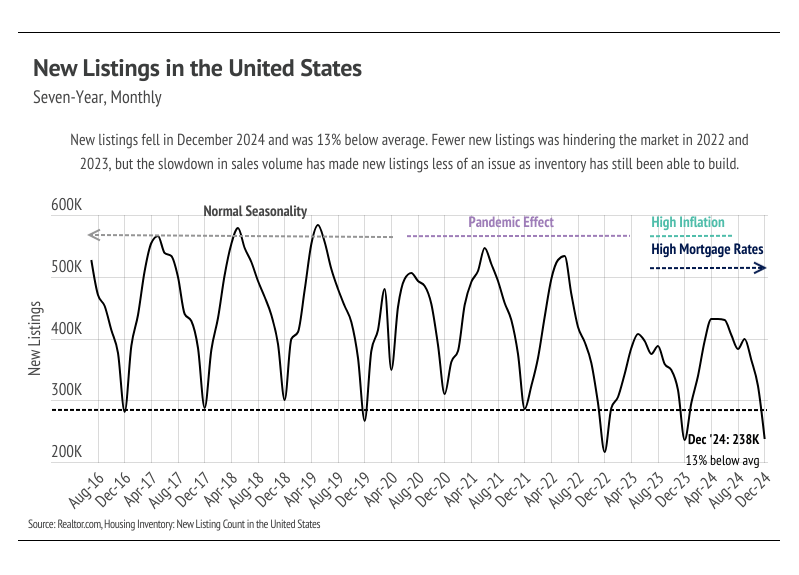

Despite high mortgage rates, home sales have surged in recent months due to increased inventory and a broader acceptance of elevated rates by buyers and sellers. Higher inventory has created a better overall buying experience with less competition, and many have concluded that waiting for lower rates is no longer worth it. Economic optimism surrounding the new administration has further boosted sales, highlighting the emotional aspects of homebuying. Local market trends may differ, and continued updates will provide tailored guidance for your buying or selling decisions.

BIG STORY DATA

THE LOCAL LOWDOWN

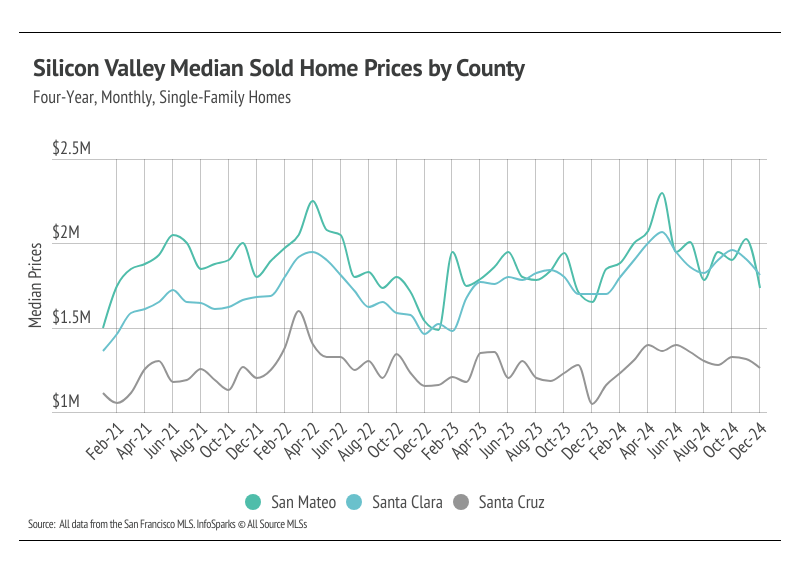

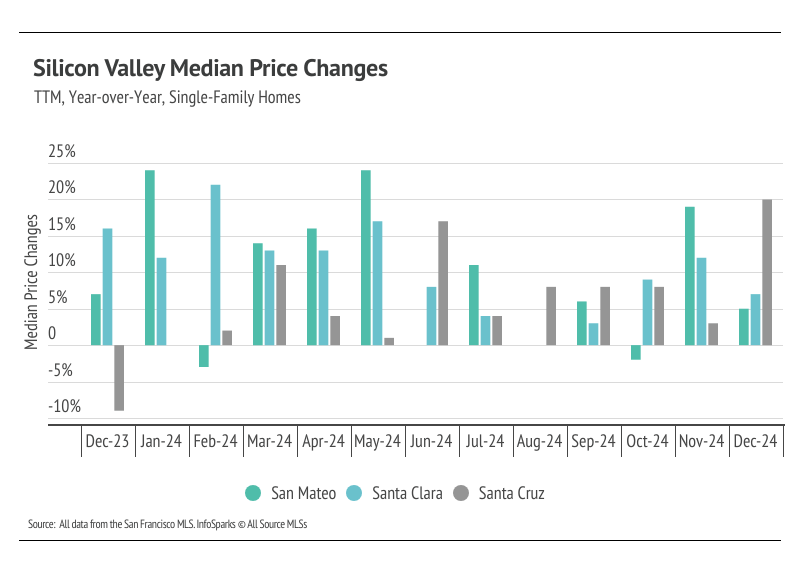

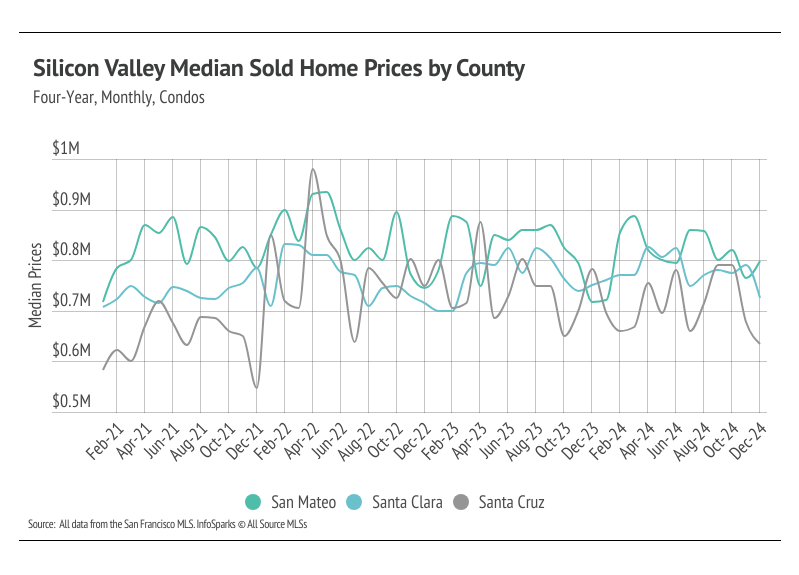

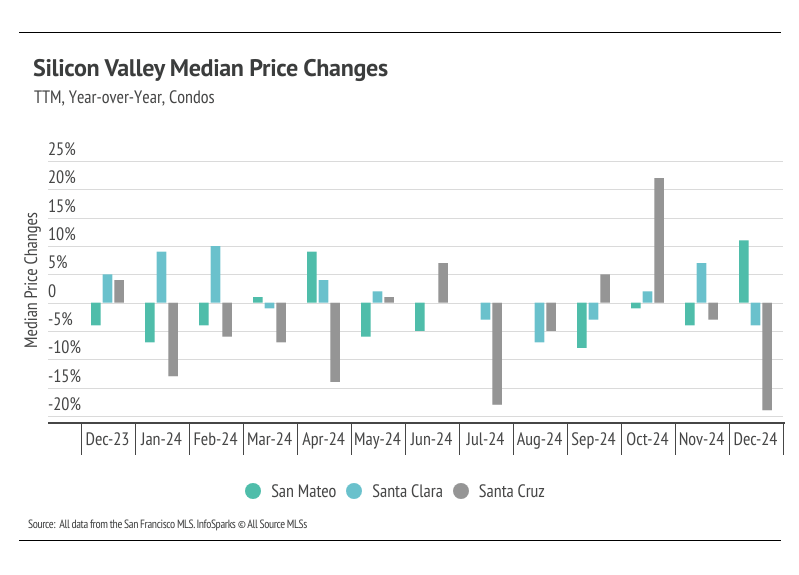

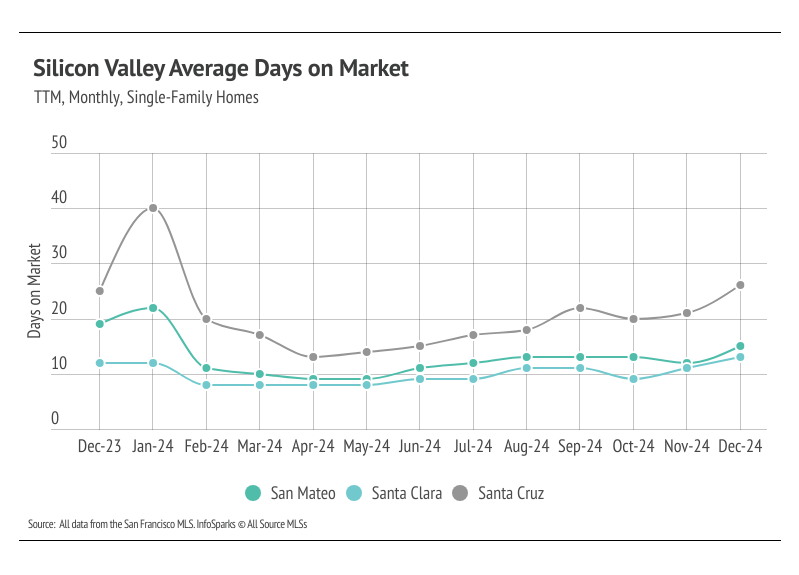

THE MEDIAN SINLE-FAMILY HOME PRICES ARE UP YEAR OVER YEAR

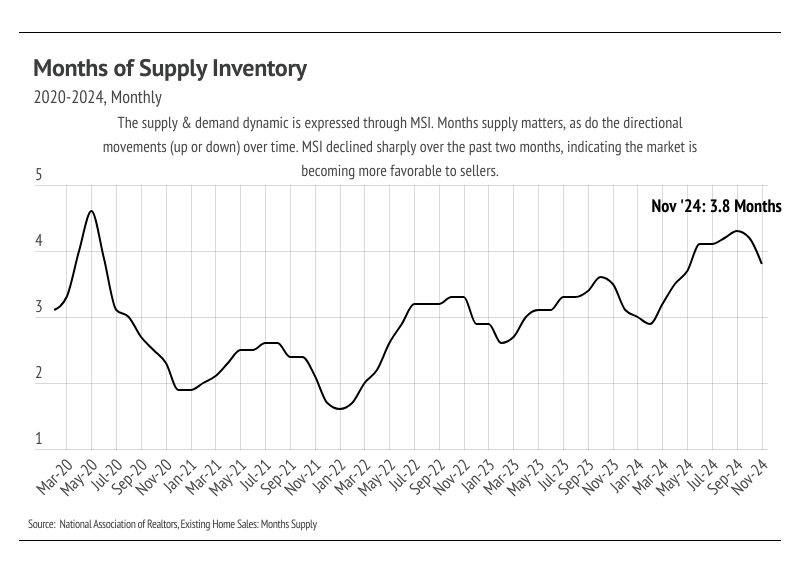

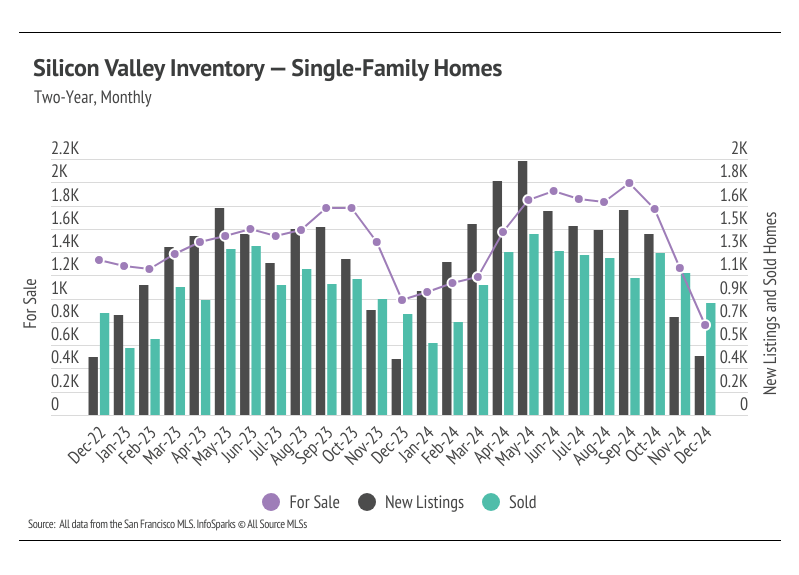

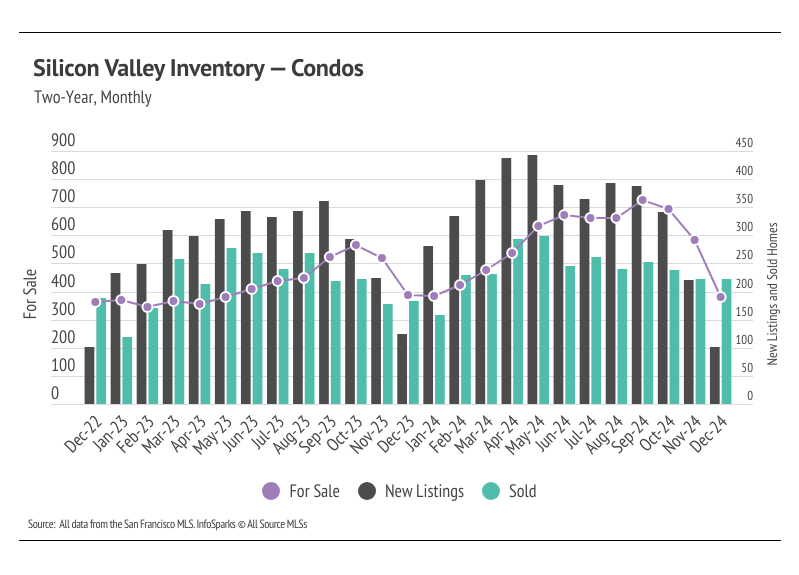

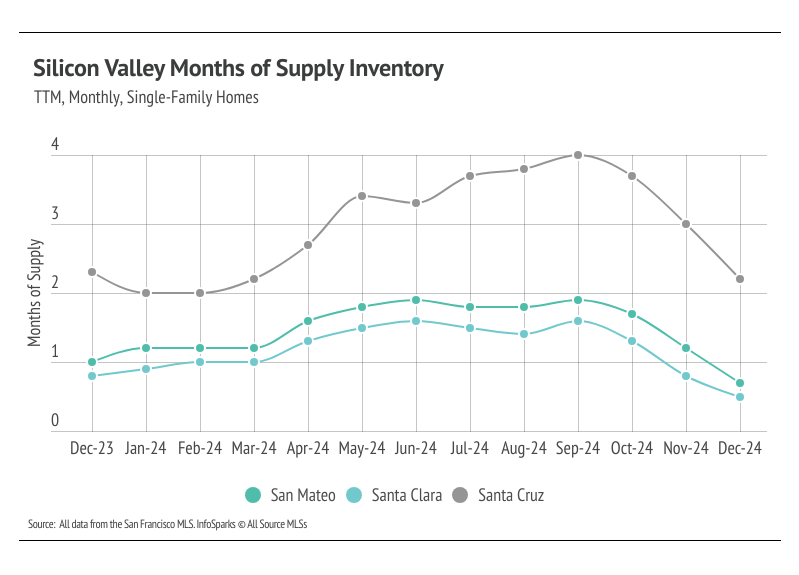

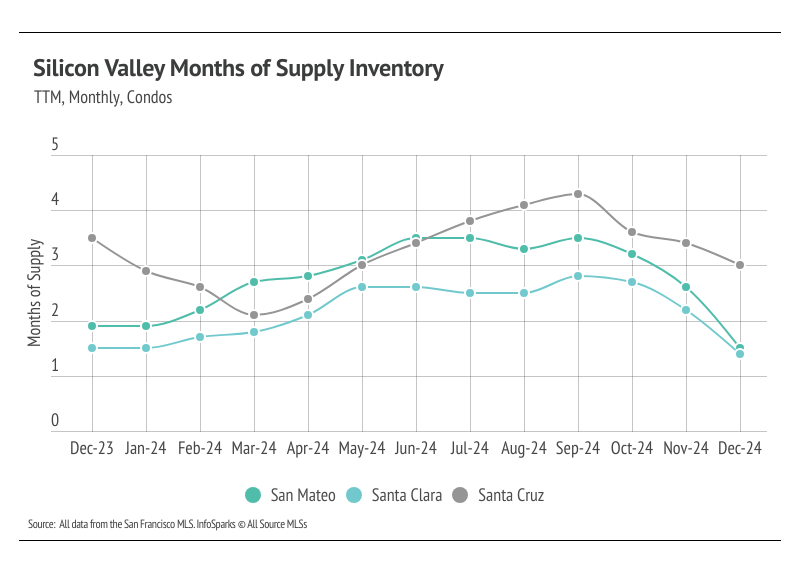

MONTHS OF SUPPLY INVENTORY INDICATED A SELLER'S MARLET IN DECEMBER

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The Silicon Valley market tends to favor sellers, which is reflected in its low MSI. In 2024, Silicon Valley MSI moved higher, particularly in Q2. In Q4, MSI dropped across markets. MSI indicated a sellers’ market for single-family homes and condos with the exception of the Santa Cruz condo market, which is more balanced.

LOCAL LOWDOWN DATA

Stay up to date on the latest real estate trends.

April 28, 2026

April 23, 2026

April 21, 2026

April 20, 2026

April 16, 2026

April 2, 2026

March 25, 2026

March 24, 2026

March 24, 2026

You’ve got questions and we can’t wait to answer them.