October 2024 Bay Area Real Estate Market Insights

Market Update

Market Update

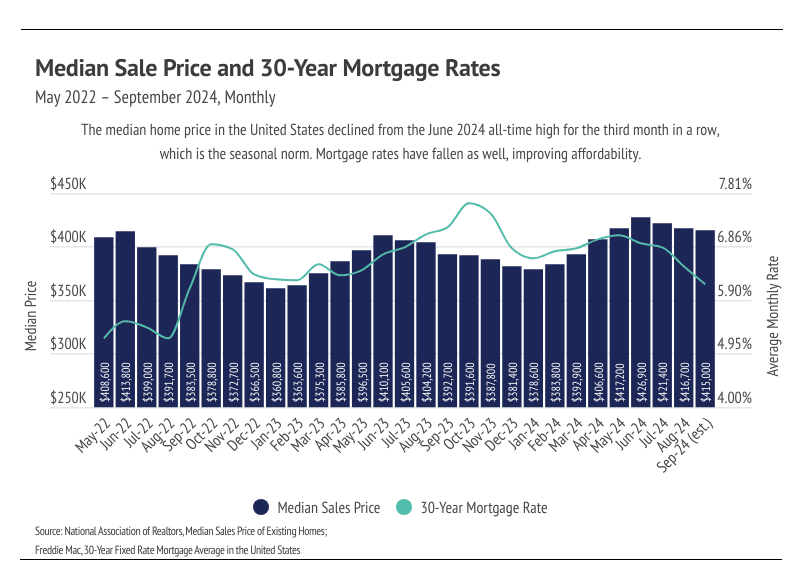

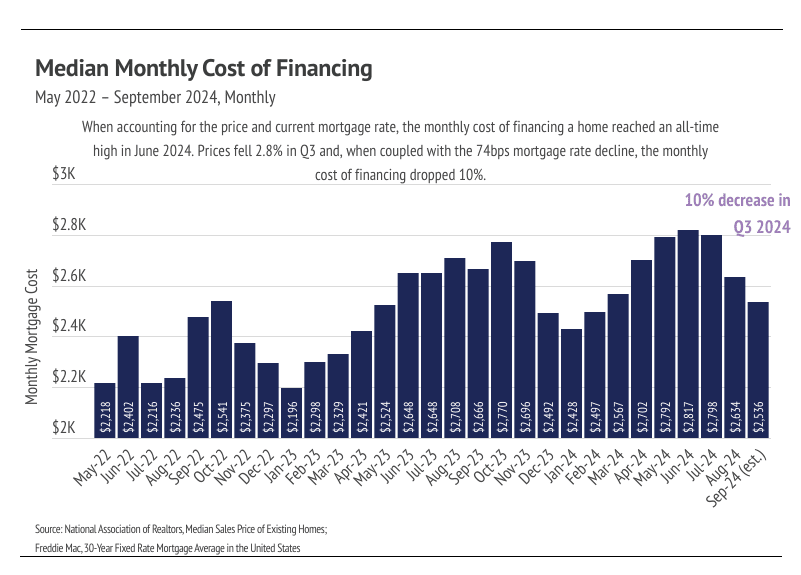

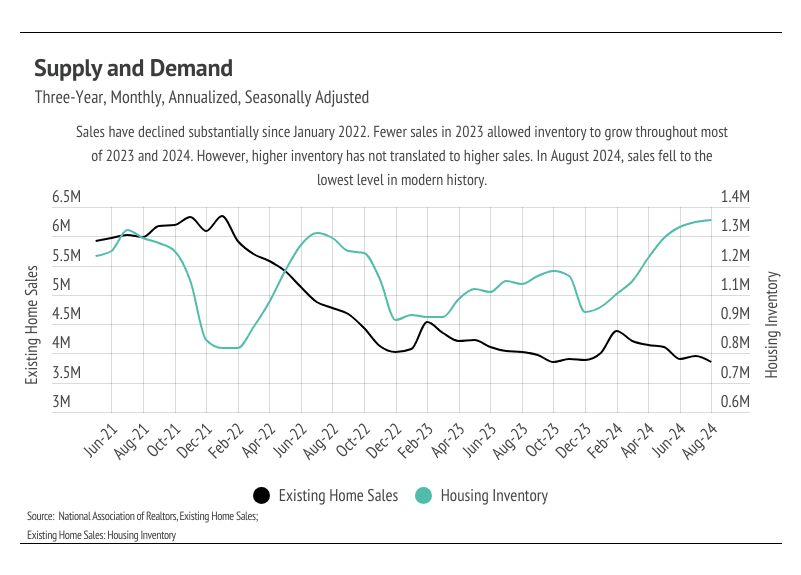

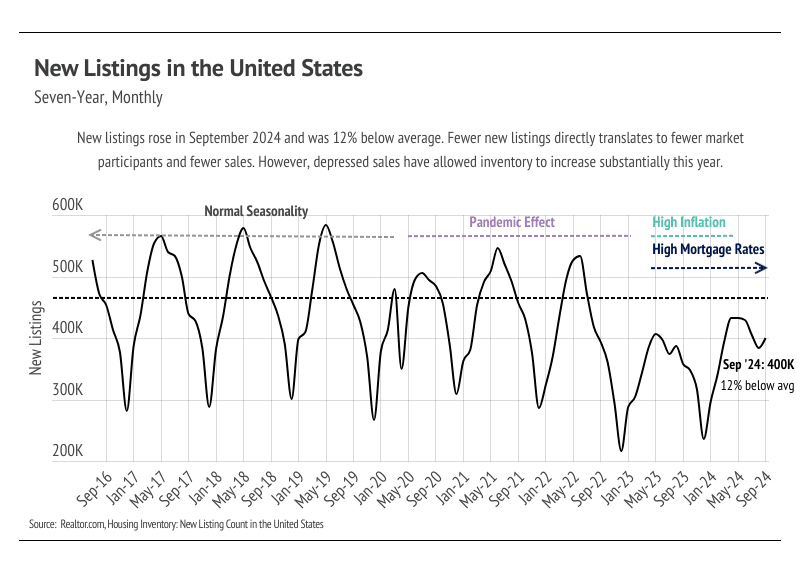

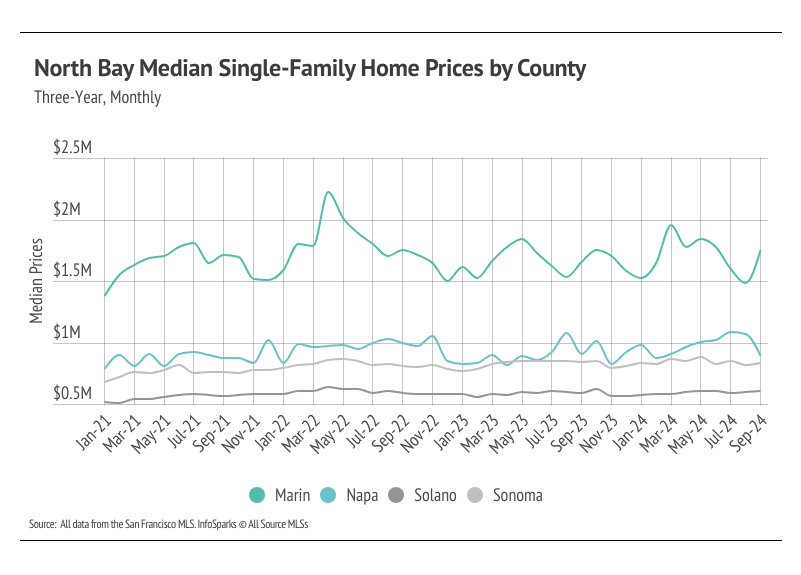

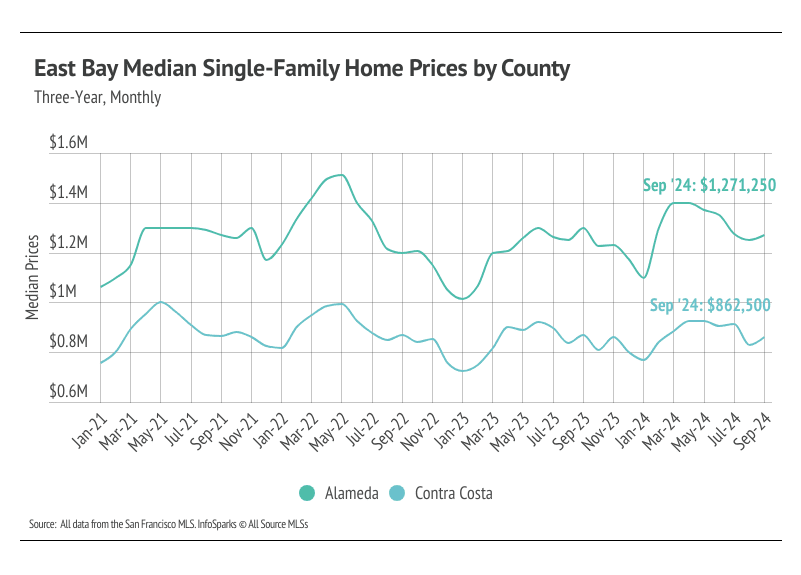

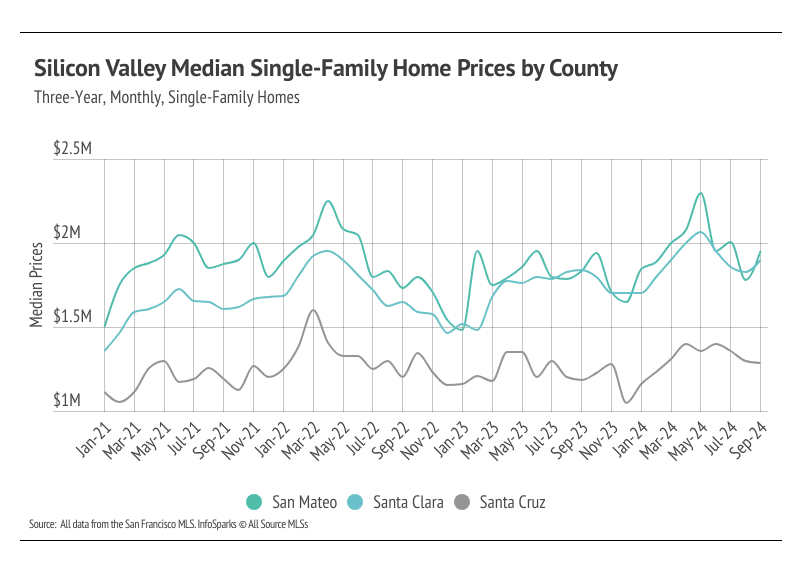

The national housing market peaked in June 2024, with prices now following a typical cycle of rising early in the year and declining later. Sales have been decreasing for nearly three years, leading to high inventory levels. Even though mortgage rates have dropped, sales remain at historic lows.

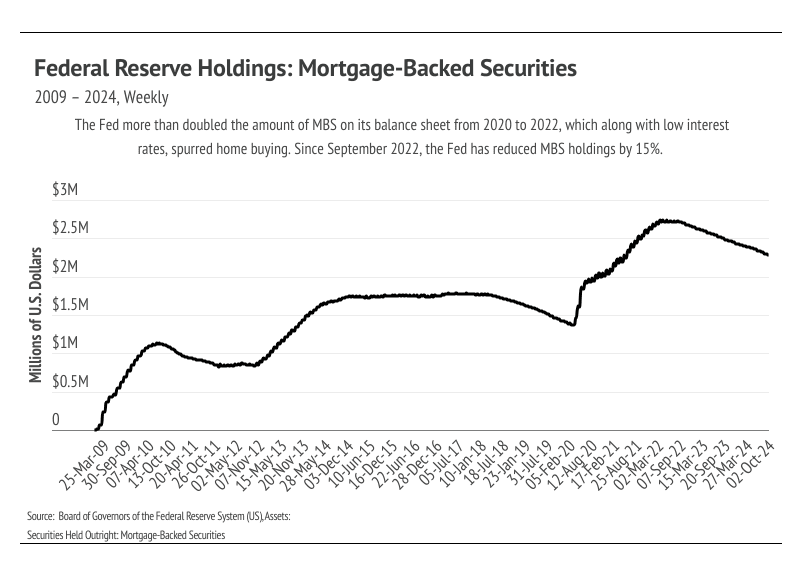

The Fed’s rate cut in September had limited impact, as it was already factored into current rates. Lower rates did improve affordability, with buyers saving significantly on mortgages compared to June. However, changes in the Mortgage-Backed Securities (MBS) market have made loans harder to originate, contributing to a slowdown.

Despite fewer sales, home prices have continued to rise, behaving more like risk assets since the mid-1990s. Looking ahead, lower rates, high inventory, and lower seasonal prices could drive a stronger spring market in 2025.

BIG STORY DATA

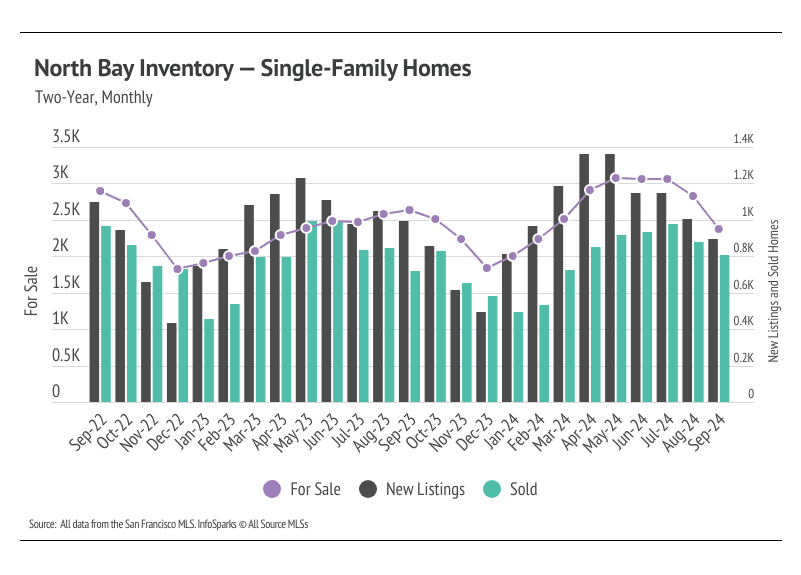

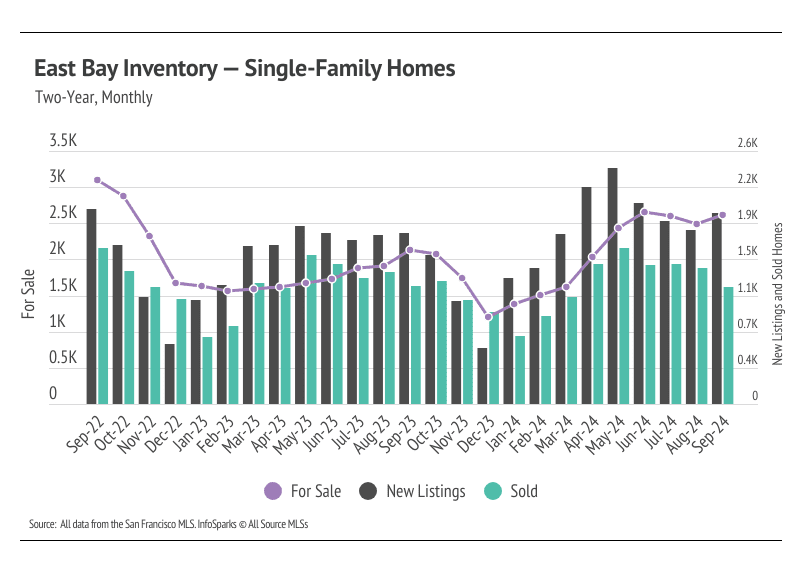

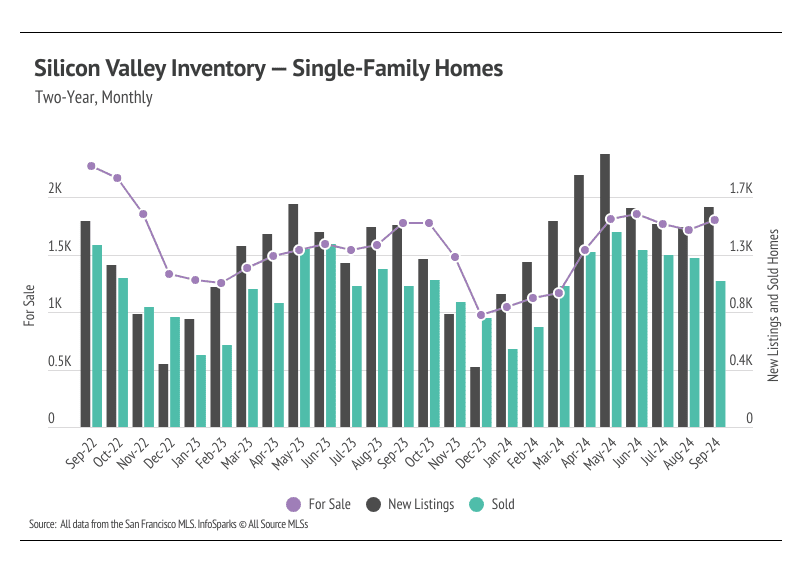

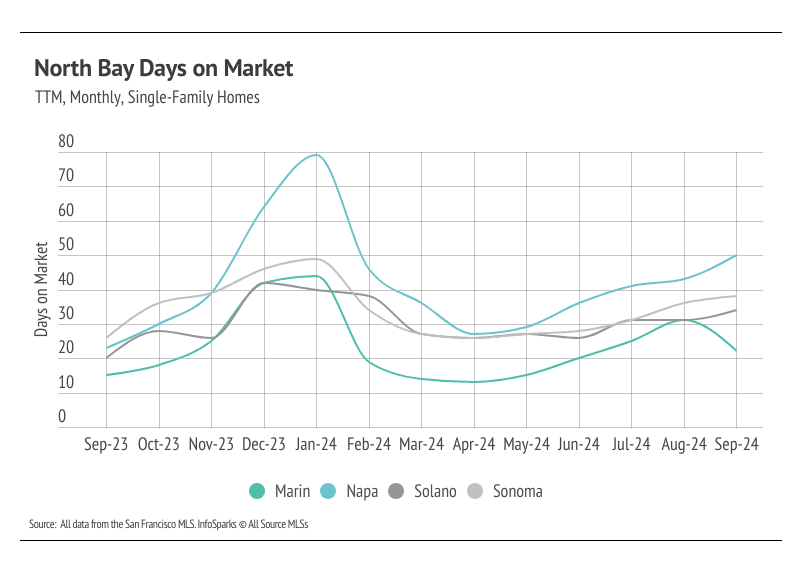

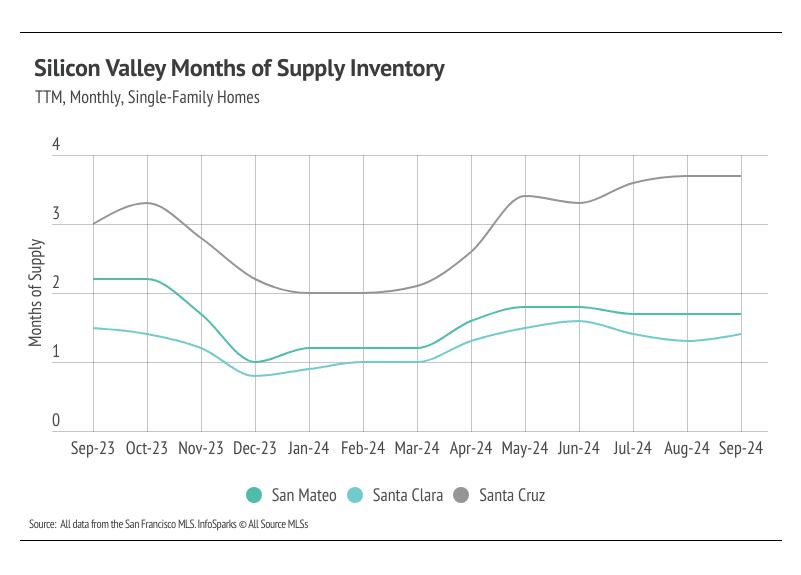

THE LOCAL LOWDOWN

Stay up to date on the latest real estate trends.

May 28, 2026

May 21, 2026

May 19, 2026

Why Some Homes Sell in 9 Days While Others Sit for 35

May 14, 2026

May 13, 2026

May 13, 2026

May 6, 2026

May 4, 2026

April 28, 2026

You’ve got questions and we can’t wait to answer them.