October '23 Silicon Valley Real Estate Market Update

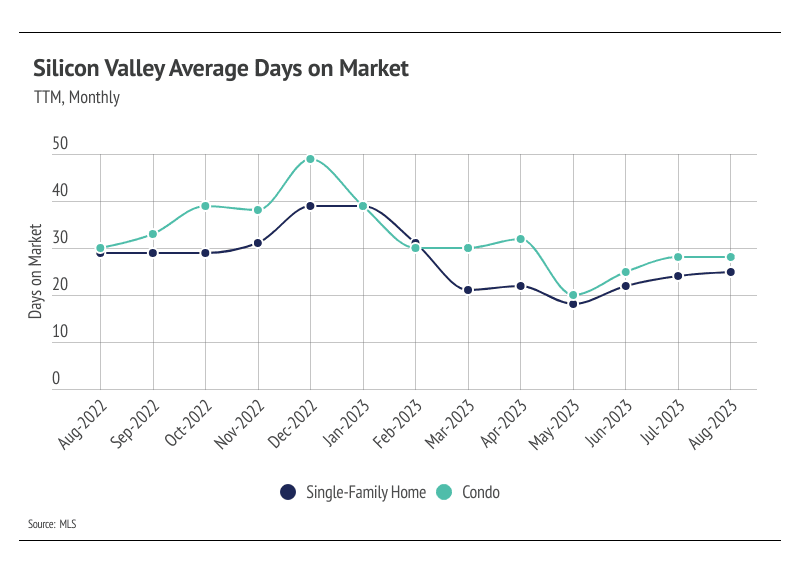

Market Update

Market Update

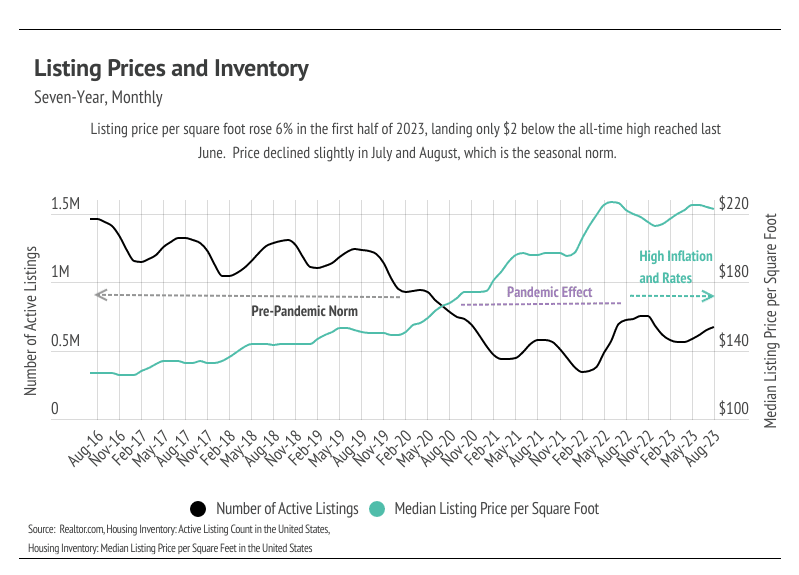

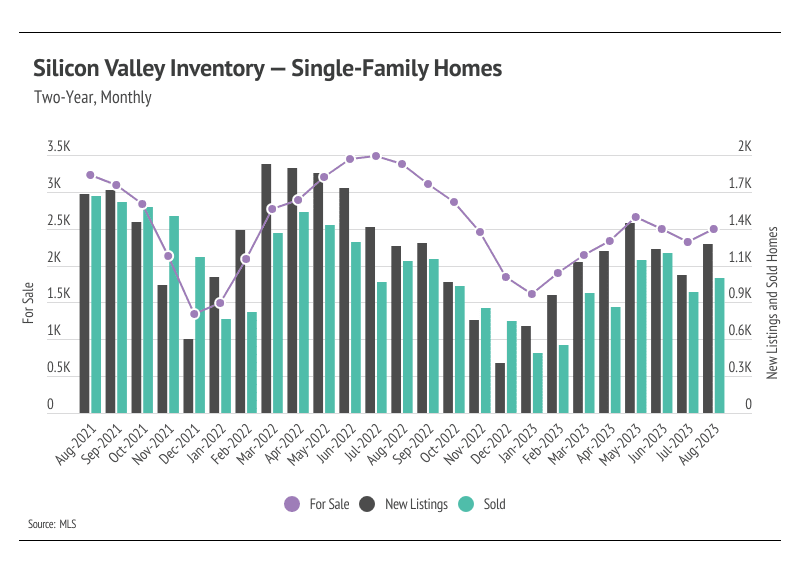

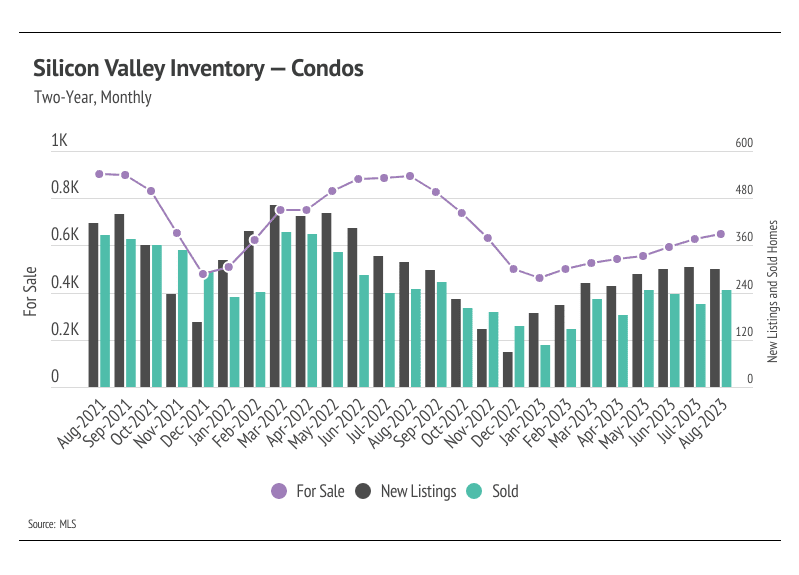

Inventory Growth: An increase in inventory means there are more homes available for buyers to choose from. This can lead to a more balanced market and alleviate some of the competition among buyers.

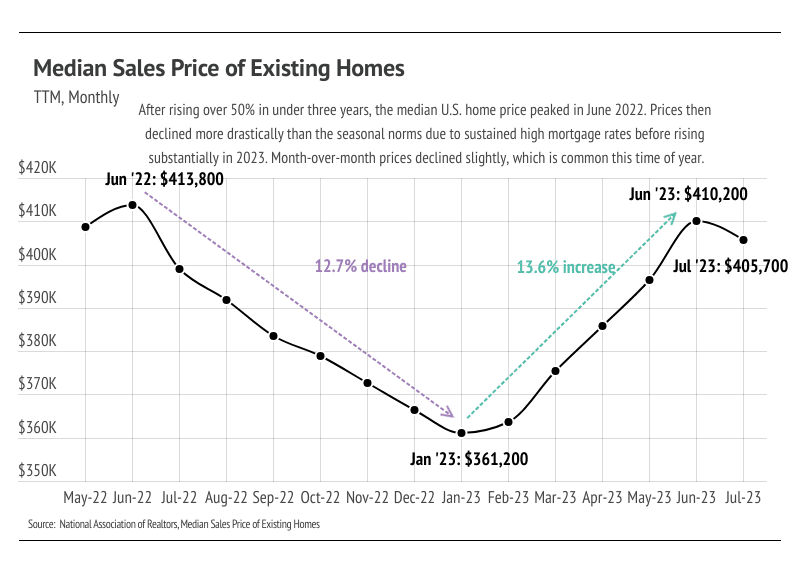

Sales Increase: Rising sales indicate continued activity in the market. It suggests that there is demand from buyers, which is essential for a healthy real estate market.

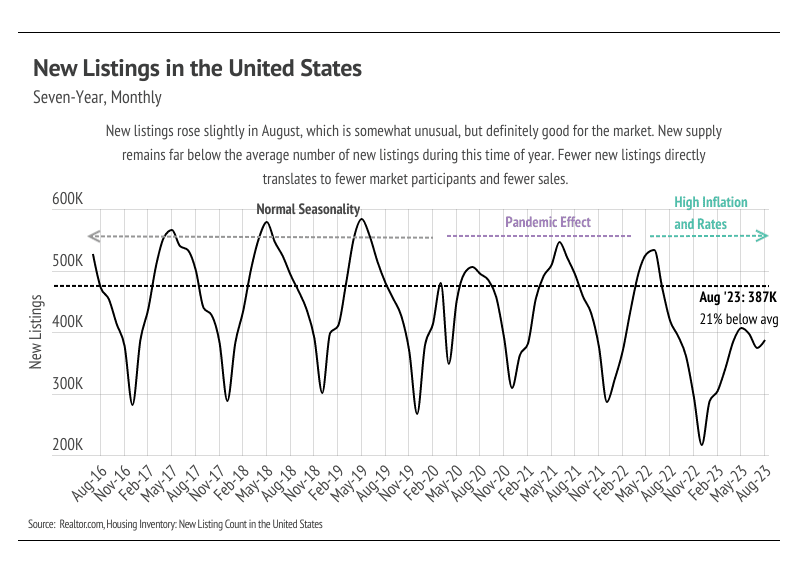

New Listings: More new listings mean that sellers are putting their homes on the market. This can contribute to a more dynamic market with a variety of housing options.

Stay up to date on the latest real estate trends.

July 23, 2026

July 20, 2026

Low Inventory Is Keeping Sellers in Control

July 16, 2026

July 15, 2026

July 15, 2026

July 9, 2026

July 2, 2026

June 27, 2026

June 25, 2026

You’ve got questions and we can’t wait to answer them.