November '23 Market Update

Home Ownership

Home Ownership

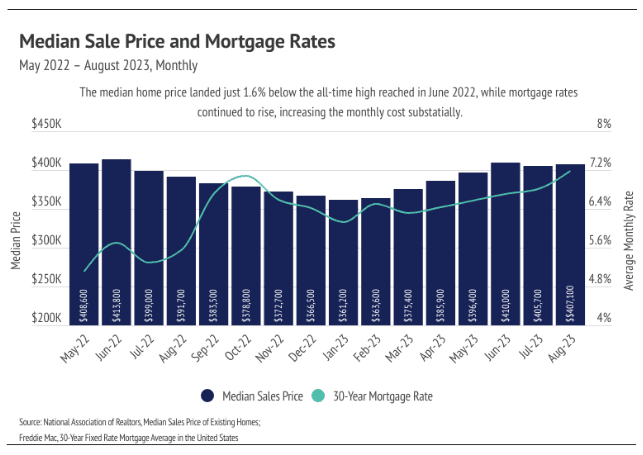

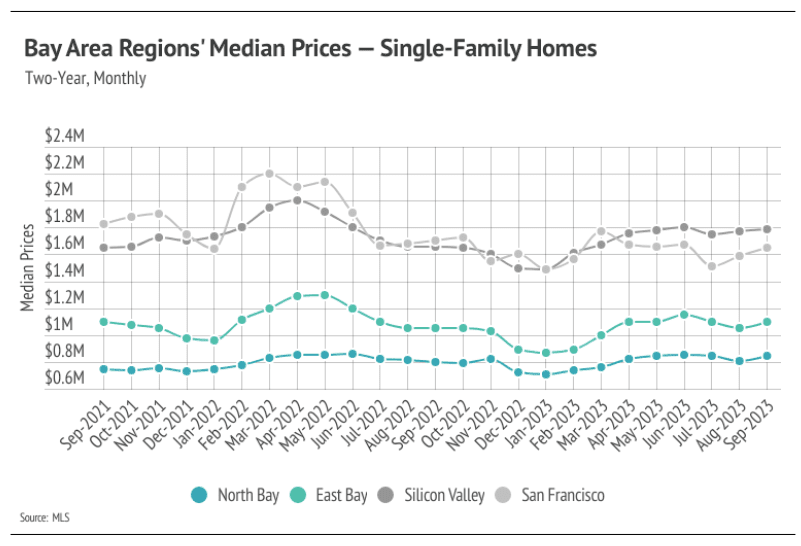

Single-Family Home Prices: Prices for single-family homes in Silicon Valley have increased year to date, indicating a strong real estate market for this property type.

Condo Prices: While single-family home prices rose, condo prices showed more mixed results. San Mateo and Santa Clara experienced increases, but Santa Cruz saw a decrease in condo prices.

Fourth Quarter Expectations: The expectation is that home prices will remain fairly stable in the fourth quarter.

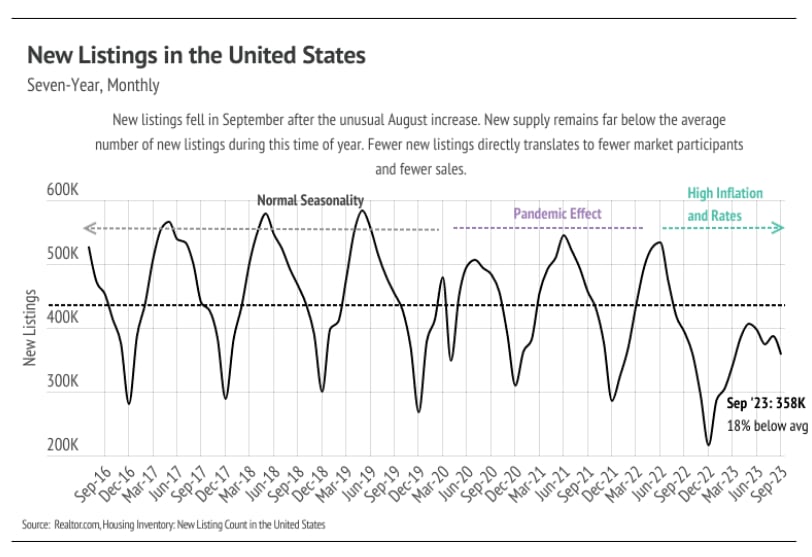

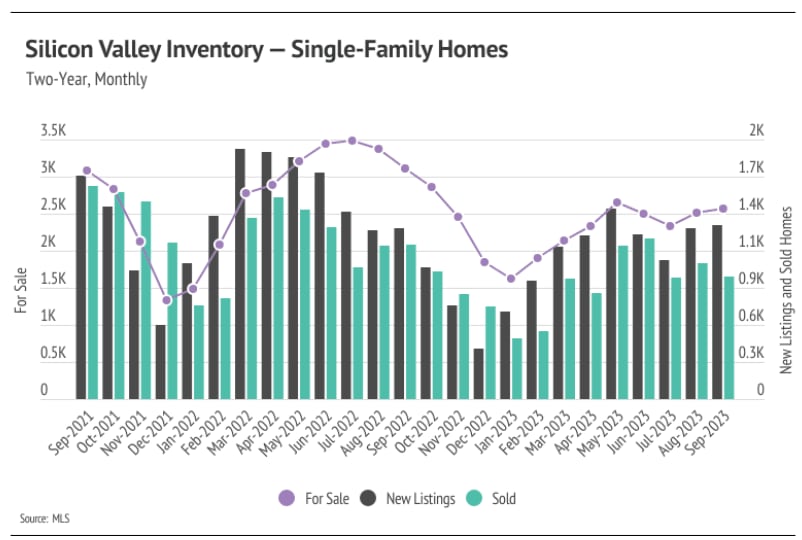

Active Listings: The number of active listings in Silicon Valley increased from August to September, continuing a nine-month upward trend. This could be a positive sign for the market.

Inventory Levels: Despite the increase in active listings, the Silicon Valley market is still 17% below last year's inventory level, indicating a continued undersupply.

Trending Toward Balance:

Stay up to date on the latest real estate trends.

June 27, 2026

June 25, 2026

June 18, 2026

June 17, 2026

June 11, 2026

June 4, 2026

June 4, 2026

May 28, 2026

May 21, 2026

You’ve got questions and we can’t wait to answer them.