July '25 Market Update

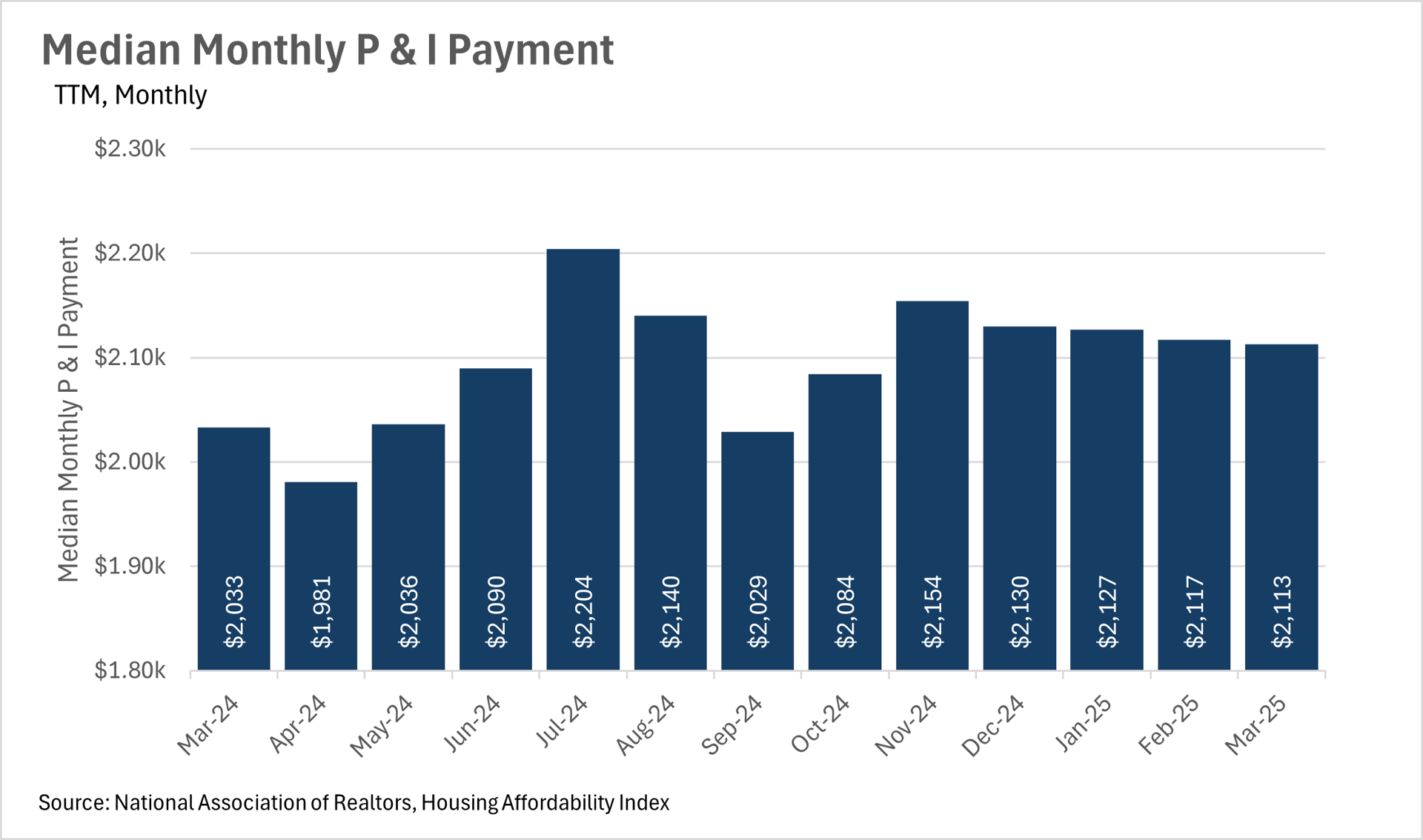

Even as inflation appears to be under control, housing-related costs continue to rise. The median monthly principal and interest (P&I) payment is now $2,113, a 3.94% increase year-over-year—outpacing broader inflation, which remains in the 2–3% range. This indicates that inflationary pressures are still present in the housing sector, driven by both local supply constraints and ongoing buyer demand in many markets.

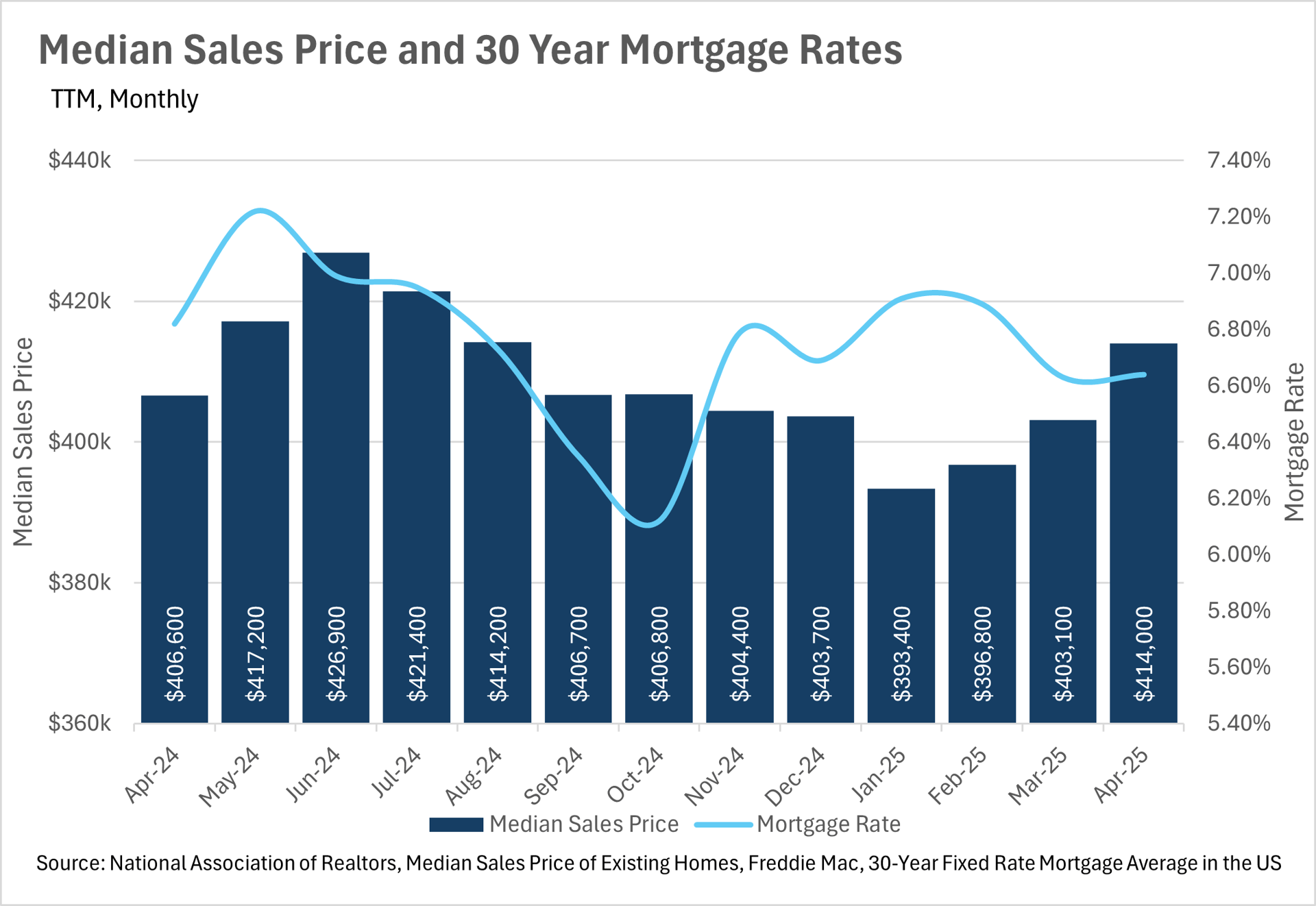

Mortgage rates are holding steady in the mid to high-6% range, with no major drops in sight unless the economy weakens significantly. Despite some speculation, the Federal Reserve has remained cautious. Most Fed officials forecast the federal funds rate to drop slightly, reaching around 3.75–4.00% by year-end, and 3.25–3.50% by 2026.

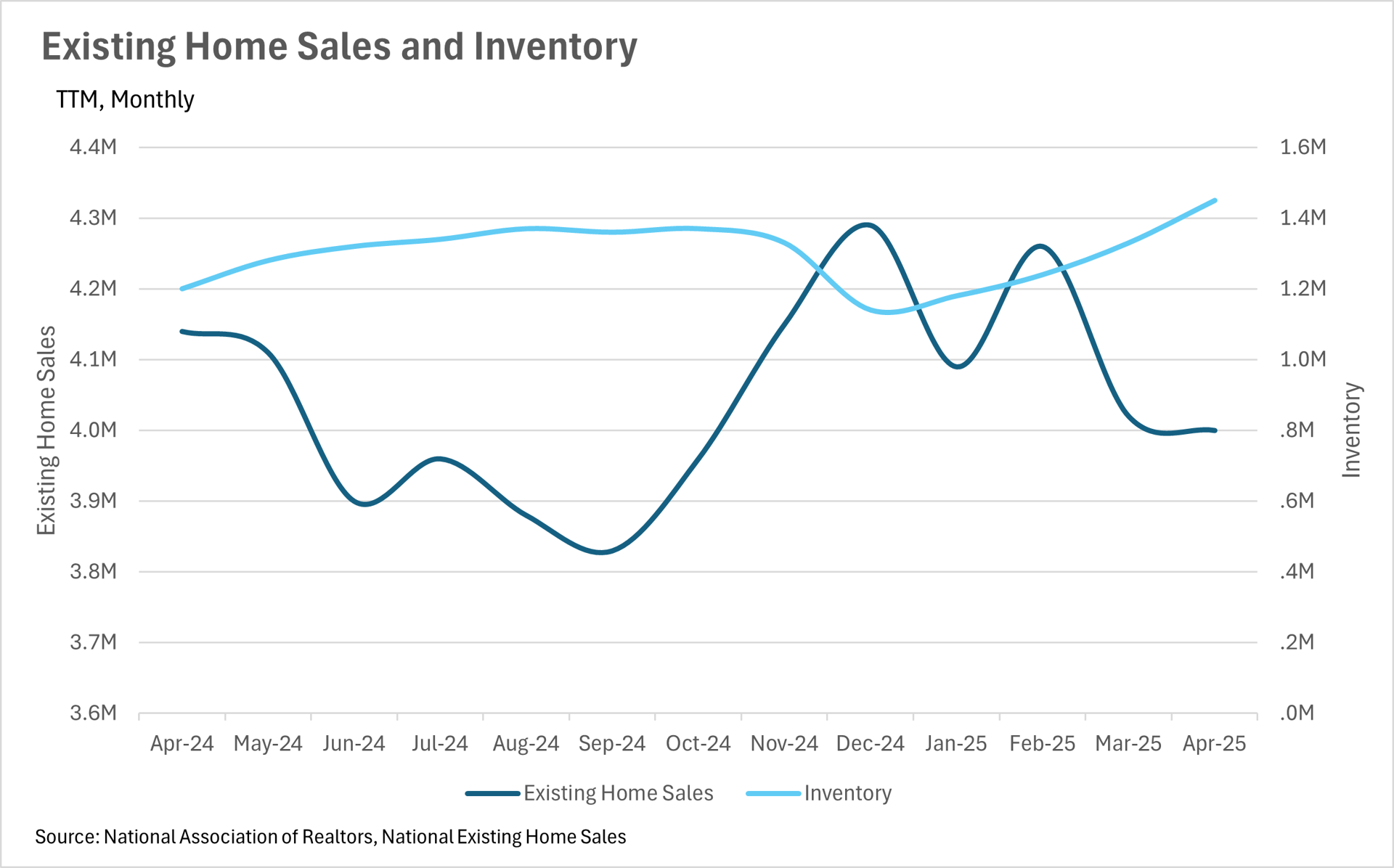

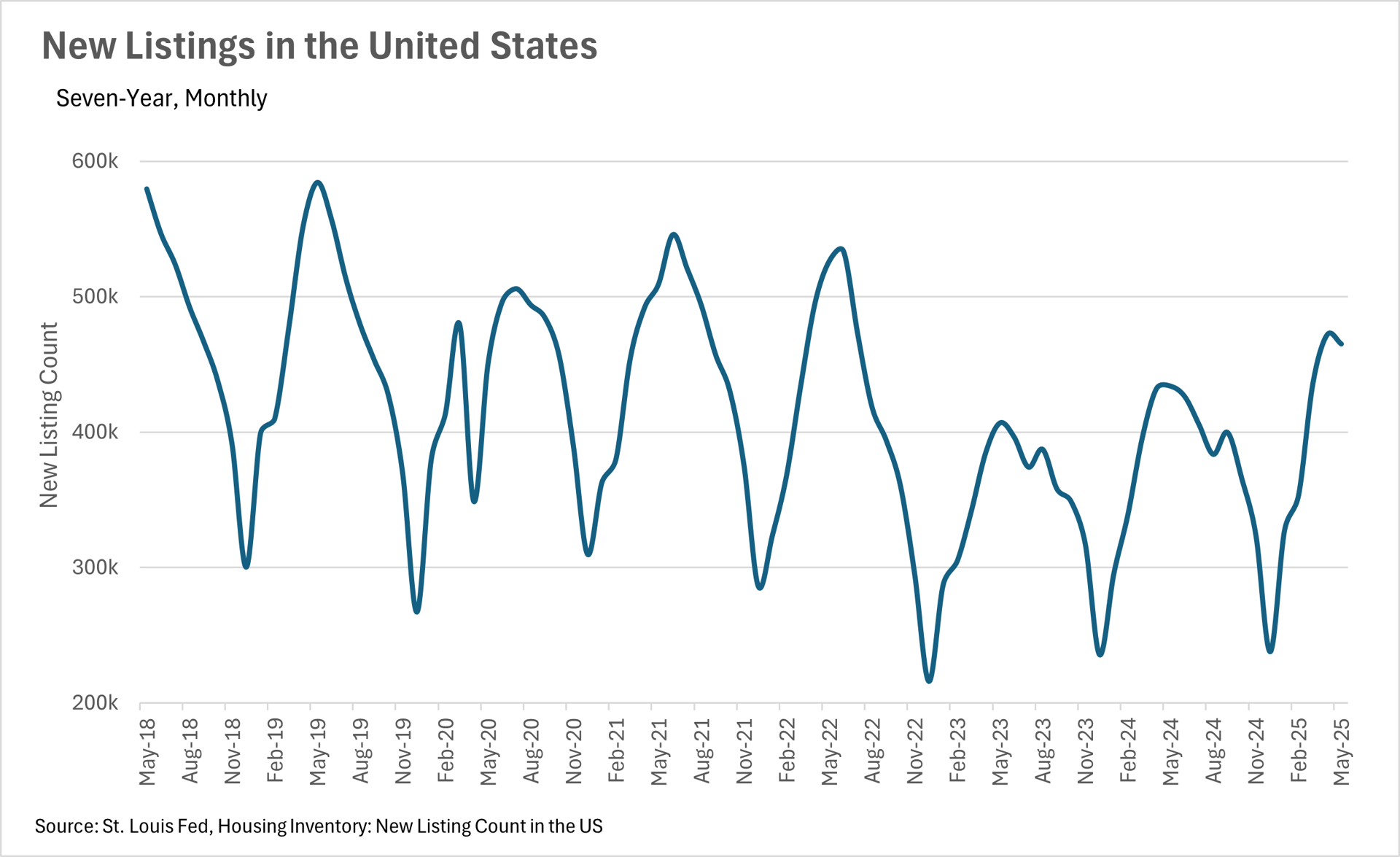

On a national level, housing inventory is growing, with a 20.83% increase year-over-year, now totaling 1.45 million homes. Meanwhile, existing home sales dropped 3.38% to 4 million. Interestingly, home prices are still climbing, with a median sale price of $414,000, up 1.82% year-over-year. And the number of new listings is rising too—up 7.19%compared to last year.

➡️ Bottom Line: We’re seeing shifting conditions on a national scale, but real estate is always local. Be sure to check out our Local Lowdown for insights on what’s happening in your own neighborhood—and how to stay ahead in this evolving market.

BIG STORY DATA

THE LOCAL LOWDOWN

The Bay Area shows a clear split:

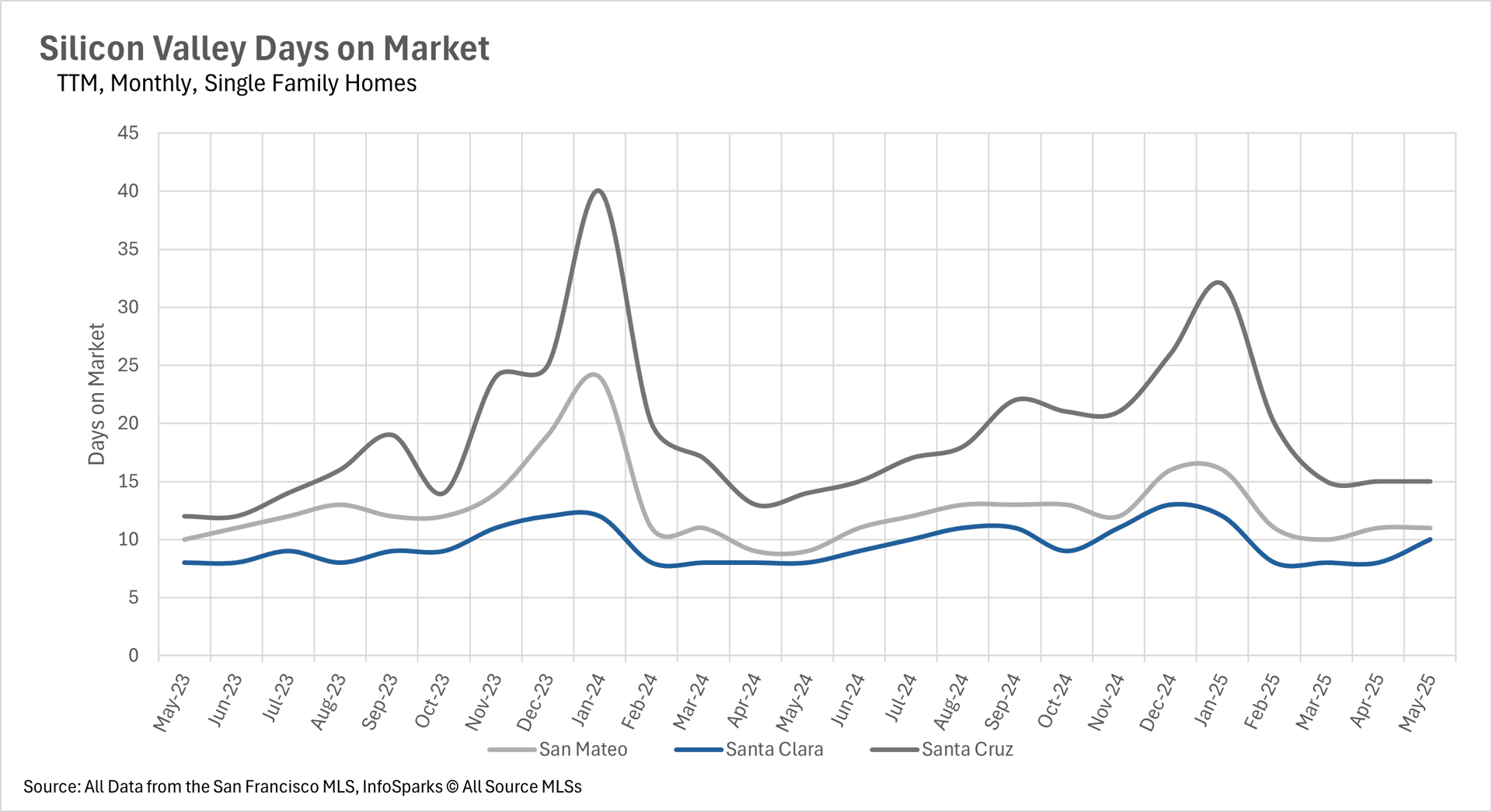

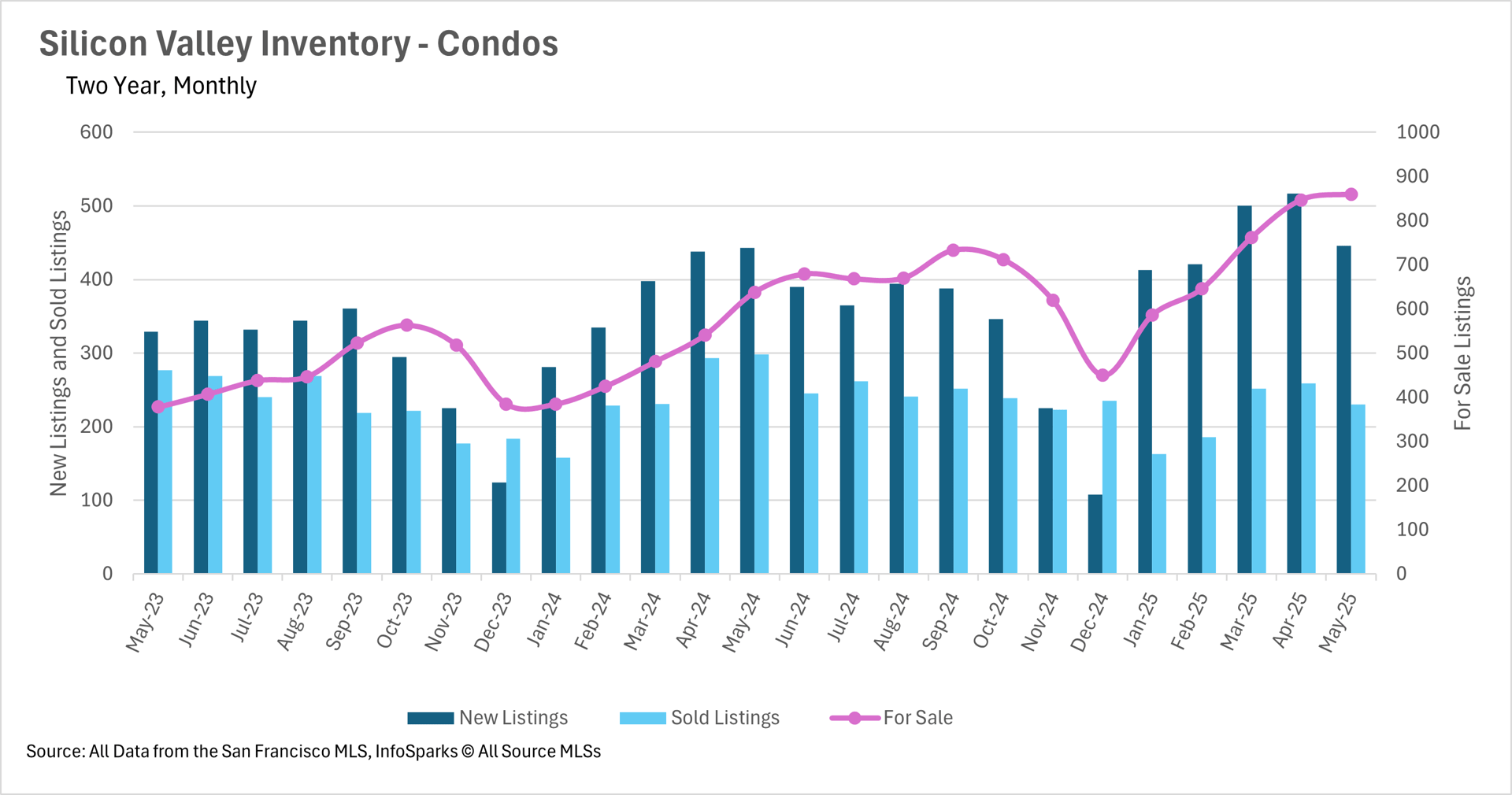

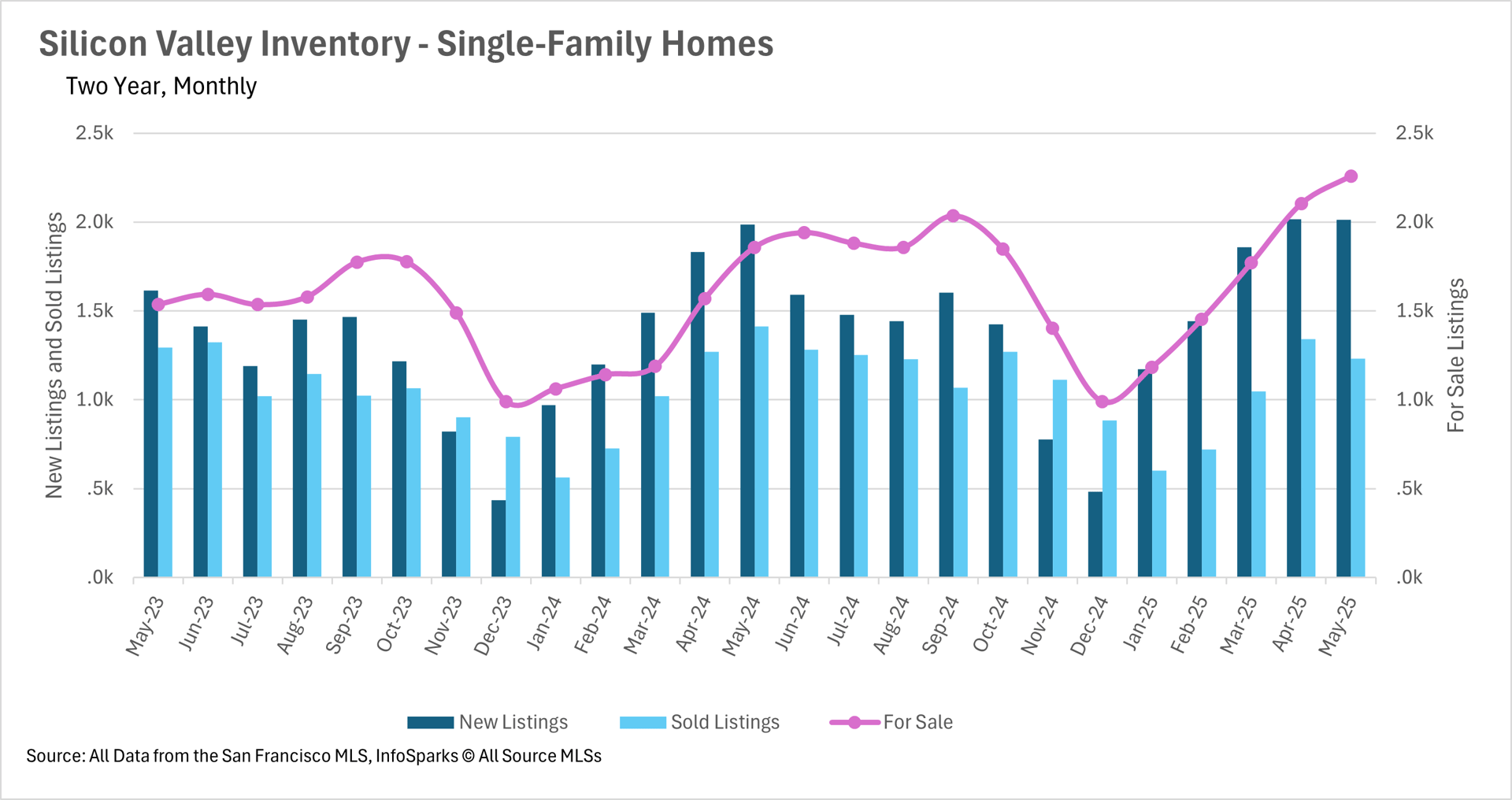

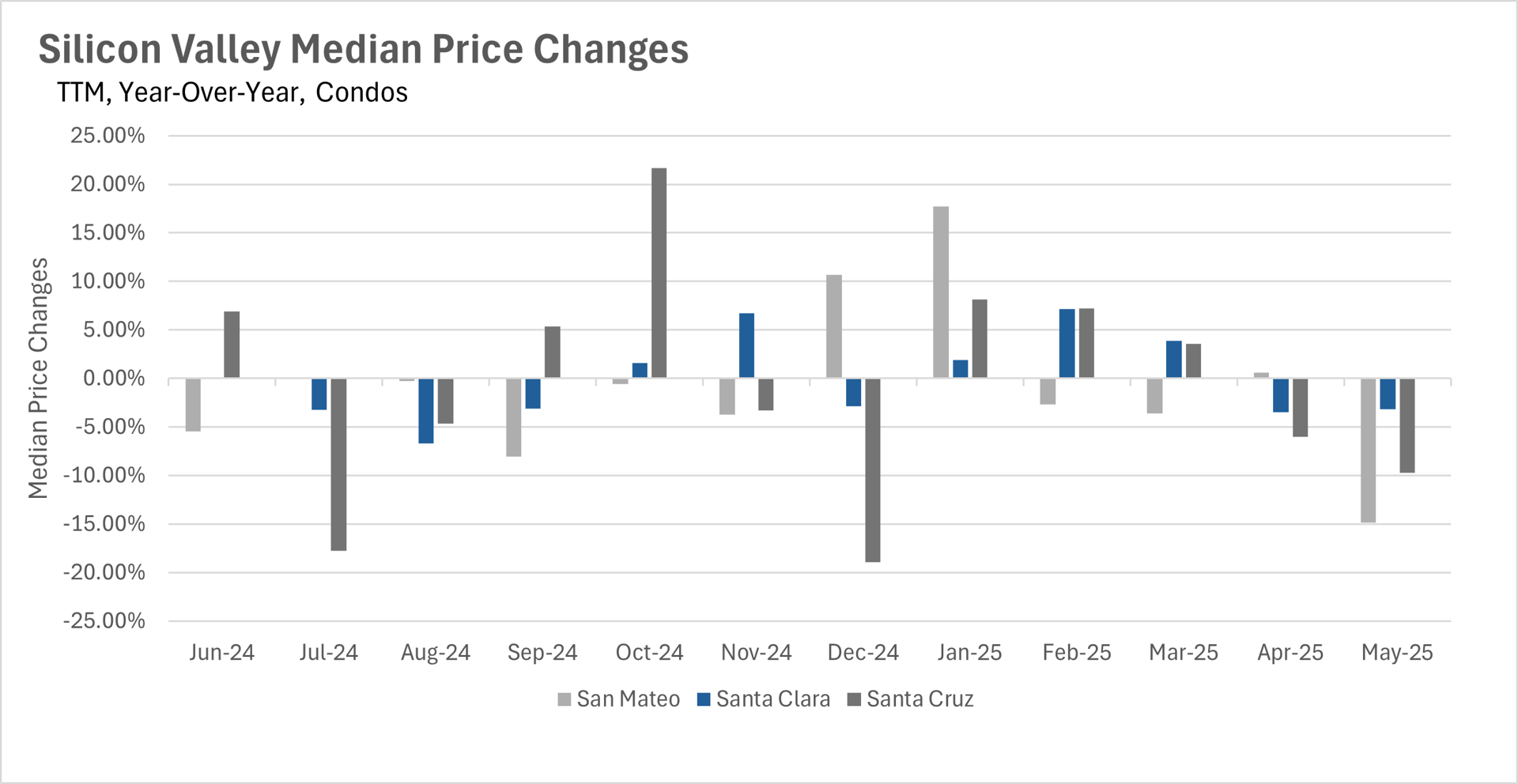

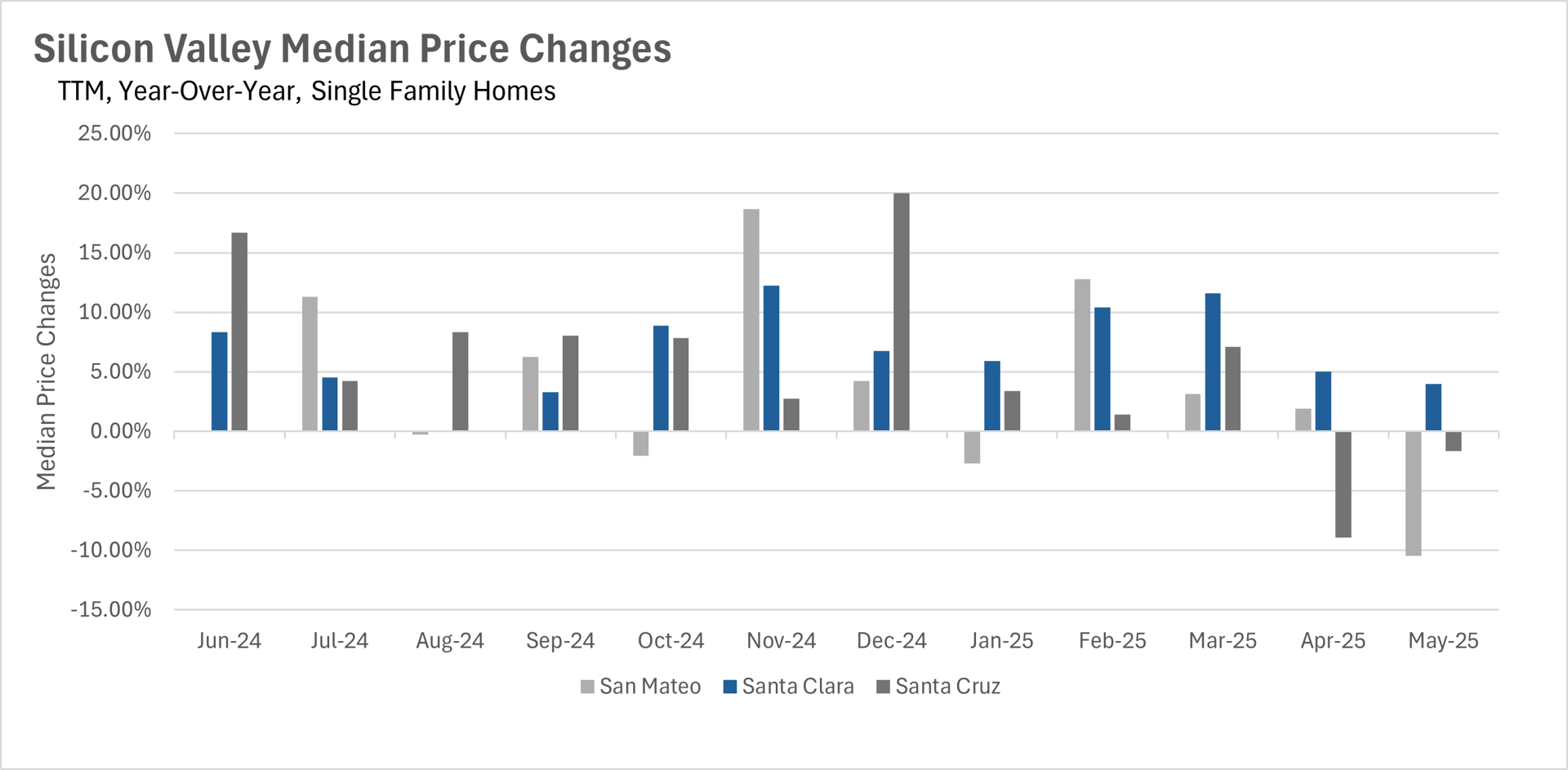

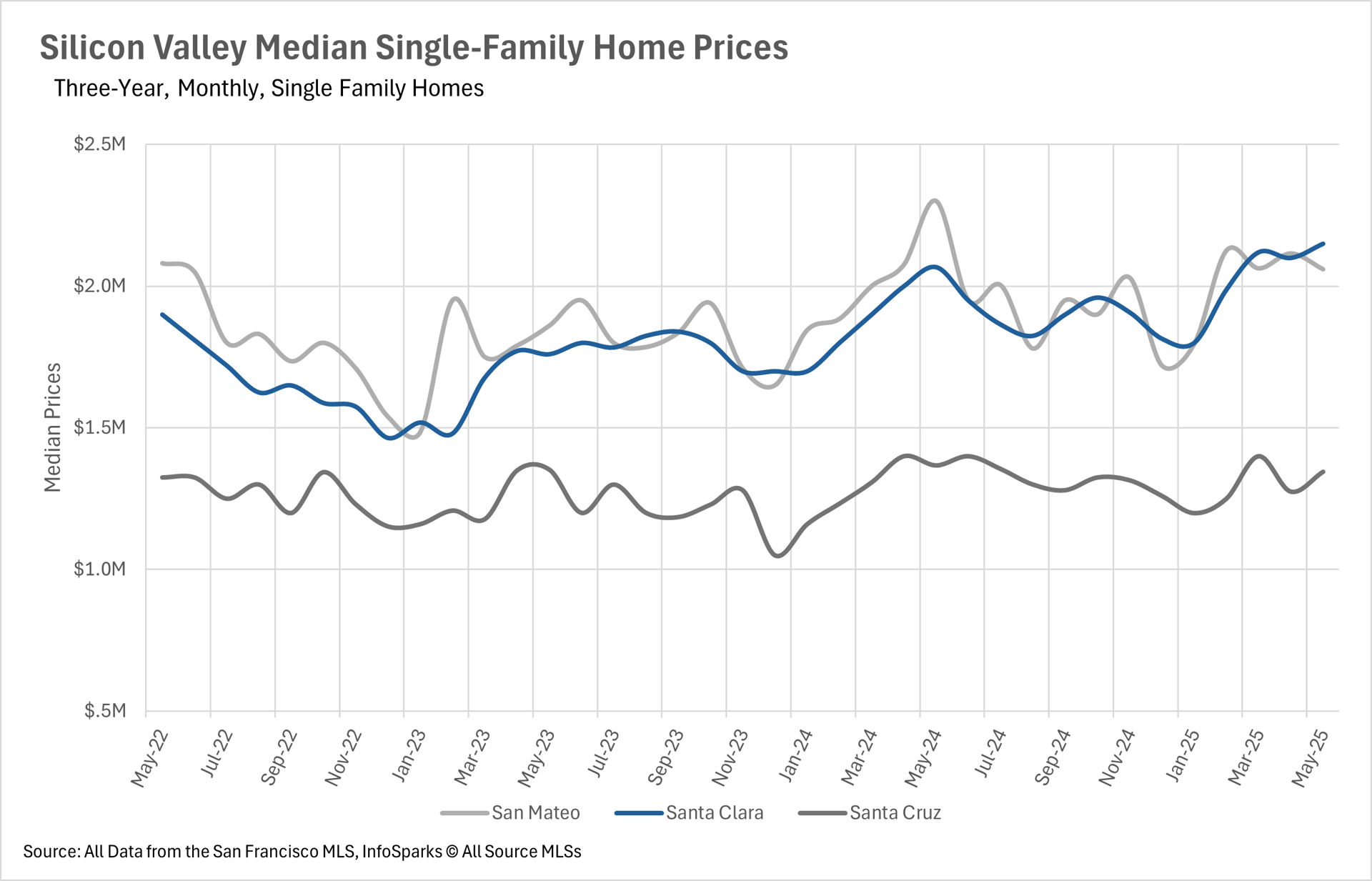

San Francisco led the Bay Area in May with strong price gains—single-family homes up 7.58% and condos up 8.26%, hitting two-year highs. In contrast, Silicon Valley cooled: Santa Cruz and San Mateo saw declines, while Santa Clara posted a modest 3.99% gain. Condos dropped sharply across the region, especially in San Mateo (-14.88%).

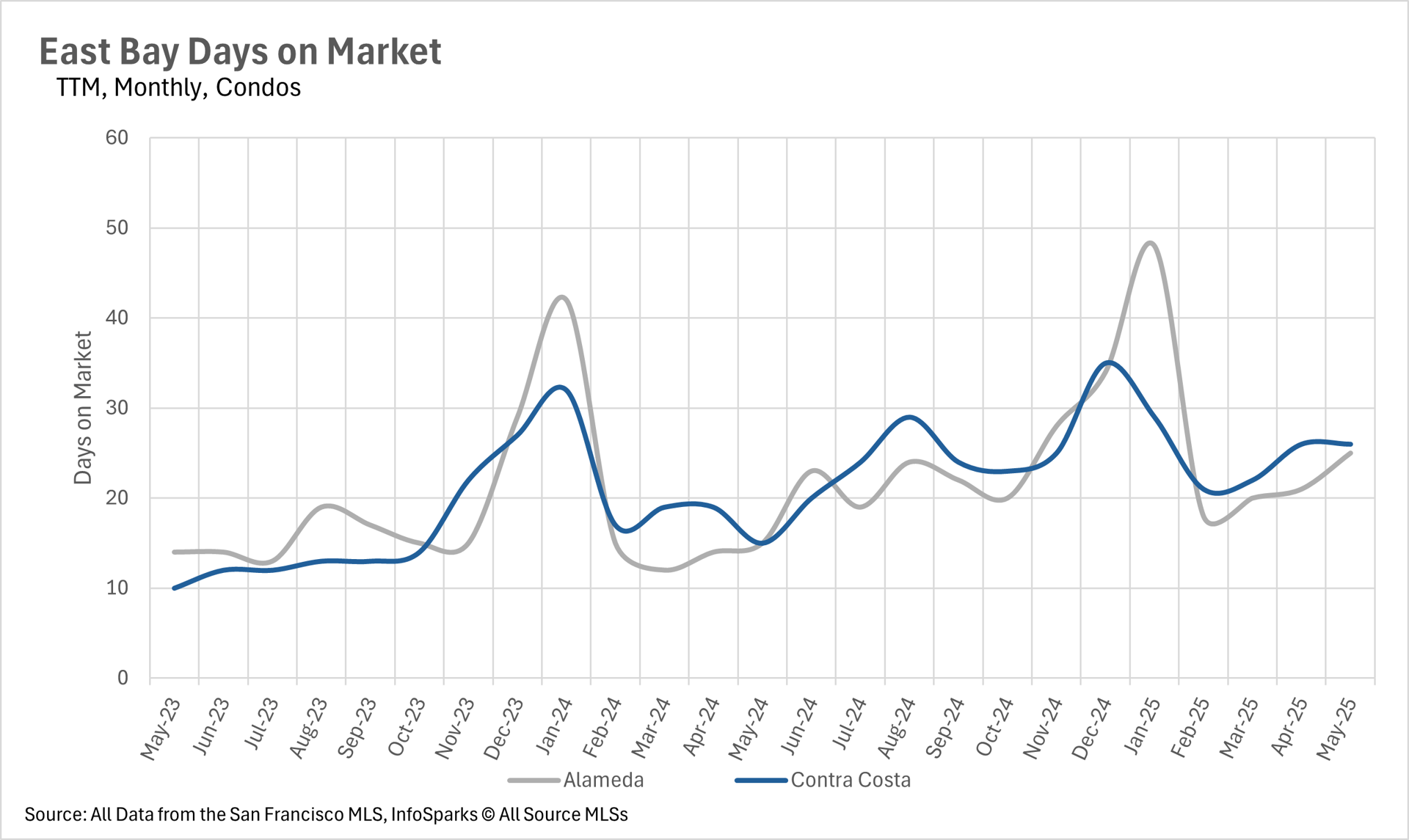

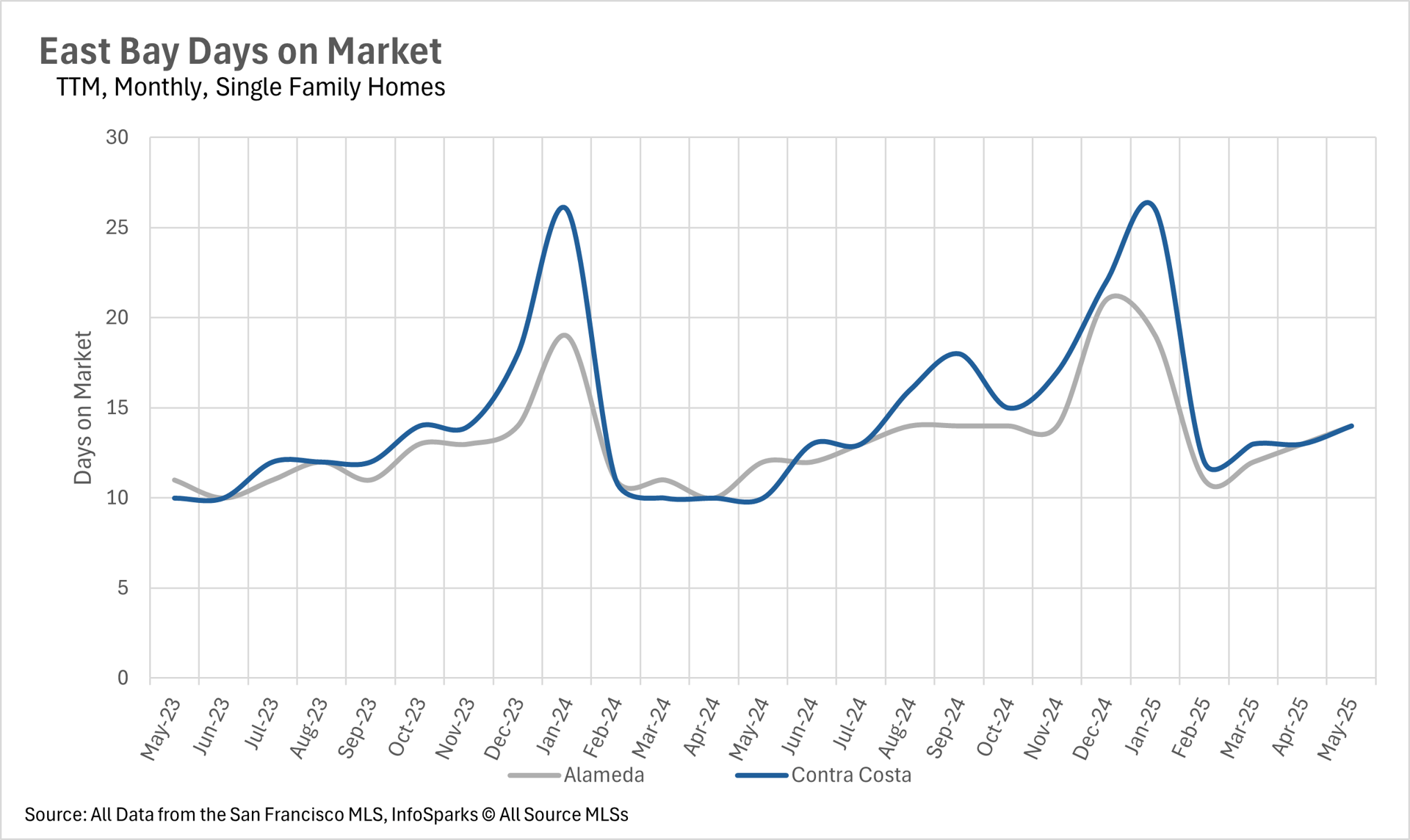

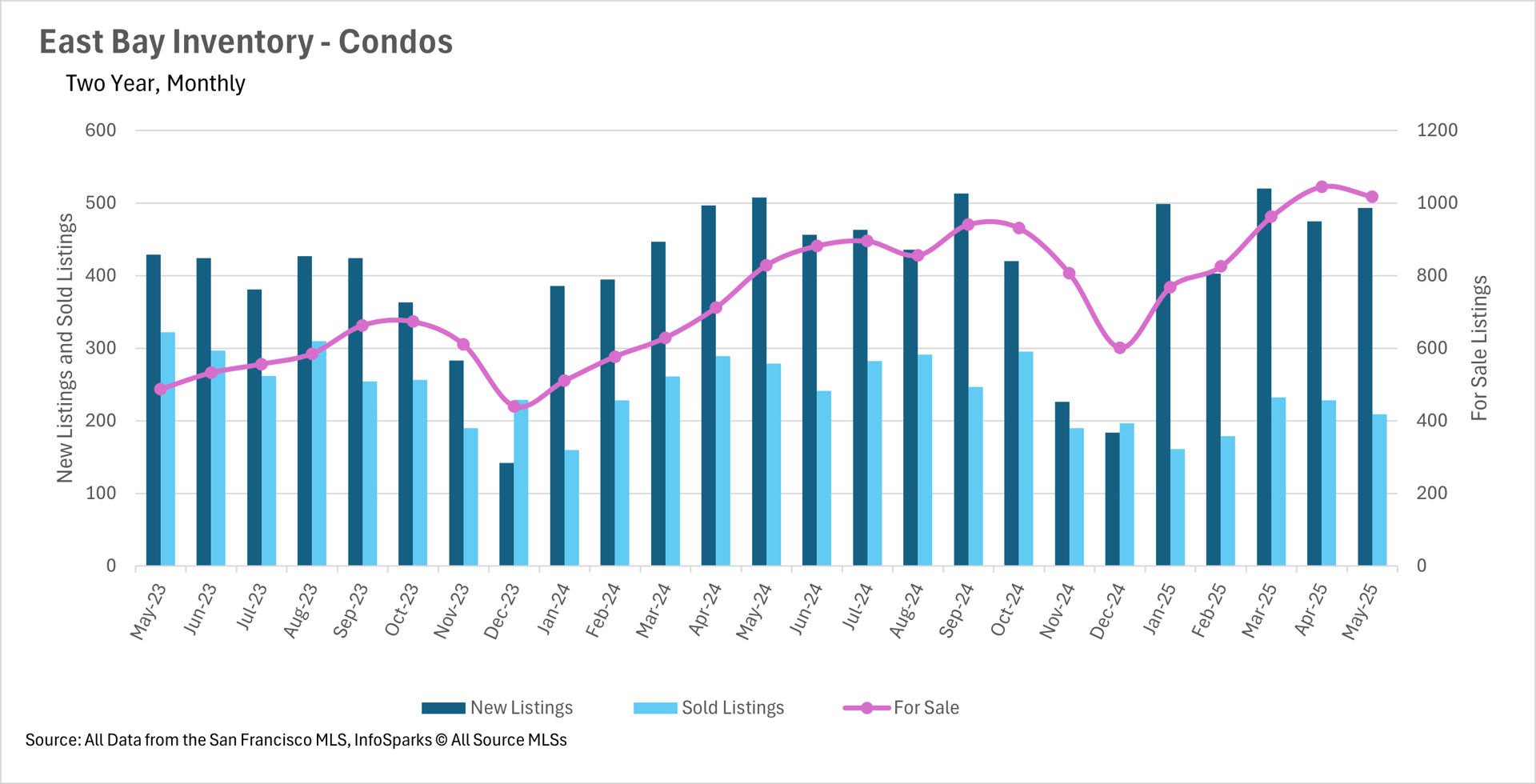

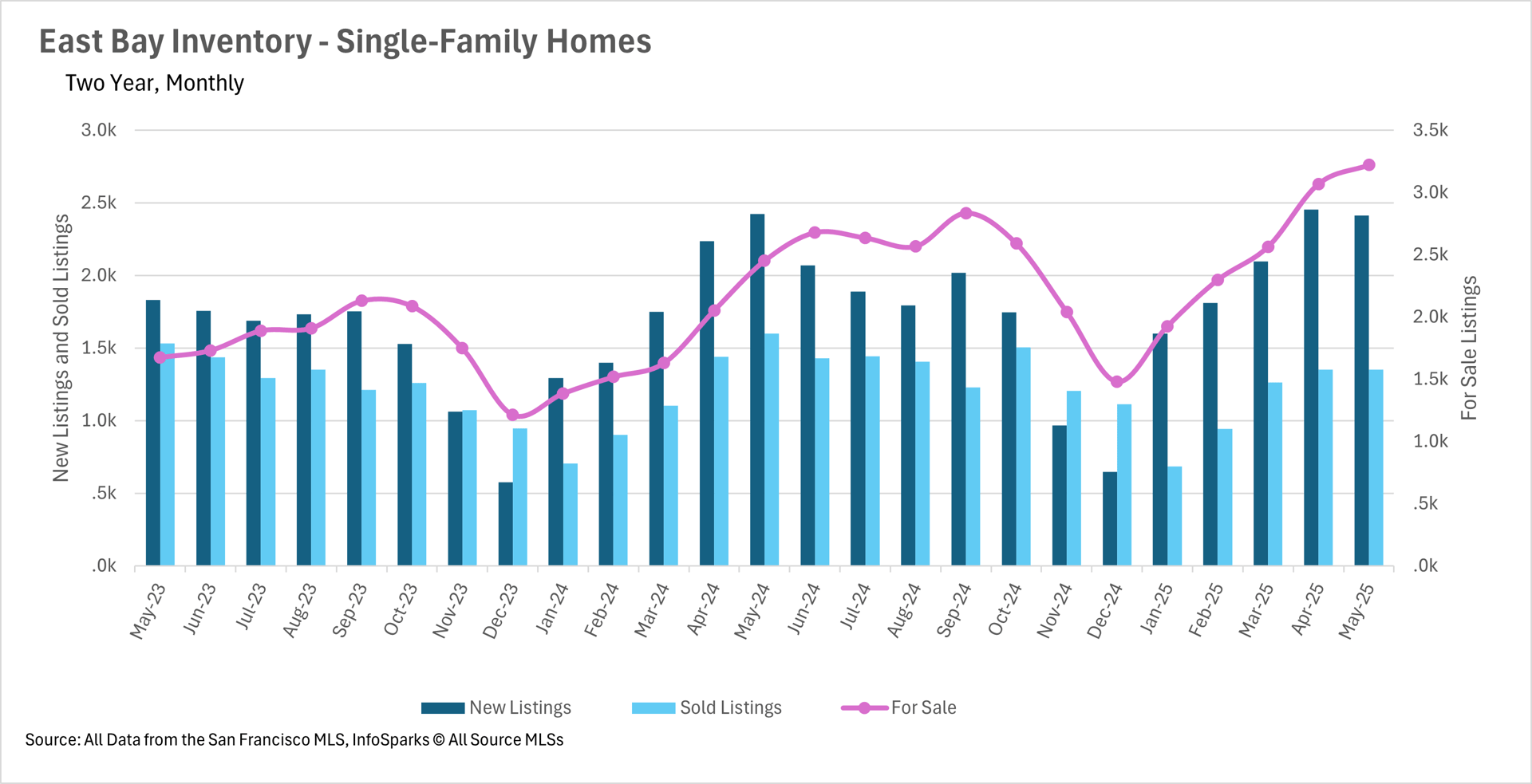

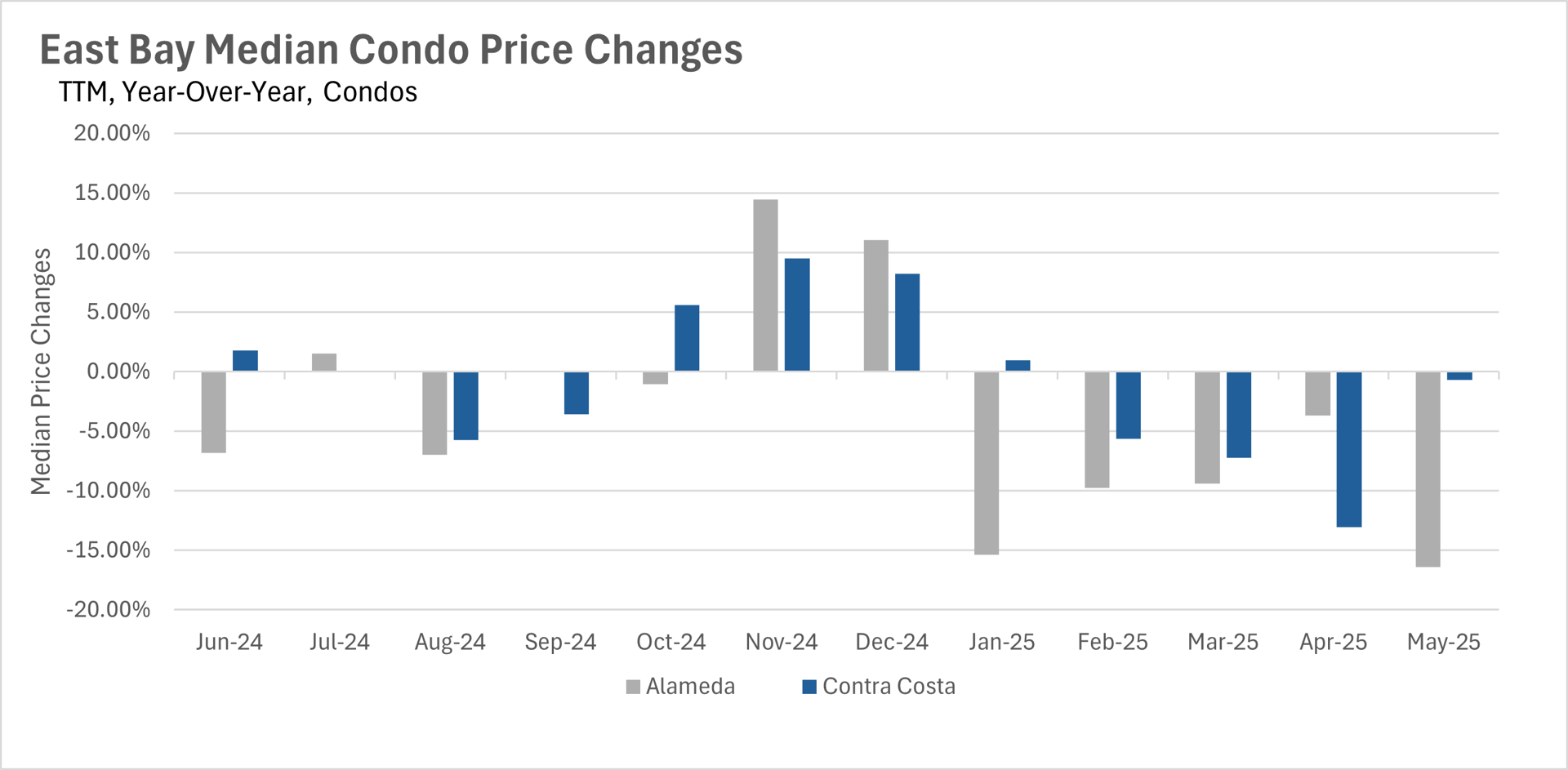

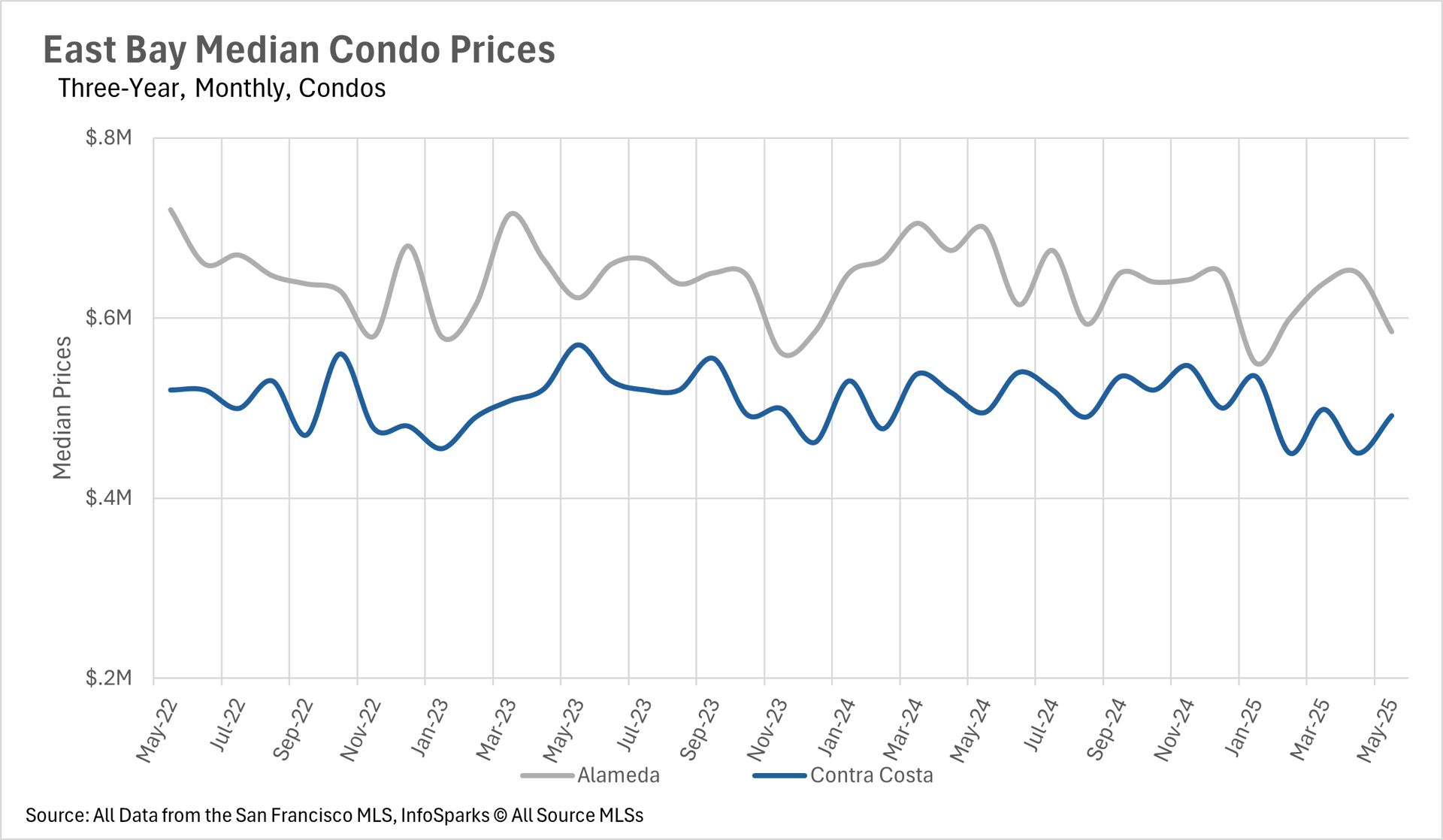

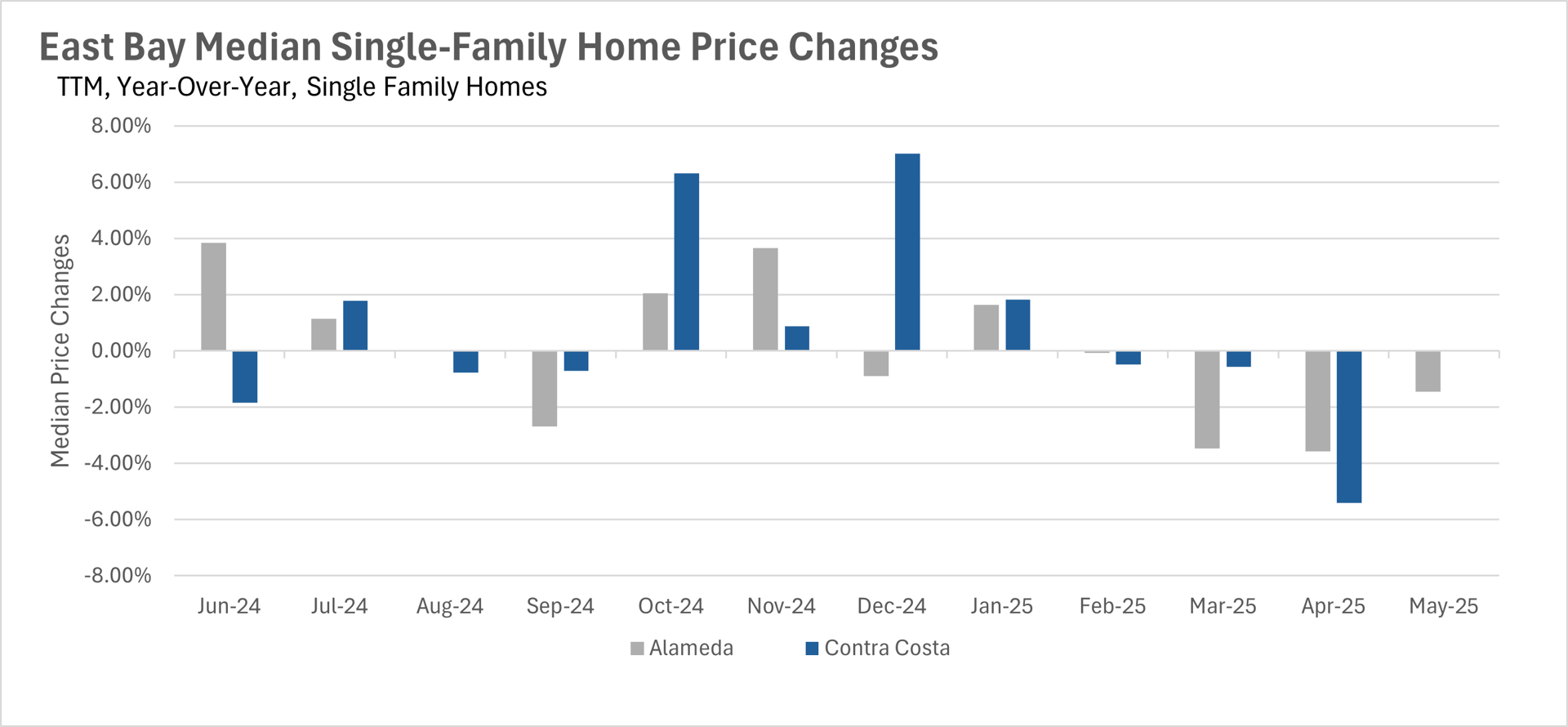

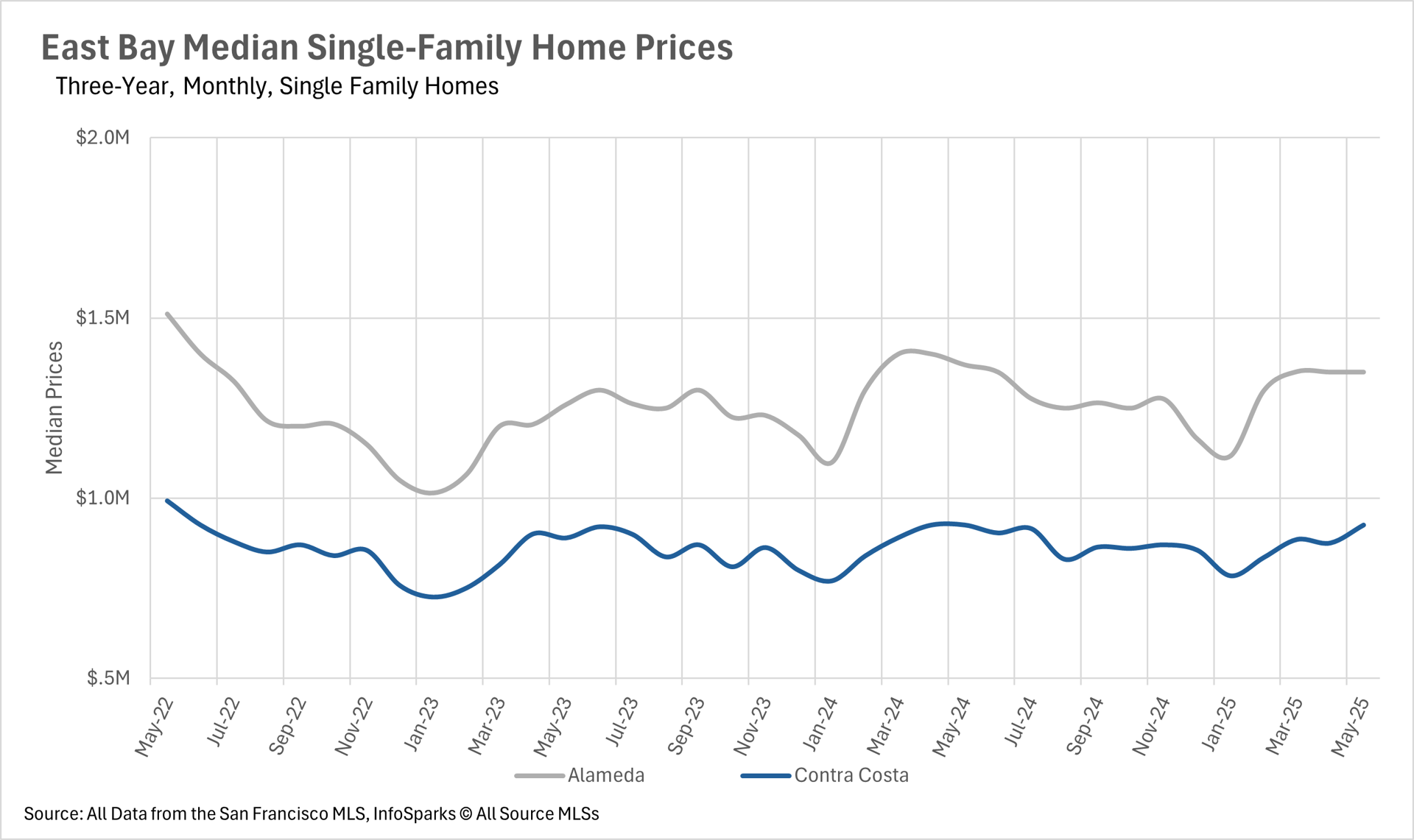

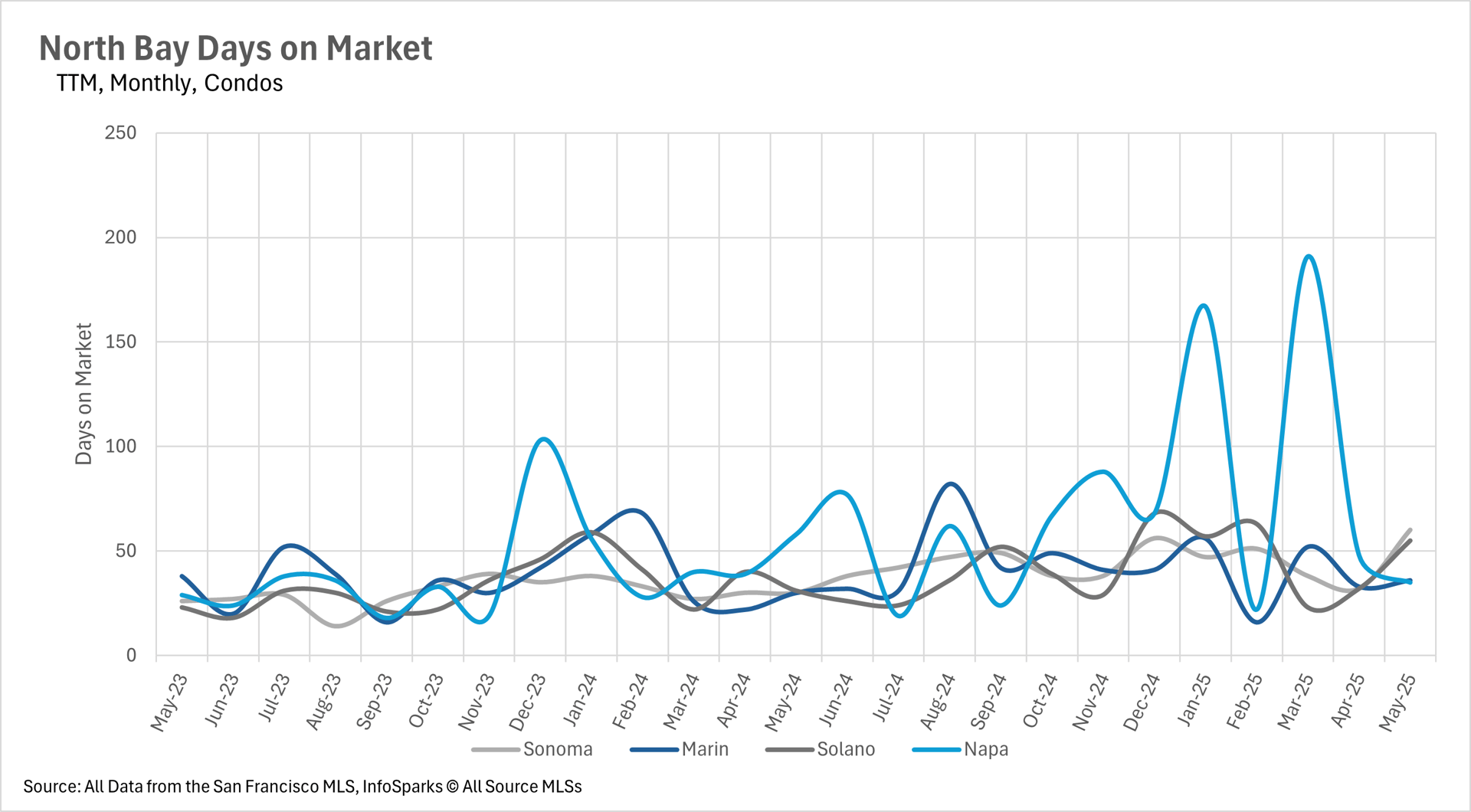

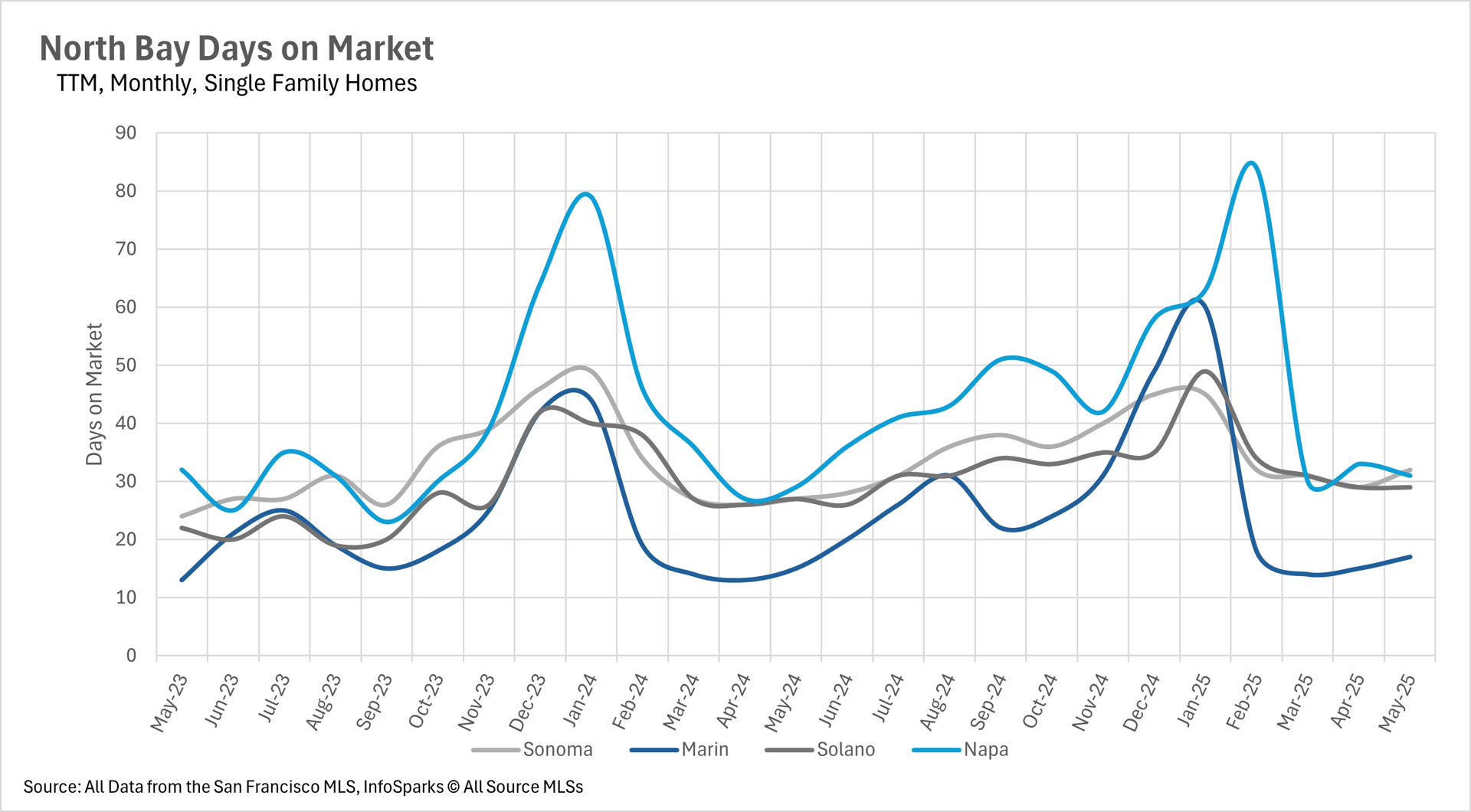

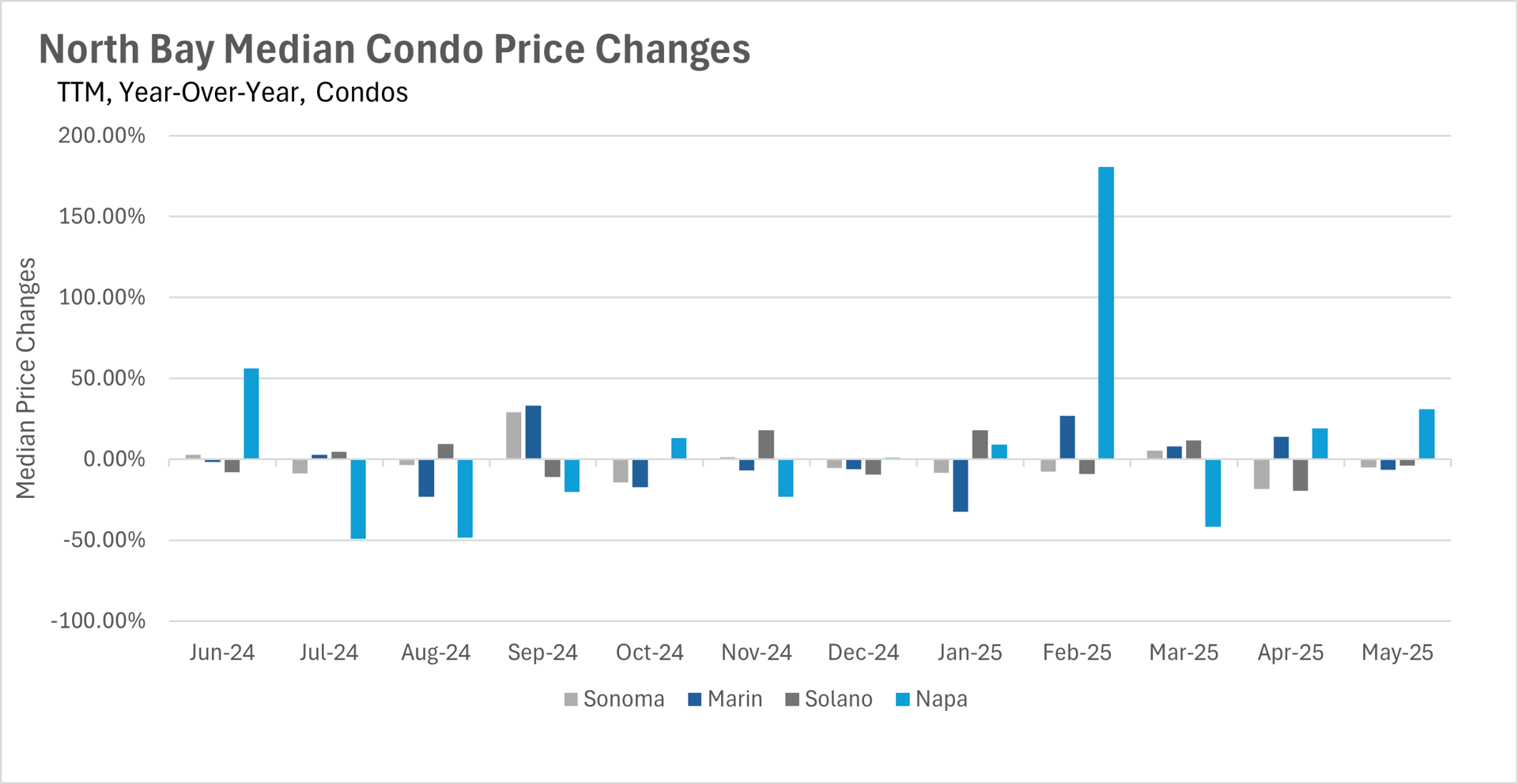

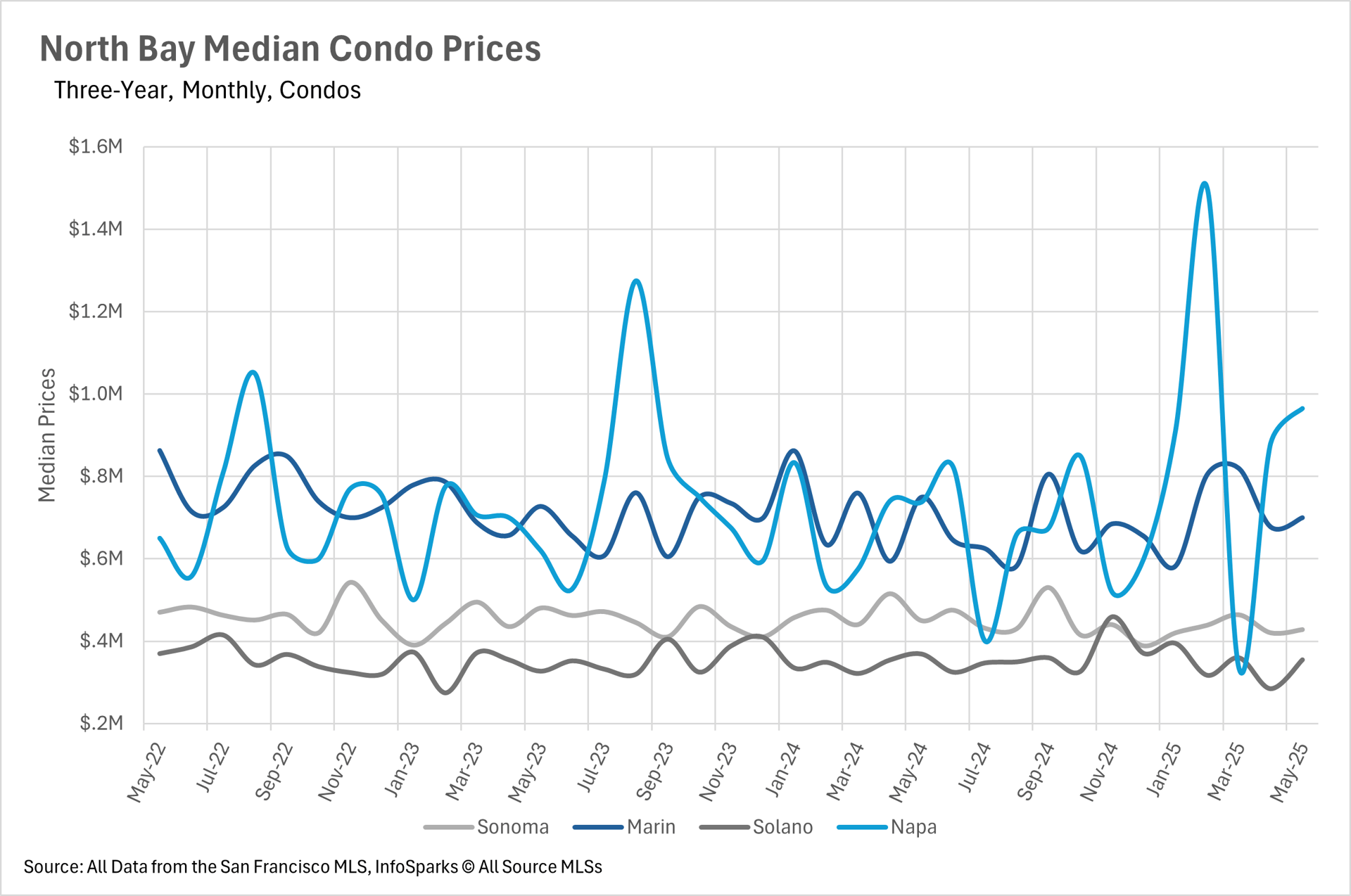

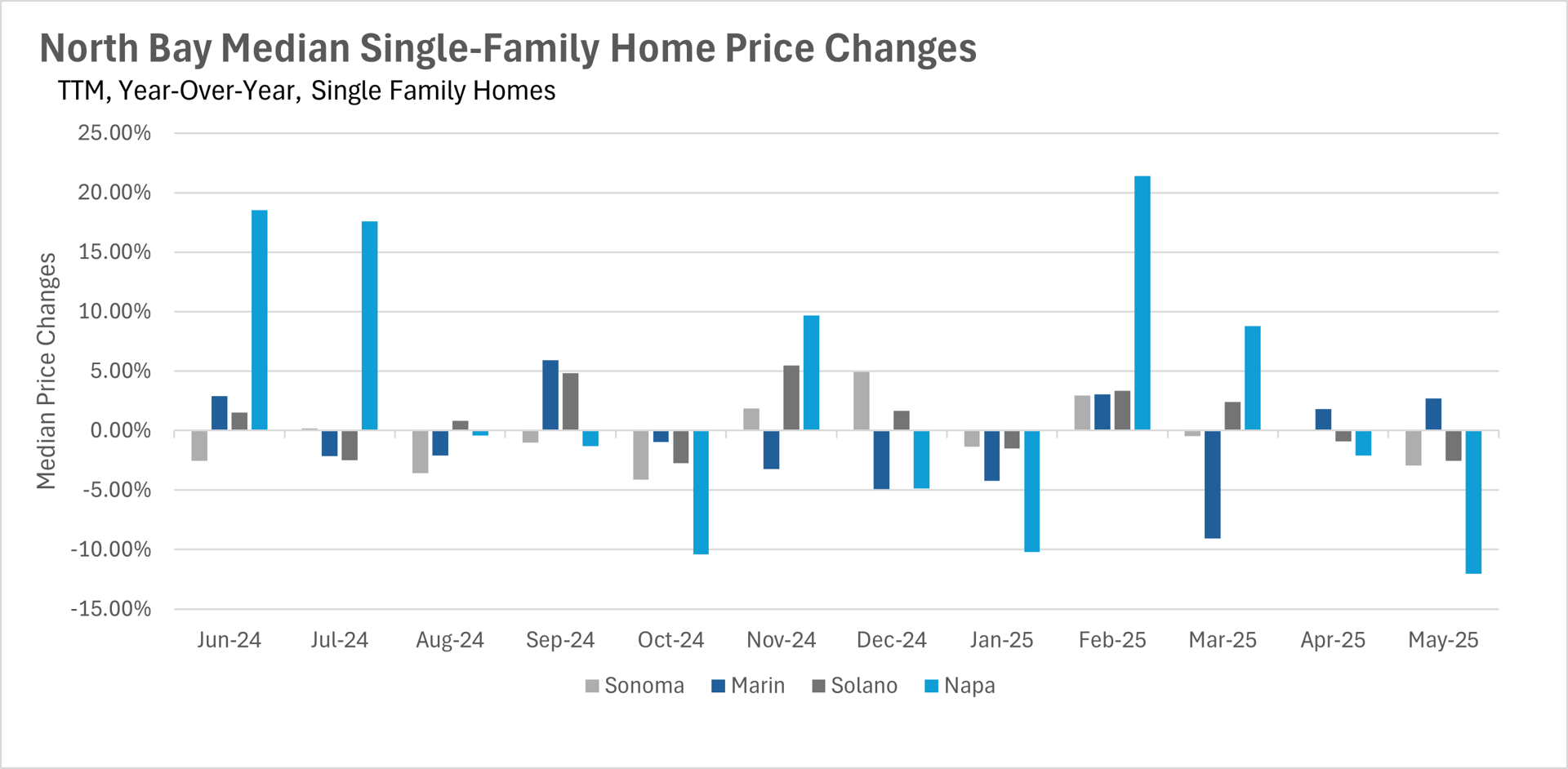

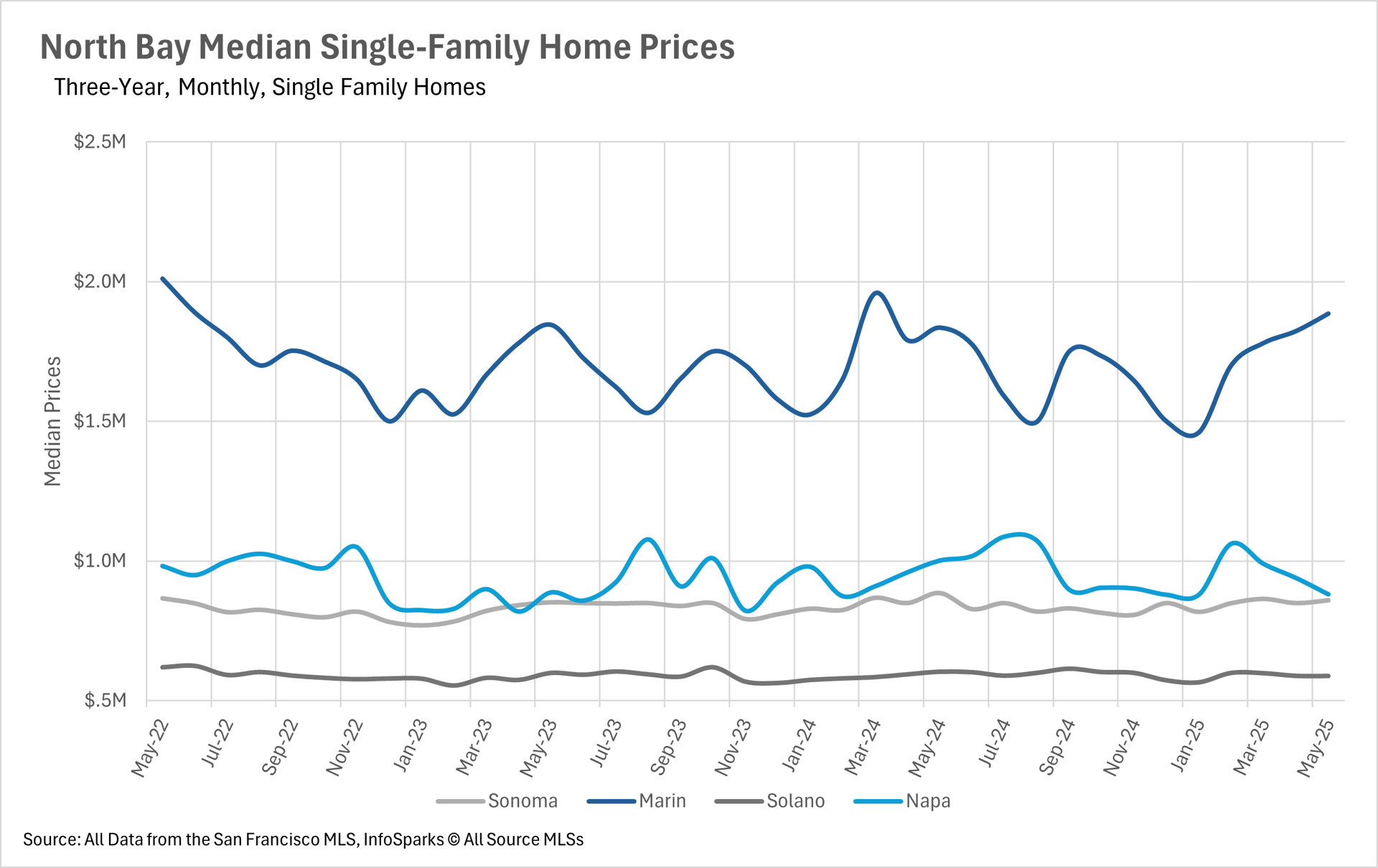

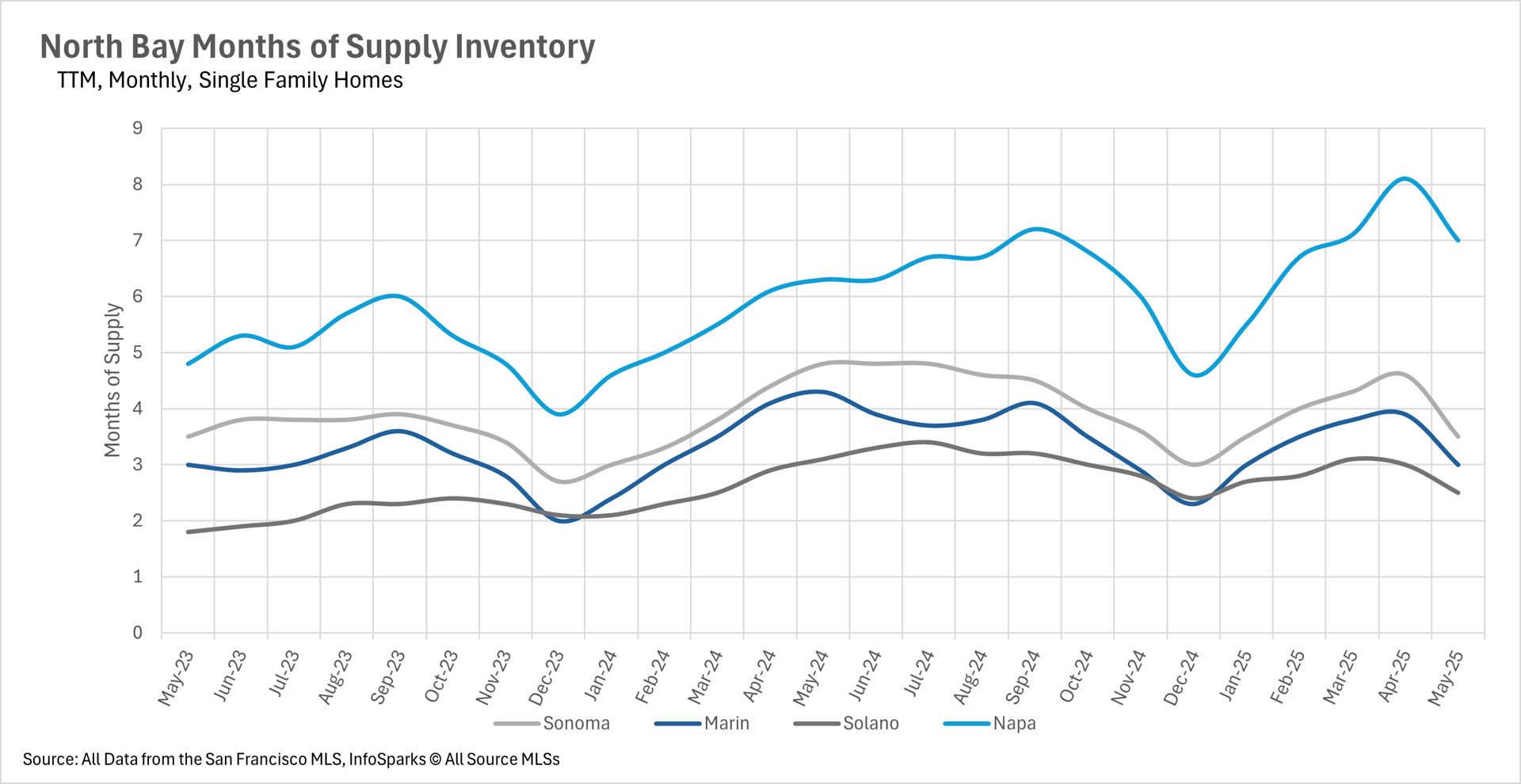

North Bay prices mostly fell, led by Napa’s 12.03% drop, though Marin edged up 2.72%. The East Bay was steady, with minor changes for homes but deeper drops for condos, especially in Alameda (-16.43%).

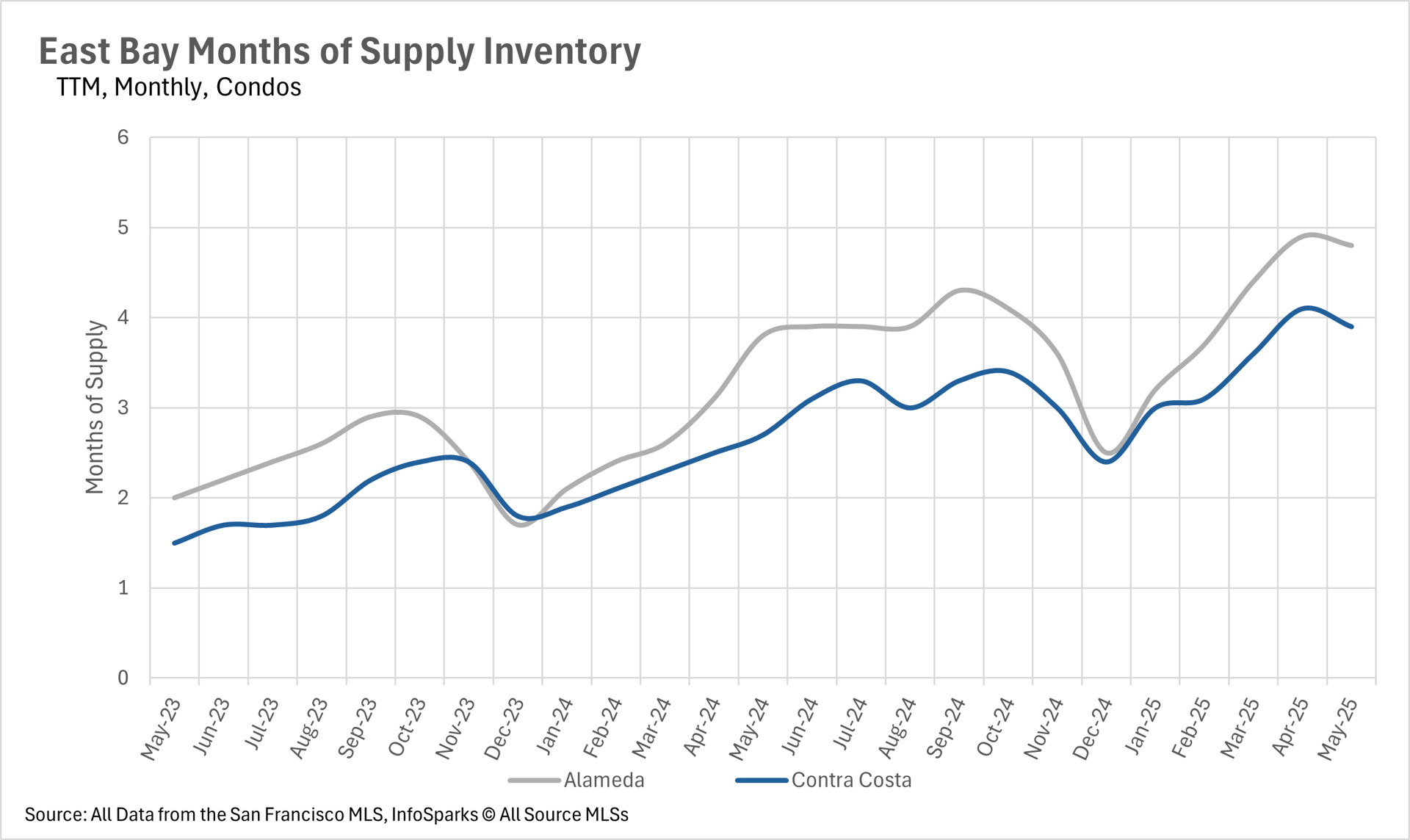

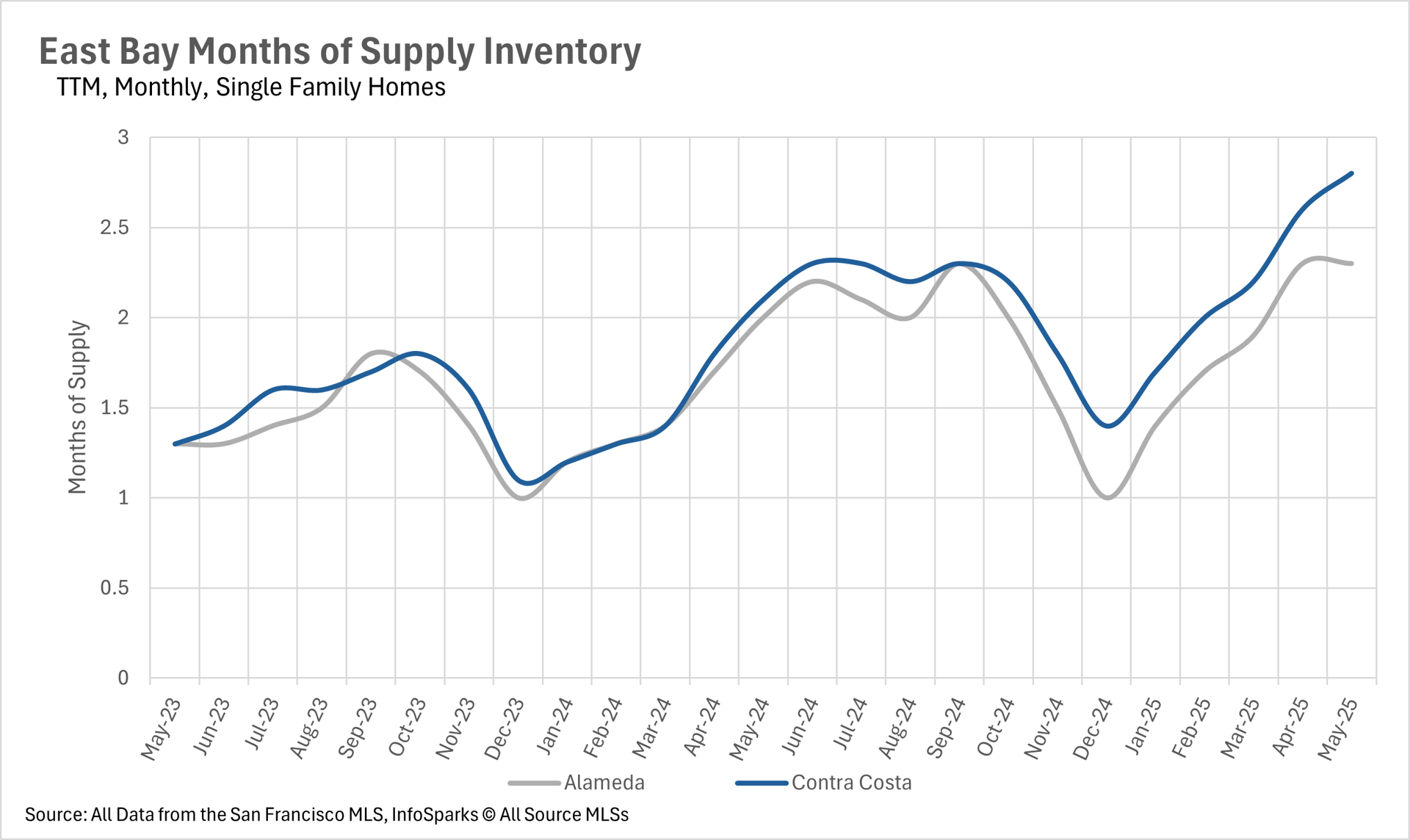

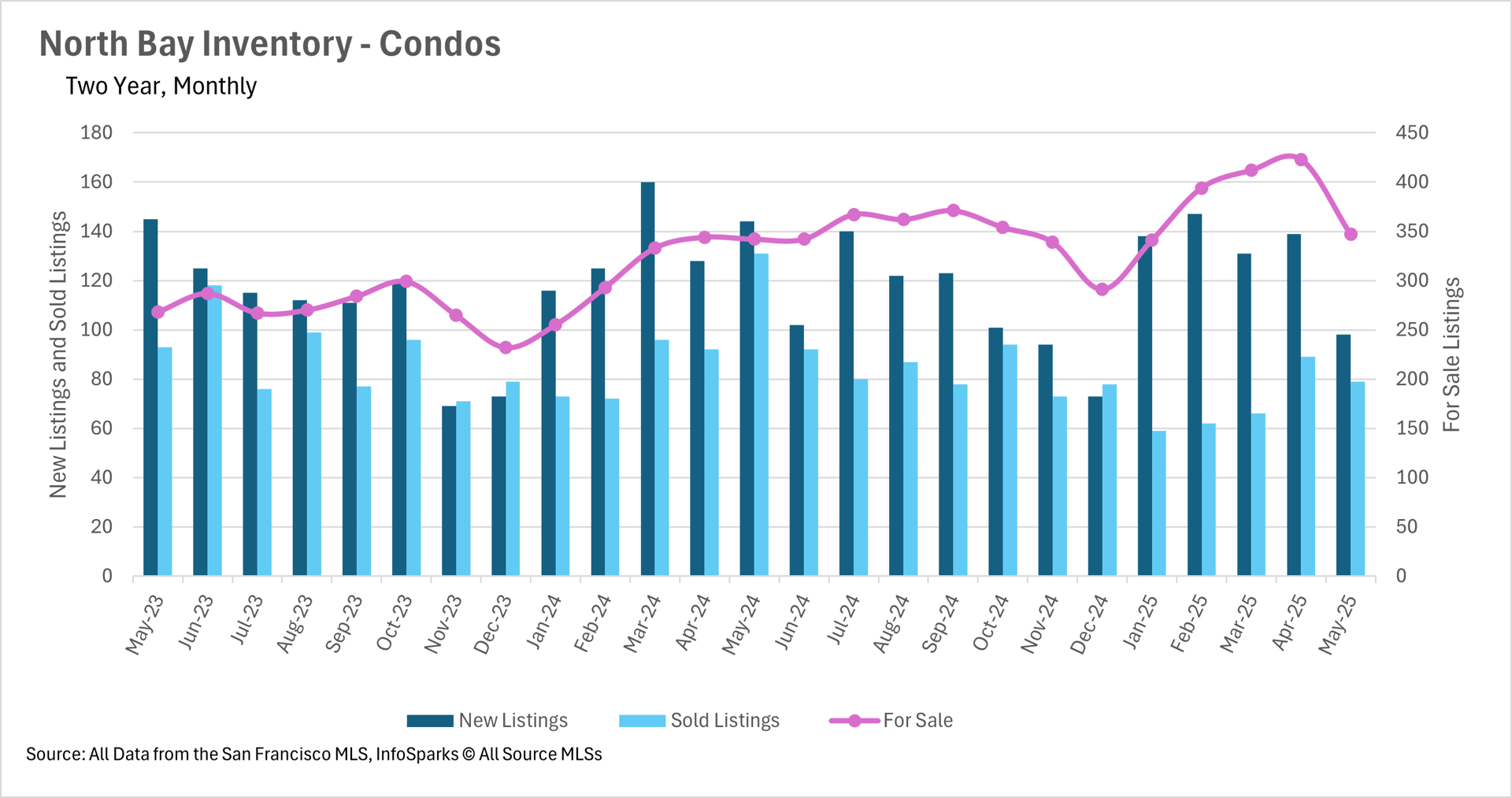

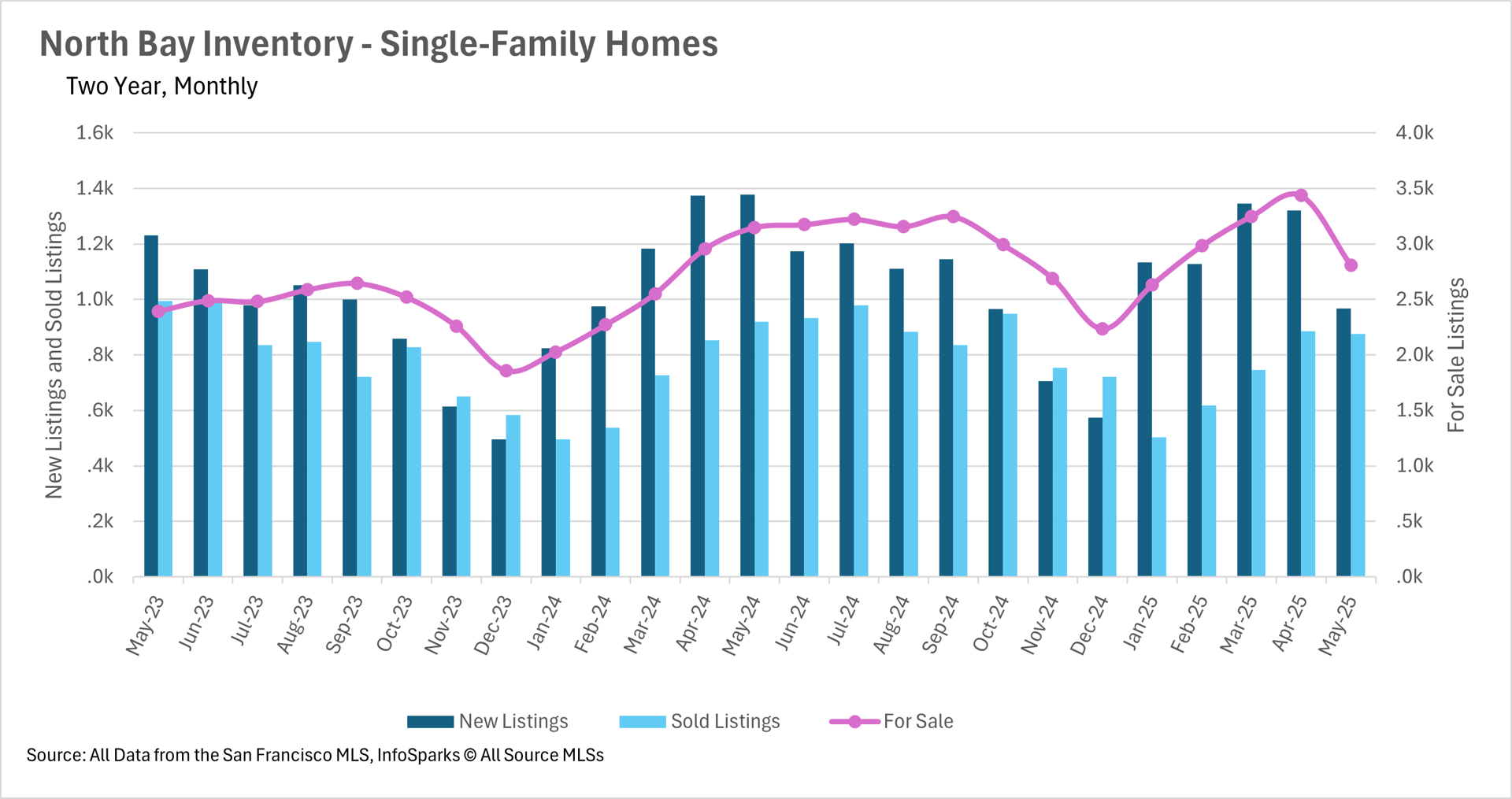

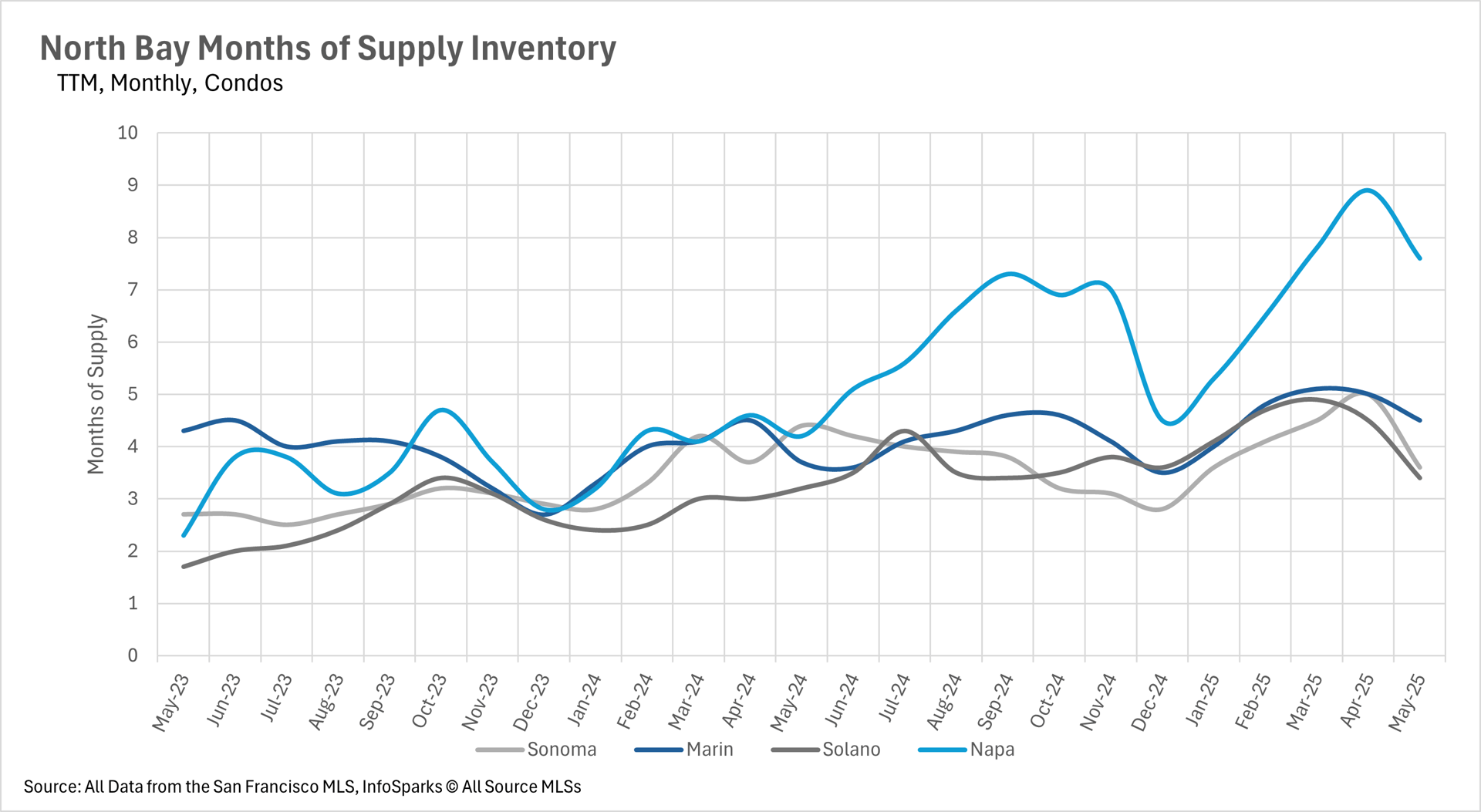

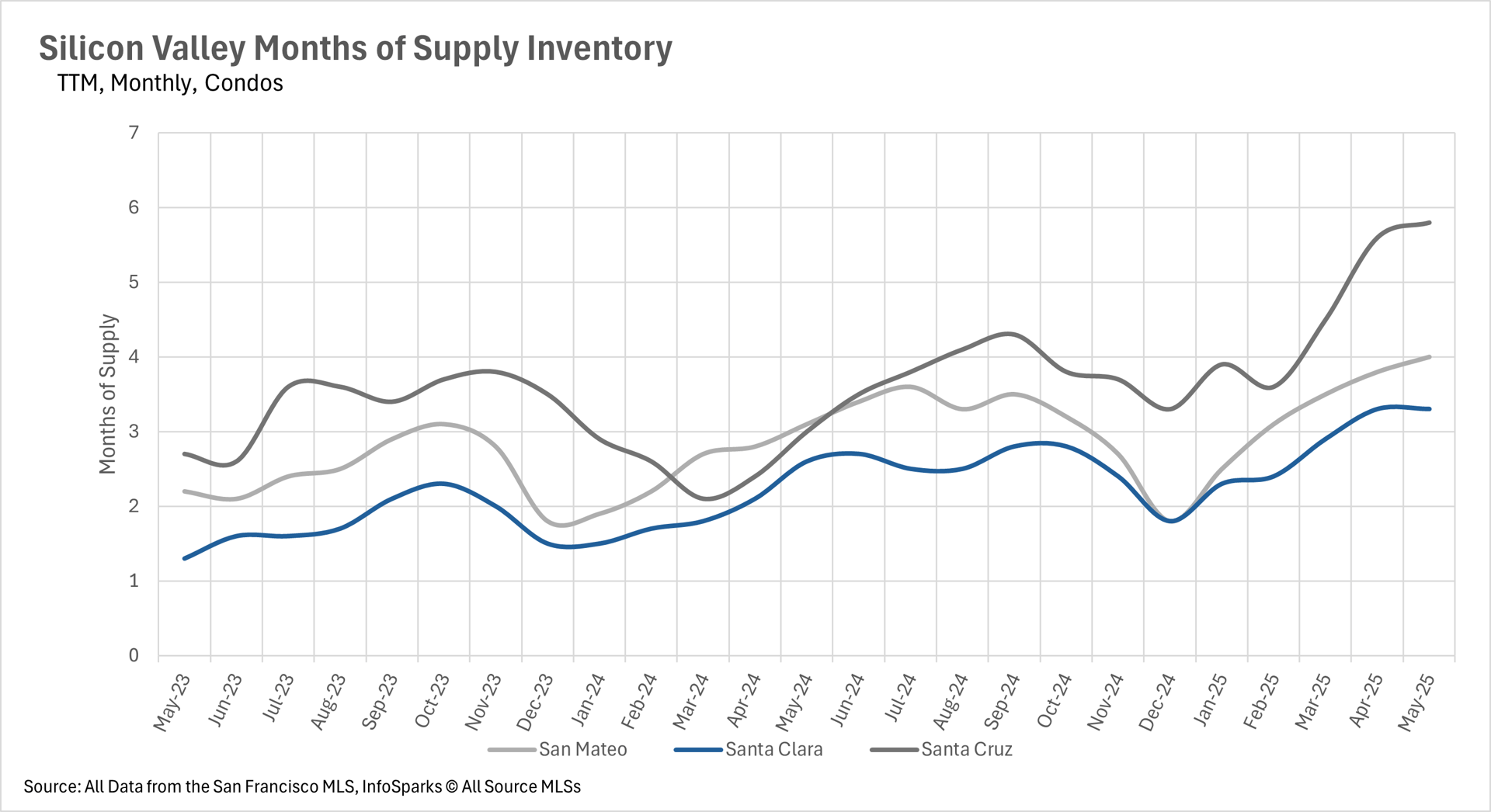

East Bay and Silicon Valley have rising inventory due to slower home sales, while San Francisco and the North Bayface declining supply. Homes are still selling quickly in SF and the East Bay, but condos—especially in Silicon Valley—are taking much longer to move. Single-family homes remain in a seller’s market, while condos are shifting toward buyers across the region.

➡️ Bottom line: Whether you’re buying or selling, property type matters more than location in today’s market.

EAST BAY

NORTH BAY

SILICON VALLEY

Stay up to date on the latest real estate trends.

May 28, 2026

May 21, 2026

May 19, 2026

Why Some Homes Sell in 9 Days While Others Sit for 35

May 14, 2026

May 13, 2026

May 13, 2026

May 6, 2026

May 4, 2026

April 28, 2026

You’ve got questions and we can’t wait to answer them.